Insights

June 11, 2020

The Stock Market and the Economic Recovery

In Market Commentary

June 08, 2020

Ending on June 3rd, the S&P 500 had the biggest 50-day rally in its history, gaining 37.7% over that period, and the NASDAQ Composite Index set a new all-time high on June 7th. As of the date of this letter, every stock in the S&P 500 is up over the last 10 weeks. S&P 500 valuations are the highest in nearly 20 years, as investors apparently think corporate profitability will dramatically increase relatively soon. The most common question we are receiving from clients is whether this rally can be sustained.

In our last communication, we explained that the S&P 500 index does not reflect the composition of the US economy because that index is disproportionately composed of large technology companies. However, the recent rally has extended well-beyond technology companies – to companies that have been significantly affected by the economic shut-down. Investors seem to be anticipating a strong and relatively quick economic recovery.

In trying to understand the pace of an economic recovery after a pandemic, history provides no assistance. The closest analogy to this pandemic is the Spanish flu, but that pandemic occurred over 100 years ago, when the economy and financial markets bore little resemblance to now and medical science was far less advanced. As there is no precedent for an economic recovery from such a widespread pandemic, the range of potential outcomes is extremely wide, but is highly dependent on two things: the confidence of the US consumer and the control of the virus.

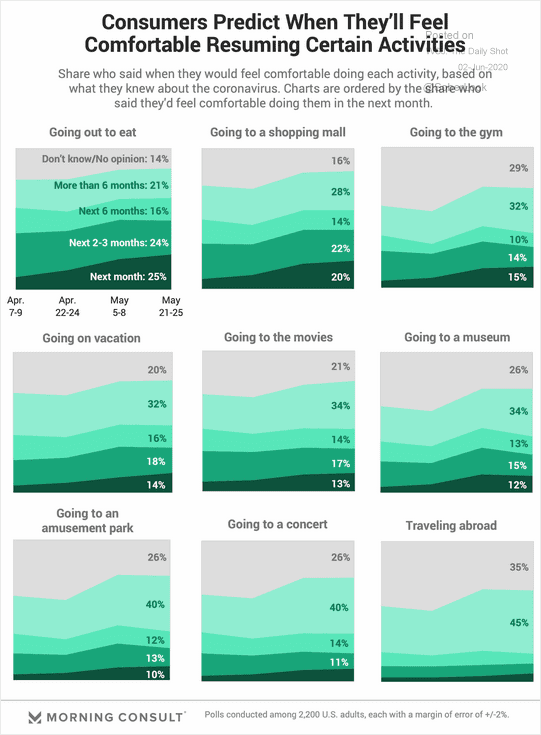

As the consumer is the primary driver of the US economy, the timing and extent of an economic recovery are dependent on the consumer feeling safe in resuming normal activity. Morning Consult, a respected polling organization, has been tracking consumer sentiment regularly regarding consumers’ confidence in returning to various activities:

Source: Daily Shot

While the graphic shows consumer confidence increasing with each subsequent poll, the percentage of consumers who say that it will take more than six months to engage in these activities ranges from 20% to 40%. Unless that changes over time, it will be a significant headwind to a full recovery.

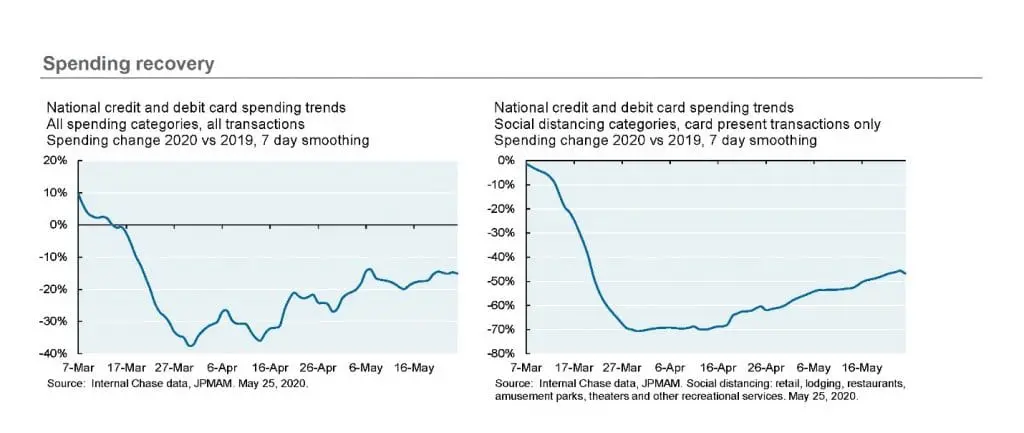

The activities the poll focused on are what JP Morgan describes as “social distancing” activities (such as non-internet retail, restaurants, and lodging). JP Morgan analyzed credit card data to determine whether there is significant consumer reluctance to engage in “social distancing” activities – the result was a resounding “yes.” In “social distancing” categories, credit card usage is still about half of what it was prior to the pandemic. However, more broad-based consumer credit card spending has recovered more than “social distancing” spending, down only approximately 20% from the beginning of the year.

Source: JPMorgan

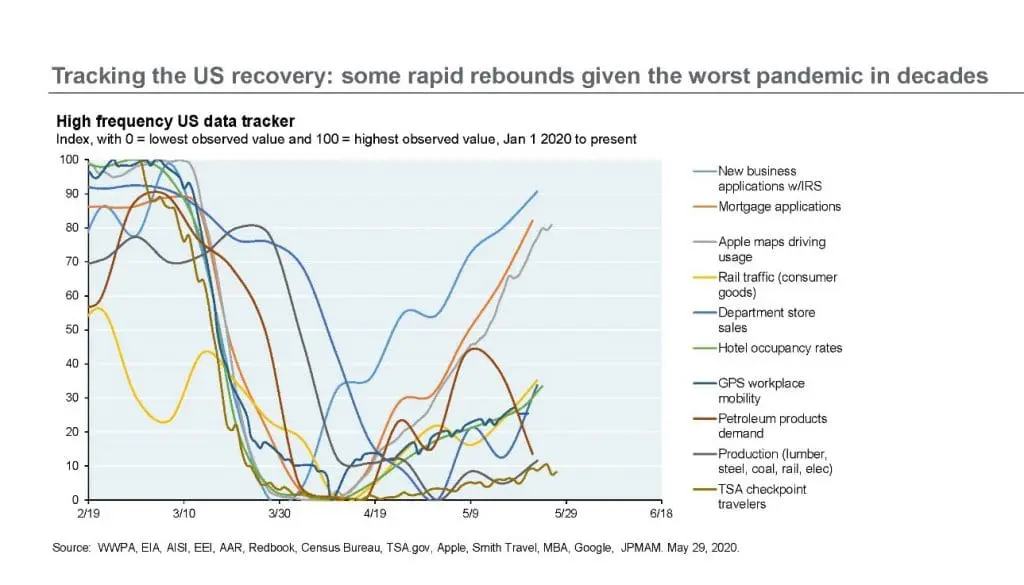

Other types of tracking data show significant increases in some types of activities, while increases in other types of activities remain muted: activities such as new business filings and mortgage applications are at near pre-crisis levels while TSA checkpoint travelers, industrial production, and workplace mobility are still far below pre-crisis levels.

Source: JPMorgan

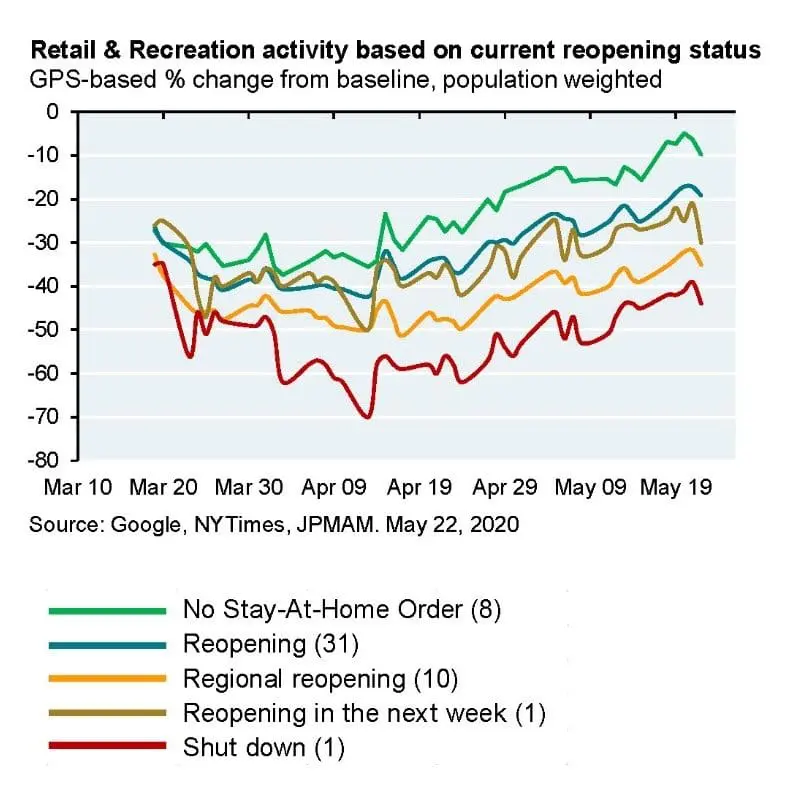

The extent of the recovery in “social distancing” activity varies widely from state to state and is affected by the degree of a state’s lockdown. This may be a positive sign showing once a lock-down is lifted attitudes change. However, the difference could also be explained by the fact that the lock-downs generally occurred in states with a higher rate of infection and by regional differences.

Source: JPMorgan

In sum, the data illustrates the variance in rates of recovery depending on both the activity involved and the geographic area of the shutdown. And also indicates that consumers as a whole are not ready to return to their prior level of economic activity.

In regard to the potential of a further economic disruption resulting from a second wave of the virus, we have yet to see a second wave in the US, but progress toward eradication has been slower than public health experts anticipated. While the number of cases and deaths nationally have gone down materially, these national figures, in part, reflect the decline of cases and deaths in some of the US’ biggest hot spots: New York, New Jersey, and Connecticut. However, in several states where the spread of the virus was not nearly as severe as in the hot spots, there have been recent increases in cases.

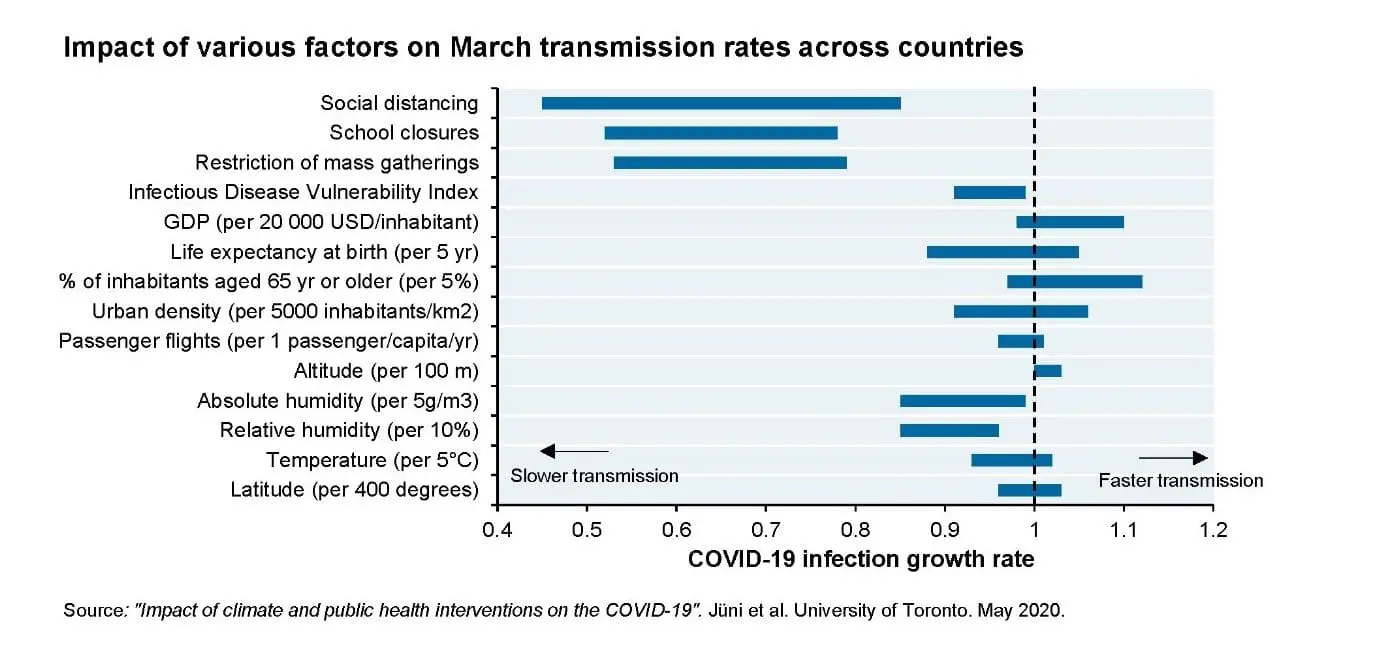

We are still learning about this virus – some factors health experts thought would have a significant impact on the spread of the virus appear less important than previously thought. For example, humidity does not seem to affect the virus as much as initially thought, nor does the virus appear to spread from surface contact as much as previously thought. Current thinking still places significant weight on social distancing, school closures, and restricting mass gatherings as having the biggest impact on virus spread. With the recent protests, we will see how important the mass gathering factor truly is.

Source: JPMorgan

While the course the virus will take is unknowable, even if we assume continued progress in reducing the spread of the virus (absent a vaccine), the evidence indicates that the economy will not return to pre-Covid levels this year. The consensus estimate appears to be that absent a second wave, the economy will return to about 80% of its pre-Covid levels by year-end. But the margin for error in this calculus is extremely wide as no one can accurately predict the course of the virus or the behavior of the US consumer three months from now.

Current equity valuations are high by historical standards, and approximately 40% of the companies composing the S&P 500 index are so unsure about their financial future that they have suspended guidance. The equity market is pricing in a quick and strong economic recovery, but the speed and extent of the recovery are far from certain. Nonetheless, the positive momentum moving equity markets currently is a powerful force that can continue far longer than one expects. In balancing these competing factors, we have tilted client portfolios to a slightly conservative positioning as we view the balance of risk to be to the downside. However, this tilt does not affect our belief in diversification. Given the broad range of potential economic outcomes, diversification becomes as important now as it ever has been. Even with the slightly conservative tilt, a diversified portfolio is designed to participate in the upside if the market continues to rally, but buffer the impact of an equity drawdown, if it occurs.

If you have any comments or questions, please feel free to contact me, your Relationship Manager, or your Portfolio Manager.

Sincerely,

Howard Coleman

Chief Investment Officer and General Counsel

Insights Tags

Related Articles

July 11, 2025

The Return of Diversification

July 10, 2025

Watch Coldstream’s MarketCast for Third Quarter 2025

June 24, 2025

Managing Increased Uncertainty in the Middle East