Insights

October 25, 2021

Permanent or Temporary: The Economic Impact OF COVID-19

In Market Commentary

Although the COVID-19 induced recession last year was short-lived, the on-going effects of COVID-19 on the global economy persist. Prior to the pandemic, the U.S. inflation rate was contained; GDP growth, though positive, was struggling to rise above 2% annually; the super-cycle of commodity price declines was continuing; global supply chains were robust, despite the U.S./China trade war; “just in time” inventory was a management imperative; there was a strong demand for downtown office space and tiny apartments; a very small percentage of the workforce worked remotely; corporate profitability was unexceptional, employment was robust, and labor had little bargaining power. The amount of change the pandemic has caused in a year and half is stunning. The great unknown is what, if any, of these changes will be a permanent feature of the U.S. economy going forward.

In particular, the length of time that three of these changes continue will greatly influence the direction of the U.S economy and markets going forward: higher inflation, stronger economic growth, and increased corporate profitability. To date, these changes have resulted in the equity markets rising sharply this year, with the S&P 500 up 15.92% through the third quarter, and the bond market, as measured by the Bloomberg Barclays U.S. Aggregate Index, declining 1.55% due to the rise in interest rates (typically, the price of bonds moves in the opposite direction of interest rates) stemming from both inflation concerns and economic growth.

The increase in the inflation rate this year has been substantial. Over the 12-month period ending September 30, 2021, the Consumer Price Index (“CPI”), increased by 5.4%. Much of the increase can be attributed to supply chain bottlenecks, which have resulted in higher prices for both raw materials and finished products.

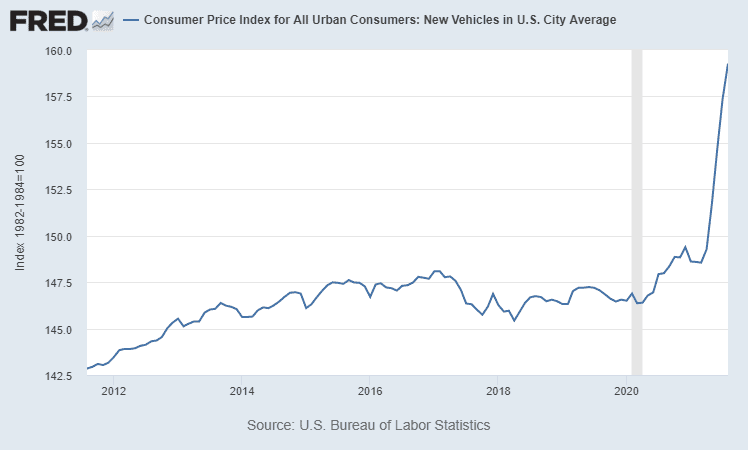

Perhaps the most publicized of these bottlenecks is in new cars, which have been caused, at least in part, by a worldwide scarcity of the computer chips necessary to make them. This shortage coupled with increased demand as the economy rebounded has resulted in soaring prices.

New Car Price

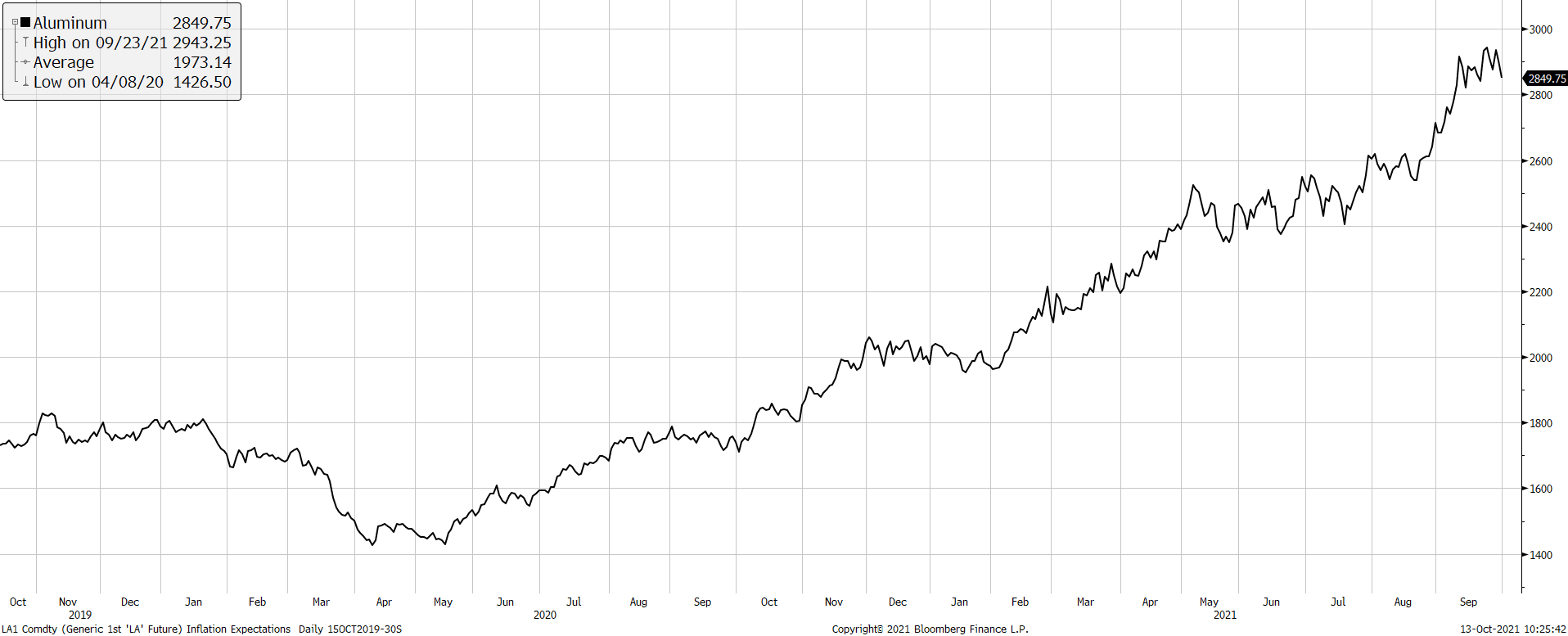

This increase in demand, along with limited available supply, has led to an increase in the commodity prices necessary to manufacture cars as well.

Aluminum Futures Price

Source: Bloomberg

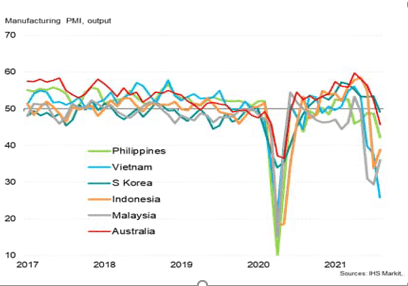

Beyond cars, the spread of the Delta variant in the third quarter of 2021 has exacerbated supply chain issues in many manufactured products, as the spread caused the shut-down of many manufacturing plants in Southeast Asia.

Asia Manufacturing

Source: IHS Markit

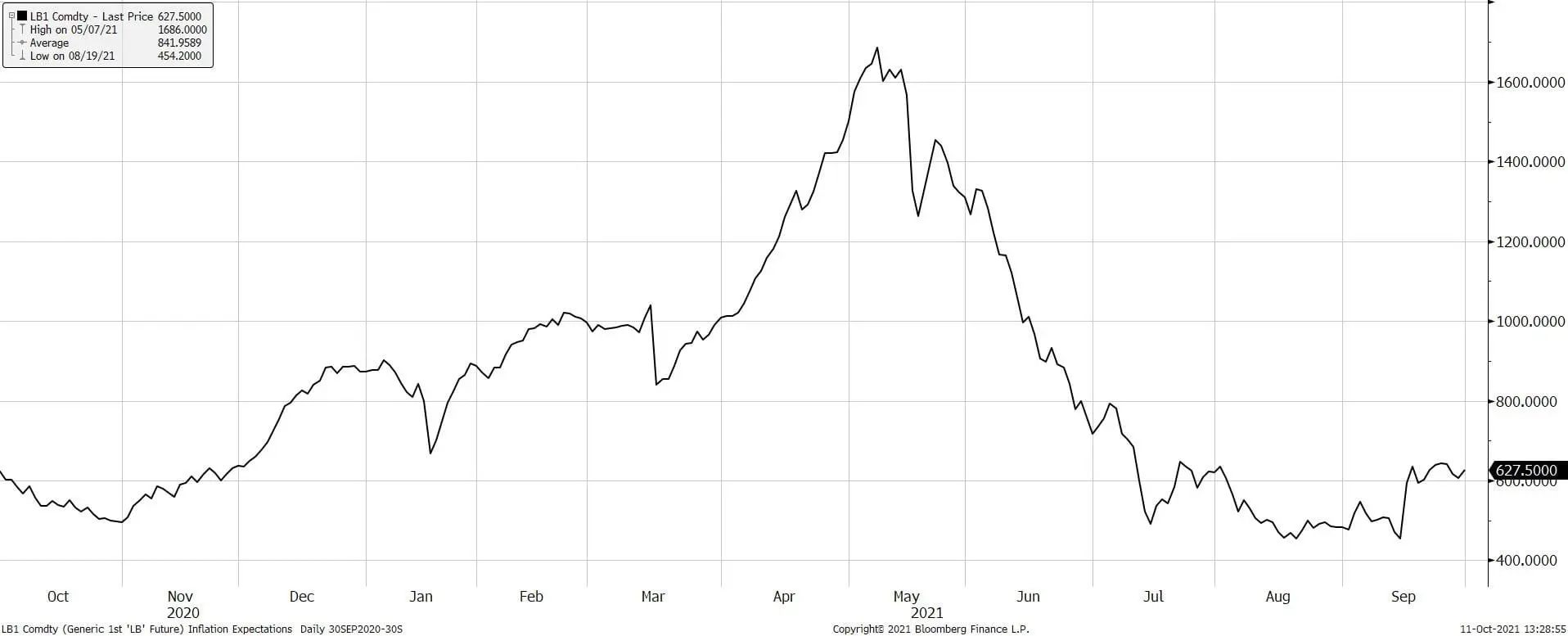

This perfect storm of lack of supply, increased demand, and additional COVID-19 shut-downs should resolve itself over time. And we would not be surprised to see the current bottlenecks in commodities and goods resolve itself, although not immediately. Once it does get resolved, prices can decline quickly, as we have seen in lumber prices.

Lumber Futures Price

Source: Bloomberg

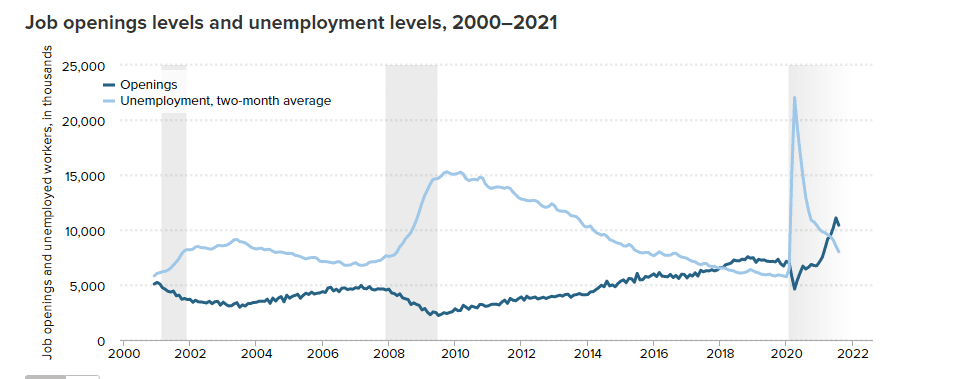

In addition to the higher prices for goods, a significant increase in wages as a result of changes in the labor market stemming from the impact of COVID-19 has contributed to inflation. The problem is easily identifiable: there are simply more job openings than workers willing to fill them, so companies have had to raise wages to attract workers. We have heard a variety of explanations for this occurrence, including: a lack of available child-care preventing people from coming to work, increased unemployment benefits providing a disincentive to work, people establishing different priorities due to the pandemic, especially for workers near or at retirement age, and a mis-match in the jobs that are open and the skills needed to fill those jobs. We suspect all of these factors contribute to some extent. Some will be easily resolved and others not. For example, increased unemployment benefits are expiring, but the skills/workers mismatch will take longer to resolve. While wages per se are not a part of the CPI, they affect almost all other aspects of that index.

U.S. Job Openings and Unemployment

Source: US Census Bureau

Although the U.S economy is experiencing inflationary pressures currently, those pressures must be considered in conjunction with long-term deflationary pressures, most notably demographics, as the U.S population is aging. We have seen what an aging demographic has done to Japan’s and developed Europe’s economies; it has slowed both growth and inflation as fewer workers must support more retirees.

This mix of shorter-term inflationary pressures and longer-term deflationary pressures has resulted in indicators of long-term inflation expectations to center around 2.5%, as of the end of September. While forecasting longer-term inflation is fraught with uncertainty, the markets’ view seems reasonable: slightly higher inflation than the U.S has experienced since the Great Financial Crisis but nothing like late 1970s inflation levels.

Similarly, growth and corporate profitability have been much higher than historical averages this year, but the fact that these gains are measured on a year over year basis and growth and profitability were slow last year is a significant contributor to these gains. We would not be surprised if growth and corporate profitability return closer to their historical averages next year.

While the U.S. economy has undergone at least temporary changes, we do not think significant changes to clients’ portfolios are warranted. The principal of diversification still applies. Diversification allows clients to participate in a market rally, but limits losses in a market correction. For example, while many currently believe that it is a certainty that interest rates will rise further, many have made that claim for the past ten years and if they placed all of their “eggs in that basket,” their portfolios would have badly underperformed. Prognosticators are often wrong, but diversification protects your portfolio and enables you to realize your financial goals through market cycles.

We greatly appreciate your trust in us. If you have any questions or comments you would like to share, please contact your Relationship Manager, Portfolio Manager or me. Thank you.

Sincerely,

Howard Coleman | Chief Investment Officer and General Counsel

Insights Tags

Related Articles

April 13, 2026

Watch Coldstream’s MarketCast for Second Quarter 2026

April 9, 2026

Turbulence: Navigating a Complex First Quarter

January 29, 2026

Artificial Intelligence: Boom or Bubble?