Insights

May 16, 2023

Thin Ice – Regional Banks in Commercial Real Estate

In Market Commentary

This is a whitepaper from Coldstream’s Investment Strategy Group Analyst, Calm Qi, on the mounting pressure in Commercial Real Estate (CRE), especially the office sector, after the collapse of Silicon Valley Bank.

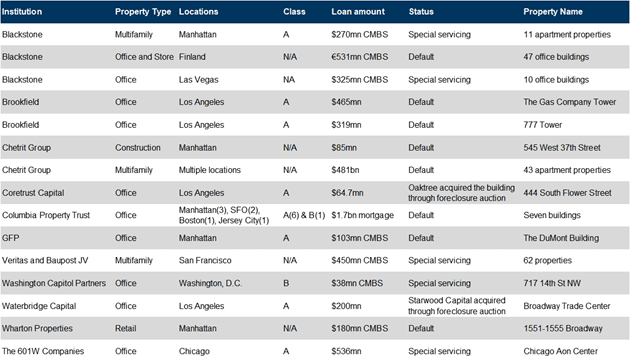

Although it appears that the collapse of SVB did not result in widespread contagion to other regional banks, we wanted to analyze regional banks’ exposure to commercial real estate, especially in the office sector. There have been a slew of high-profile news headlines around CRE loan defaults in bustling urban centers held by prestigious asset managers (Exhibit 1).

Exhibit 1: Recent CRE Loan Defaults

Source: Company reports, CoStar, compiled by Goldman Sachs Global Investment Research

OOF: Trouble in the Office Sector

Office properties dominate this list and it is easy to see why from the fundamentals: (1) a structural demand shift post-Covid caused low occupancy as people prefer working from home (Exhibit 2); (2) the cost of capital, including debt service costs, refinancing, hedging, are skyrocketing due to the Fed’s rapid interest rate hike (Exhibit 3); and (3) much tighter lending standards as regional bank failures caused lenders to be extremely conservative (Exhibit 4). These fundamental backdrops also collide with the fact that not only are 2023 and 2024 peak years for CRE loan maturities, with about $1.1 Trillion in total, with office loan maturities accounting for around 23% (Exhibit 5), but also they are peak years for lease expiration. JLL’s data suggest around 900 million square feet of office space is set to expire by 2025, representing 13.8% of the total stock.

Exhibit 2: Average US Weekly Office Occupancy

Current office occupancy across the US is tracking at 50% vs pre-pandemic levels.

Source: Kastle, Goldman Sachs

Exhibit 3: 10-Year Spread to SOFR Swaps

SOFR (Secured Overnight Financing Rate) is an overnight bank lending rate typically used as a benchmark for commercial real estate lending. The cost of capital for lower quality assets has significantly increased.

Source: Trepp, CNBC

Exhibit 4: CMBS Origination Volume

If we use CMBS issuance as a gauge into the total loan origination of CRE, it is clear that tighter credit conditions have squeezed borrowers. During the first quarter of 2023, private-label CMBS issuance is down 79% year over year. The last time it was as low was in 2009, right after the Great Financial Crisis.

Source: Trepp

Exhibit 5: $1.1 Trillion Commercial Mortgage Maturities in 2023-24 by Property Type

Office accounts for 23% of the commercial mortgage maturities in 2023-24.

Source: Mortgage Banker Association, Goldman Sachs

These fundamental conditions create a significant headwind for the CRE market, especially in the office sector. As a result, we have observed that delinquencies are on the rise, not only in the office sector, but also extending into multifamily (Exhibit 6). Rent growth has decelerated across all property types, even in the hotly sought after industrial sector (Exhibit 7). Total US CRE transaction volumes have plummeted along with leasing activities (Exhibits 8 & 9), making liquidity harder to come by. Sellers who are in dire need of liquidity might be forced to sell their property at heavily discounted prices, placing a big question mark on the actual value of the underlying property.

Exhibit 6: CMBS Delinquency Rate Across Property Types

Again, using CMBS delinquency rate as a gauge into the total CRE loan market, office and multifamily sectors saw the highest delinquency rate increase recently. Although it is still relatively mild compared to other notable stress periods, the consensus estimates expect the delinquency rate to continue to pick up in the coming months.

Source: Trepp, Goldman Sachs

Exhibit 7: Rent Growth in the US YOY

Rent growth has started to decelerate across all property types.

Source: CoStar, Goldman Sachs

Exhibit 8: Total US CRE Transaction Volume is Down 60% YOY

The transaction volume decline signals liquidity running dry given the Fed’s rapid rate hikes. In addition, the lack of liquidity makes pricing certain assets more difficult due to the lack of comparable sales.

![]()

Source: RCA, Goldman Sachs

Exhibit 9: Total US Leasing Activity is Down 35% YOY

Cost cutting has become a major theme among the biggest clients of CRE as the fear of a recession continues to loom.

Source: CoStar, Goldman Sachs

Looking past a possible recession and the Fed’s interest rate hiking cycle, the outlook for commercial office sector is still poor. According to data from CoStar and CommercialEdge, there were around 123.5 million square feet of new office space under construction and a further 271.3 million square feet in the planning stages, although these may get canceled or postponed. Adding insult to injury, around 232 million square feet of vacant space, tracking at twice the amount of pre-pandemic levels, further exacerbates the worsening demand-supply dynamics as workers are less willing to return to offices. This imbalance remains a deciding factor on the tepid growth trajectory facing commercial offices that could potentially suppress both rent and value.

The Role of Regional Banks

Regional banks are certainly not the only source of funding for CRE but are the fastest growing lender to CRE in the last 10 years, accounting for 90% of the increase in bank CRE loans since 2015 (Exhibit 10). Within the office sector, regional and local banks account for 30% of total lending and 62% of bank lending (Exhibit 11). Upon further examination of banks’ balance sheets, according to Goldman Sachs’ analyst, CRE makes up 25% of US banks’ loan mix. However, the smaller the bank’s asset base is, the more the bank skews toward commercial real estate lending. Banks with less than $100 billion in assets currently control around 65% of the total bank CRE lending (Exhibit 12).

Exhibit 10: Ownership of CRE Loans

Smaller banks have been the fastest growing and are now the largest holder of CRE loans.

Source: Federal Reserve Board, Bloomberg, JPMorgan

Exhibit 11: Composition of US Office Debt Market by Lender Group – 2022

Regional banks are the biggest lender in the troubled office segment.

Source: RCA, Goldman Sachs

Exhibit 12: Loan Mix by Asset Size

Banks with less than $100 billion in asset hold 65% of the total CRE bank loans, while larger banks tend to lean towards the more stable consumer and C&I debt.

Source: SNL Financials, Federal Reserve Board, Goldman Sachs

The concentration of CRE loans in smaller banks is a direct result of a decades long commercial real estate bull market, and artificially induced ultra-low interest rates. CRE debt was considered a relatively safe investment even in the hardest of times – the Great Financial Crisis (Exhibit 13), as it provided stable cash flows coupled with the potential of appreciation and was often secured by a 1st lien loan on the asset. It also enabled regional banks to participate in their region’s economic development.

When the pandemic hit and work from home became prevalent, the economics of CRE office investments changed dramatically, with both rent and valuations declining. Currently, there are very few transactions occurring in the CRE office sector. CRE loans are typically 10-years in length, and refinancing these loans will prove to be challenging as CRE loans typically have a balloon payment at the end of their term. Without new financing, landlords won’t be able to repay the previous loans. Further, some CRE loans are floating rate loans, and the increase in interest rates may prove challenging for landlords to make monthly loan payments timely. Although the bank may have made the loan with a low LTV originally, the bank’s principal may be impaired given the significant decline in value. Banks will attempt to sell the property to get their principal back but may not be able to do so.

Currently, we are seeing the beginning stages of a downward spiral in the office sector: (1) CRE is a highly leveraged business. The Fed’s rapid interest rate hikes have significantly eroded operating net income and suppressed appreciation due to high debt servicing costs; (2) Banks have been trying to tighten lending standards in anticipation of a future economic downturn, and they have experienced the largest deposit draw since the 80’s due to the recent regional banking crisis; (3) As a result of the regional banking crisis, tougher regulatory oversight is likely to hit banks in the coming months potentially creating more liquidity constraints; and (4) While high-profile delinquencies have been focusing on Class A office properties, there exists a vast pool of Class B and C office inventory (Exhibit 14). According to CWK, around 1.4 billion square feet of office will be considered obsolete by 2030, a strong indication that the worst is yet to come.

Exhibit 13: Commercial Real Estate Loans, All Commercial Banks

CRE loan levels have stayed extremely stable even during the GFC era, only experiencing a slow-paced 17% decline post-GFC as banks recapitalized.

Source: FRED

Exhibit 14: US Office Inventory by Class

There exist large pools of Class B and C office inventories that may well become impaired as tenants will have bargaining power as they can lease Class A properties for lower lease payments and will need more innovative ways to lure employees back to the office.

Source: CoStar, Goldman Sachs

Implications and Silver Lining

To wrap up, what are the implications to regional banks in this potential downfall? JP Morgan’s Investment Bank conducted a bank stress test assuming 21% default in offices that showcased a 30-40 basis point reduction in Tier 1 capital for some smaller regional banks. Although that does not seem very large, the actual effect might be higher as the analysis ignores the effect of a possible recession and the higher cost of customer deposits. So, it presents a significant risk that can potentially cause another downfall in smaller banks with large CRE exposure, assuming there is no government intervention.

There exist a few silver linings: (1) We are nearing the end of the Fed’s hiking cycle; interest rate stabilization will relieve some pressure from the banks; (2) Industrial and multifamily fundamentals remain strong and have become the go-to asset type for equity real estate investors due to the rise of e-commerce during Covid and the shifting US demographics. CRE has also evolved to include more non-cyclical sectors such as medical office space, self-storage, and student housing that could offer alternatives to traditional real estate investing; and (3) Banks typically prefer not to take the keys to the building, and a good percentage of foreclosed buildings will go to auction, which could create significant opportunities for distressed real estate managers. In addition, office conversions to other uses have become an increasingly attractive and popular option to transform older, less competitive buildings. CBRE predicts strong growth in the conversion strategy (Exhibit 15). However, the cost of converting Class B and C office space into condos or other non-office use may well be prohibitive.

One thing is for sure: the office sector will only become more vulnerable if the current situation persists. Given the vertiginous drop in transaction volume year-to-date, even the most experienced analyst will have a hard time determining the true value of these loans, so they will remain a mystery until events unfold. The eventual outcome not only depends on lenders and landlords getting creative to bridge the gap left by the pandemic, but also depends on the delicate dance performed by the Fed, if they can steer the economy away from a potential recession ahead.

Exhibit 15: Office Conversion by Construction Status and Estimated Year of Completion

Source: CBRE

Calm Qi is an Analyst at Coldstream Wealth Management in Bellevue, Washington. Coldstream Wealth Management is an independent firm offering comprehensive financial planning and customized investment portfolios for high net-worth individuals, families, and organizations. We guide you through the complexity of wealth management so that you can have peace of mind while achieving the financial and lifestyle goals important to you.

Disclaimer: This paper is not an offer or solicitation with respect to the purchase or sale of any security, nor does it constitute investment advice or tax advice, and is not intended as an endorsement of any specific investment or investment strategy. Additionally, any performance numbers displayed are for presentation purposes only, and should not be construed as a guarantee of performance for your investments. Actual performance results could differ depending upon the size of a portfolio, investment objectives and restrictions, current economic environment, and other factors. You should consult with a Coldstream representative for specific advice.

Related Articles

April 13, 2026

Watch Coldstream’s MarketCast for Second Quarter 2026

April 9, 2026

Turbulence: Navigating a Complex First Quarter

January 29, 2026

Artificial Intelligence: Boom or Bubble?