Insights

February 23, 2023

Should I Participate in Deferred Comp?

In Company Benefits, Tax Planning, Wealth Strategy

This is a common question we receive from high-income executives looking for ways to reduce their tax burden. It seems like a no-brainer to defer paying taxes and keep those funds invested – right? While it’s true that tax-deferral can accelerate the growth of your investments over time, there are significant drawbacks to deferred comp plans that are worth exploring before committing to deferring your hard-earned compensation. To help our clients evaluate this decision, we consider the following factors: expected growth over time, risk of default, changes to future tax rates, and need for liquidity. Understanding the benefits and risks can help you reach the decision that is optimal for you.

What is a Non-Qualified Deferred Compensation Plan?

Many companies offer non-qualified deferred compensation (NQDC) plans as a tool for attracting and retaining executives. NQDCs are designed to avoid the onerous regulations that qualified plans, such as 401(k) plans, are subject to, including testing requirements and low contributions limits. A NQDC allows executives to earn compensation in one year but defer that compensation and the related taxes to a later year. Decisions must be made around when this income will pay out in the future and elections are generally irrevocable.

The Benefits of Deferred Comp

To help explain the benefits of a deferred compensation plan, we’ll use an illustrated example. Suppose that you are trying to decide what to do with your next $100,000 of income and you have the following two options available:

- Option 1: Defer the income by placing it in your company’s NQDC.

- Option 2: Receive the income, pay taxes, and invest the net proceeds in a taxable brokerage account.

For this example, we will assume that the investment options in both cases are identical, both accounts will generate a 6% annualized return[1], and you are in the top marginal tax bracket of 37% for ordinary income and 23.8% for capital gains (20% LTCG + 3.8% NIIT)[2]. For the sake of simplicity, we’ll set aside payroll taxes from this analysis.

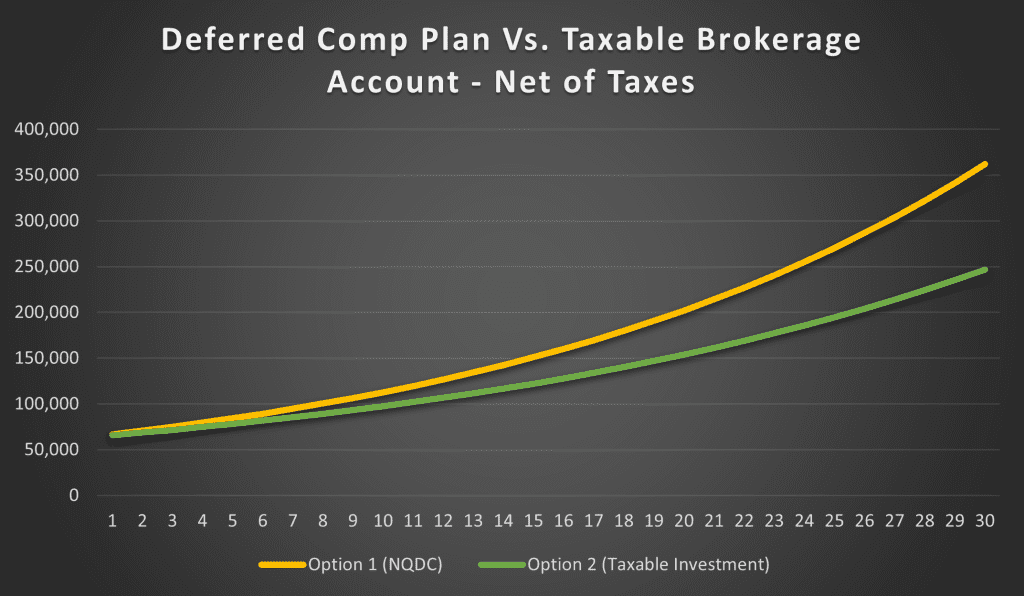

As a starting point, let’s examine how these strategies compare if you remain in the top tax bracket post-retirement. The following chart illustrates the remaining balance net of taxes for each scenario:

Source: Coldstream Wealth Management, based on above noted assumptions

Option 1 (Contribute to NQDC): In this scenario, you have a full $100,000 working for you from day 1. This amount will grow completely tax deferred until withdrawn from the plan in retirement. Under the previously mentioned return and tax assumptions, the balance would grow to $179,000 ($113,000 net of taxes) by year 10. After 30 years, the balance would be $574,000 ($362,000 net of taxes).

Option 2 (Invest in Taxable Brokerage Account): Because the $100,000 is taxed at the beginning of this scenario, $37,000 is shaved off the top, leaving you with only $63,000 to invest. Furthermore, you are not able to defer taxes on the dividends and interest paid out each year. Over shorter intervals, the difference is less meaningful, but over 20 years, it leads to a shortfall of roughly $48,000 when compared to Option 1. Over 30 years, the difference is roughly $115,000.

The benefits of utilizing a NQCD are even more meaningful if we assume that you fall into a lower tax bracket upon retirement. For example, if your ordinary income tax bracket fell to 24% in retirement and your capital gains rate to 18.8% (15% +3.8% NIIT), Option 1 would come out ahead by almost $87,000 over 20 years and $183,000 over 30 years.

The Risks of Deferred Comp

Though the long-term benefits of tax deferral through a NQDC can be meaningful, it is critical to understand the unique risks of these plans. Two of the primary considerations are changes to future tax rates and the risk of default by your employer.

Changes in Future Tax Rates:

While most people assume that their marginal tax bracket will decrease upon retirement, this is not always the case. This is especially true for those who have already contributed significant dollars to a NQDC that will begin paying out after retirement.

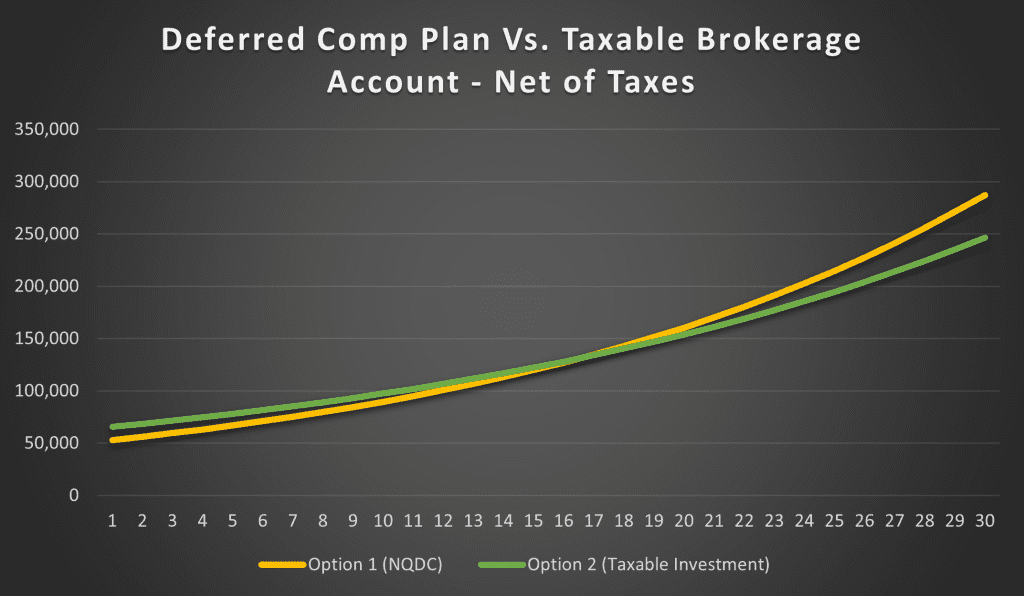

Coming back to our example, let’s look at what the impact would be if tax rates were to increase post retirement. If the top marginal tax bracket were to rise to 50% in retirement, keeping all other variables the same, it would take almost 17 years just to break even on putting money into a deferred compensation plan.

Source: Coldstream Wealth Management, based on above noted assumptions

Risk of Default:

To understand the considerations around credit risk, it is important to be familiar with how NQDCs can offer tax deferral without adhering to the rules of qualified plans. Unlike a qualified plan, when an employee enrolls in a NQDC, they are electing to forego constructive receipt of a portion of their salary or bonus – in other words, the deferred income is still an asset of the company. Participants are essentially issuing an unsecured loan to their employer in exchange for tax deferral. Consequently, if the company were to become insolvent, any assets set aside for funding the NQDC would be subject to their creditors.

While this may sound like an outlandish scenario, these plans can and do sometimes fail to pay out the balances due to participants. For those already heavily invested in their employer’s stock, these plans can cause some to unwittingly double down on the idiosyncratic risks of their company.

How To Decide What is Optimal for You

Determining the right course of action when it comes to NQDCs can be complex. The optimal answer will depend in large part on the nuances of your tax situation both pre and post retirement. It’s important to consider legislative changes that could impact marginal tax rates, and to examine the creditworthiness of the company you work for, and how long you are willing to be exposed to these risks. Many companies allow employees to take their distributions over a number of years post-retirement. While this may be beneficial from a tax standpoint, you should reflect on how comfortable you are with having a substantial portion of your retirement savings tied up in an unsecured loan with a company that you no longer work for.

One helpful way to frame the pros and cons is to come back to our analogy of viewing the NQDC plan as a loan to your employer; the excess growth generated by the tax efficiency of this strategy could then be viewed as equivalent to interest on your loan. Viewed this way, the excess ending value of $48,000 after 20 years, on a starting balance of $100,000, would equate to roughly a 2% interest rate. Considering that 20 Year treasury bonds are currently yielding almost 4%, it would appear most NQDC participants are not receiving a sufficient return on a risk-adjusted basis.

To help you determine whether participation in your company’s NQDC is appropriate for you, we’ve developed the following checklist to use as a guide:

- How heavily concentrated are you in your employer’s stock? Are you comfortable with greater exposure to the risks of the company?

- Are you comfortable with the financial position of the company?

- Are you contributing the maximum amount to your 401(k)?

- 401(K)s allow for the same tax-deferred growth of a NQDC, but without the risk of default by your employer. One should only consider participating in a NQDC if they are already maxing out their 401(K).

- Are you eligible for an HSA? If so, are you contributing the maximum dollar amount and investing the funds?

- HSAs provide for the best of both worlds: A pre-tax contribution and a tax-free withdrawal if used for eligible medical expenses. We often encourage clients to invest the funds in their HSA and to use it for medical expenses in retirement. If you are eligible for an HSA, contributions to this account should generally take precedence over contributions to a NQDC.

- Does your 401(k) allow for non-deductible contributions and in-plan Roth conversions?

- Some plans will allow you to contribute on an after-tax basis and convert these contributions to Roth (often referred to as a Mega-Backdoor Roth Conversion). We recommend working with your advisor to determine whether this strategy is appropriate based on your current tax bracket and expected bracket in retirement. For those who anticipate that they will still be in a high bracket post-retirement, it is generally prudent to prioritize this strategy over NQDC contributions.

- Are you satisfied with your portfolio’s exposure to alternative asset classes?

- Your NQDC will have a limited list of investment options, so for those who have not achieved their diversification objectives in asset classes like private equity/debt or real estate, it may be prudent to prioritize taxable assets you can deploy into a wider range of investments.

- Do you have significant charitable goals that you are seeking to achieve with your wealth?

- For those who fall into this category, you may be able to accomplish the goal of tax deferral using a Flip CRUT.

Please reach out to your Coldstream wealth management team to help answer questions on this topic or any others that should arise along your wealth planning journey.

[1] Coldstream target annualized rate of return for a long-term balanced investment objective portfolio, rounded to nearest whole number.

[2] Current tax rates for 2023

DISCLAIMER: THIS ARTICLE HAS BEEN PROVIDED FOR INFORMATIONAL PURPOSES ONLY AND SHOULD NOT BE CONSIDERED AS INVESTMENT ADVICE OR AS A RECOMMENDATION. THIS MATERIAL PROVIDES GENERAL INFORMATION ONLY. COLDSTREAM DOES NOT OFFER LEGAL OR TAX ADVICE. ONLY PRIVATE LEGAL OR TAX COUNSEL MAY RECOMMEND THE APPLICATION OF THIS GENERAL INFORMATION TO ANY PARTICULAR SITUATION OR PREPARE AN INSTRUMENT CHOSEN TO IMPLEMENT THE DESIGN DISCUSSED HEREIN. CIRCULAR 230 NOTICE: TO ENSURE COMPLIANCE WITH REQUIREMENTS IMPOSED BY THE IRS, THIS NOTICE IS TO INFORM YOU THAT ANY TAX ADVICE INCLUDED IN THIS COMMUNICATION, INCLUDING ANY ATTACHMENTS, IS NOT INTENDED OR WRITTEN TO BE USED, AND CANNOT BE USED, FOR THE PURPOSE OF AVOIDING ANY FEDERAL TAX PENALTY OR PROMOTING, MARKETING, OR RECOMMENDING TO ANOTHER PARTY ANY TRANSACTION OR MATTER.

Related Articles

July 9, 2025

The “One Big Beautiful Bill”: Key Tax Provisions

June 27, 2025

Diversified Estate Planning for LGBTQ+ Families

June 20, 2025

Incorporating a “Die with Zero” Philosophy into Your Long-Term Financial Plan