Insights

February 1, 2023

Reflecting on 2022’s Respect for Marriage Act: How does it impact the lives and finances of American same-sex marriages?

In LGBTQIA+, Wealth Strategy

On December 13, 2022, the Biden Administration passed the Respect for Marriage Act. Thinking about our clients who are impacted, we wanted to offer perspective on what this means today and for the future.

To provide context, let’s look at the relevant legal history of the subject over the past few decades:

- The Defense of Marriage Act – “DOMA” (1996); restricted the federal recognition of marriage to opposite-sex couples only, defining “marriage” as between a man and a woman, and a “spouse” as a person of the opposite sex.

- United States v. Windsor (2013); the United States Supreme Court determined that DOMA’s restricted definition of “marriage” and “spouse” was unconstitutional.

- Obergefell v. Hodges (2015): the Supreme Court ruled that all states must allow same-sex couples to marry and must recognize same-sex marriages lawfully performed in other jurisdictions.

- Respect for Marriage Act – “RMA” (2022); Signed into law by President Biden, this act provides statutory authority for same-sex, interracial, and international marriages, replacing DOMA provisions restricting the definitions of “marriage” and “spouse,” with the provision that every state must recognize a marriage between two persons that is legally issued under the laws of any other state.

The Respect for Marriage Act codifies aspects of Windsor and Obergefell, mandating that individual states fully recognize legal marriages performed in other states and may not discriminate or inhibit favor of federal rights based on gender, race, ethnicity, or spousal nationality, regardless of future Supreme Court rulings on the matter.

One driving factor behind the bipartisan support of the Act is the stipulation that the RMA does not minimize or rescind religious expression, and will not require nonprofit religious organizations to provide services or accommodations for the affirmation or sanctification of marriages that are contrary to their religious beliefs. Simply put, same-sex marriages are protected nation-wide at the federal level, while religious entities remain entitled to perform marriages based upon their beliefs.

In review, the Respect for Marriage Act:

- Requires all states to recognize legal marriage licenses from other states on a federal level.

- Protects Federal Rights and Privileges in the Full Faith & Credit Clause of the constitution for all legal marriage licenses, in all states, regardless of individual state laws limiting their definition of marriage.

The Respect for Marriage Act does not:

- Affect religious liberties or conscience protections that are available under the Constitution or federal law.

- Compel religious organizations to provide goods or services to formally recognize or celebrate a marriage.

- Require individual states to grant marriage licenses to same-sex couples.

- Affect any benefits or rights that do not arise from a marriage, or recognize under federal law any marriage between more than two individuals.

If Obergefell was overturned today

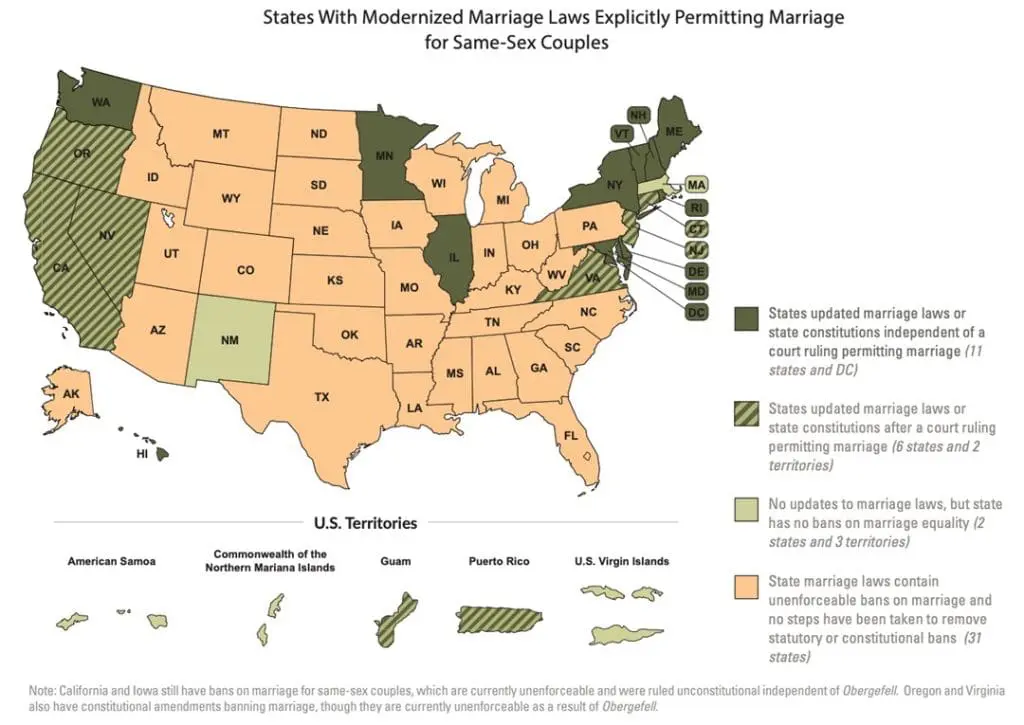

Without the RMA, many states would not be required to recognize or guarantee the rights and privileges of marriage provided by the United States to LGBTQ+ couples who were married in other states. The states that do have protections for same sex marriages, however, would still issue and recognize same-sex marriage licenses, with Washington and Oregon states protecting the Pacific Northwest region.

The federal government does not have the power to define marriage for the purpose of the states, but it does have the power to require that all states recognize same-sex, interracial, and international marriages equally in respect to the law and the Full Faith and Credit clauses of the Constitution. Should Obergefell be overturned, states will not be federally mandated to issue same-sex marriage licenses but will still be federally obligated to treat same-sex marriages issued by other states equitably, because of the RMA.

This map highlights where same-sex marriages would still be granted licenses in the USA if Obergefell is overturned:

How does this affect you and your communities financially?

This protection extends the rights and privileges of marriage granted by the federal government, including but not limited to:

- Employee benefits such as favorable tax treatment for employer-provided spousal health coverage, life insurance options, increased FSA/HSA contributions, and other rights under COBRA and HIPAA

- Social Security benefits

- Pension, annuity, and retirement plan benefits

- Eligibility for the Family and Medical Leave Act (FMLA) and bereavement leave

- Equitable tax treatment on annual tax returns filed jointly, estate tax marital deductions, and gift tax deductions

- Rights in consideration of custodianship / guardianship or adoption of children

- Priority for hospital visitation and medical decisions

- The ability to sponsor a spouse for citizenship

- Representation under the Full Faith and Credit Clause of the Constitution that requires all state courts respect the laws and judgements of courts from other states

There are currently no immediate changes that must be implemented to financial plans

The Respect for Marriage Act is a precautionary layer of protection, should the Supreme Court take a case that could potentially overturn the Obergefell ruling. The RMA safely assures that legally married same sex couples will be entitled to the federally backed rights and benefits detailed above, regardless of future action taken by the Supreme Court or where they live and work within the USA.

While we still have a way to go towards bona fide nation-wide marriage equality in America, this Act is arguably one of the biggest legislative victories for the LGBTQ+ population in modern US history. The recent words from Director-Counsel Janie Nelson of the Legal Defense Fund are important to note: “Anything less than full equality for couples is the equivalent of relegating LGBTQ+ people and interracial couples to an inferior status in our nation. And, as we have seen all too often, perceiving a group of people as inferior leads to hateful speech, discriminatory laws, and violence intended to intimidate and terrorize marginalized people and their communities.”

With Inclusion and Diversity as one of our organization’s core values, we remain committed to providing guidance and support for our LGBTQ+ clients. Knowing that politics and legislation can instantly change the protections and opportunities for the LGBTQ+ community, our mission is to ensure that your financial life remains a constant source of stability, flexibility, and that it honors your values.

As we see developments in this area, our LGBTQ+ Wealth Strategy Group at Coldstream will work hard to examine how legislative changes could impact our LGBTQ+ friends and families, and make sure they are equipped to navigate the evolution of law to remain informed, empowered, and protected.

Related Articles

May 28, 2026

Building a Financial Foundation: Books for Young Adults

May 15, 2026

Irrational Decisions in Investing

April 29, 2026