Insights

April 18, 2022

The Inflation Story

In Market Commentary

Simply put, inflationary pressures occur when demand outstrips supply. However, when demand dries up, recession often follows as the economy shrinks.

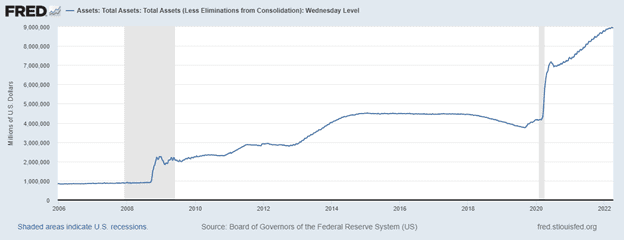

During the last two periods of great economic stress, the Great Financial Crisis of 2008 and the COVID-related shut-down of March 2020, the Federal Reserve focused on creating demand to sustain the economy and used tools it had never used before to both stabilize financial markets and spur economic growth.

During both periods, these tools included the Fed buying government bonds to drive down interest rates and taking the Fed Funds rate to zero to make the cost of borrowing negligible. During the COVID-19 shut down, the Fed did those things, plus more: for example, it bought corporate bonds to enable corporations to raise money during the shut-down. These actions supported the economy through these crises but resulted in the Fed owning far more assets than it ever owned before.

Source: Federal Reserve

In addition, during the COVID-related shut-down, Congress addressed the significant increase in unemployment and decline in economic activity by making direct cash payments to households and issuing forgivable loans to companies. These actions increased the amount of household savings and supported corporate profitability.

Although the Fed and Congress’ bi-partisan response to the economic effects of COVID were crucial to the US’ economic well-being at the time, the effect of those policies created the seeds for the inflation the US is experiencing currently. The liquidity provided by government increased the amount of household savings and resulted in a record amount of household expenditures for goods. As the COVID-19 shut down eased, household expenditures for goods still remained far above pre-COVID levels, while expenditures for services increased and returned to pre-COVID levels.

In total, consumer spending exceeds pre-pandemic levels.

Source: Federal Reserve

In addition to increased consumer demand, two other factors have created significant inflationary pressures: a shortage of workers and broken supply chains. During the COVID-19 related shut-down, unemployment in the US skyrocketed. Now that the economy is experiencing strong consumer demand, the unemployment rate has declined to pre-COVID levels, and there is a strong demand for additional labor. However, an unanticipated by-product of the crisis has been that 2 million workers have left the workforce since March 2020. This has created a demand for labor that has resulted in rising wages also fueling inflation.

There are almost 2 jobs open for every unemployed person in the U.S.

Source: Baird

The lack of available labor not only increases demand for labor but constrains the supply of goods and services that can be produced. In addition to the shortage of labor, supply has been constrained by a shortage or commodities such as lumber and the components of computer chips. These supply challenges have been exacerbated by the Russian invasion of Ukraine, as the price of energy globally has skyrocketed, along with the price of other commodities produced in Russia and Ukraine.

Combined, these events have triggered the largest increase in inflation that the US has experienced in 40 years. When inflation began to increase initially last year, the Fed viewed it as temporary, thinking the supply chain and worker shortage issues would resolve themselves quickly. As a result, it did not act to raise interest rates or immediately end its bond-buying program, and essentially, continued to stimulate demand. However, inflation has proved to be more durable than the Fed initially anticipated.

“Sticky” inflation continues to increase.

Source: JPMorgan

At its March 2022 meeting, the Fed recognized it needed to begin curtailing demand and raised the Fed Funds rate to 0.25% and indicated that there would be more rate hikes to follow. It also ended its bond buying program on April 1st and began the process of reducing the assets it owns.

From encouraging demand for most of the last 14 years, the Fed is now in the process of curtailing it. It is faced with the challenging task of decreasing demand but not to the extent it throws the US economy into a recession.

Thankfully, the Fed is undertaking this tightening while the US economy is strong. Corporations continue to be highly profitable, and US households have reduced debt and increased savings. Most leading economic indicators remain positive.

The US equity market declined by 12.99% in February from its peak before cutting its losses at the end of the quarter. Historically, how a stock market performs after a decline of over 10% depends on whether the economy enters into a recession, and there are no immediate signs of a recession this year.

Path of S&P 500 around 10% market corrections.

Source: Goldman Sachs

In the fixed income markets during the first quarter, prices fell as yields rose on inflation concerns. The path of the bond market will be dependent on the extent to which the Fed raises interest rates and inflation can be curtailed.

Despite the temporary decline in both the stock and bond market, in our view, investors should remain diversified. The old cliché that it is not timing the market but time in the market that builds wealth has proven to be true. Given the amount of global uncertainty both economically and geopolitically, there could well be continued market volatility, but no one can predict how events like the war in Ukraine will ultimately conclude or whether the Fed will act too aggressively or too passively in raising the Fed Funds rate. These could all result in very different outcomes in both the debt and equity markets. Maintaining diversification, unlike betting on a specific outcome, will mitigate losses in a down market while enabling you to participate in market rallies.

Insights Tags

Related Articles

April 13, 2026

Watch Coldstream’s MarketCast for Second Quarter 2026

April 9, 2026

Turbulence: Navigating a Complex First Quarter

January 29, 2026

Artificial Intelligence: Boom or Bubble?