Insights

January 16, 2020

Market Update: 2019 Recap and 2020 Outlook

In Market Commentary

Best wishes for a happy, healthy, and prosperous New Year. As 2020 begins, we wanted to provide you with: (1) a 2019 financial market review, (2) a snapshot of where we are currently, and (3) some thoughts going forward.

YEAR IN REVIEW

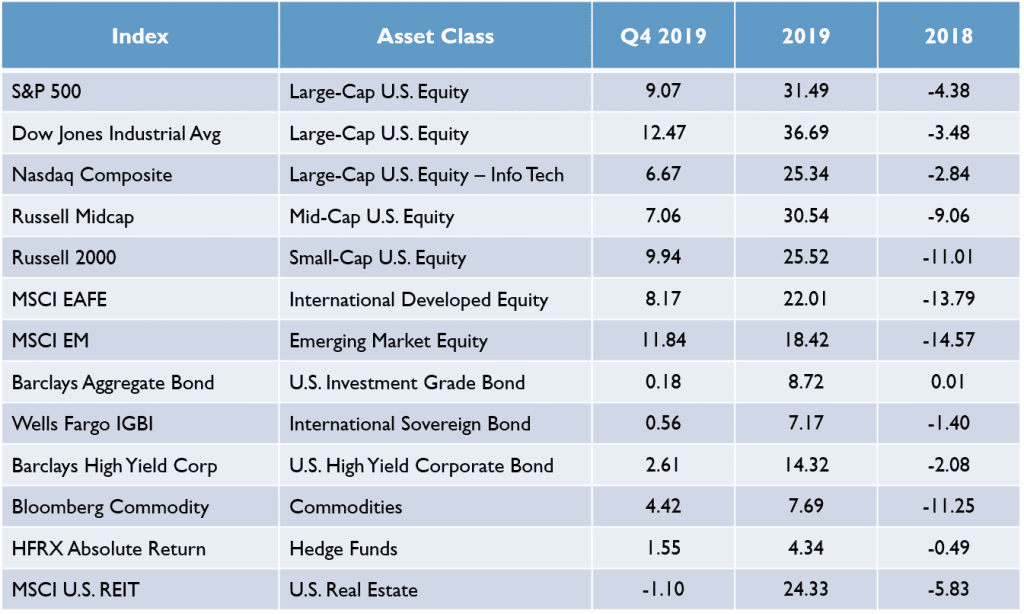

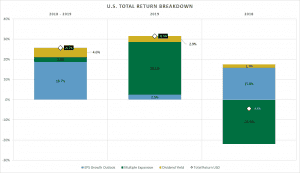

2019 was a stellar year for virtually all asset classes with the S&P 500 leading the way, providing a total return of 31.49% for the year. However, the gain in US equities was not due to an increase in corporate profitability, as S&P 500 earnings per share (EPS) are estimated to have increased by only 2.5% for the year. Instead, the rally was primarily driven by an expansion in equity valuation multiples (the ratio of a corporation’s stock price to its annual earnings), which increased by approximately 26% in 2019. Put simply, the US equity market became more expensive in 2019.

However, 2019 financial results should not be viewed in isolation from 2018. In that year, virtually every asset class posted losses, with the S&P 500 down 4.38% and the MSCI Emerging Market Index down 14.57%.

Source: Bloomberg

In contrast to tepid US corporate profitability in 2019, US corporate profitability was strong in 2018, with S&P 500 EPS increasing 15.8%, but the index’s valuation multiple decreased 21.9% and drove its total return into negative territory.

Source: J.P. Morgan

2018’s sharp contraction in valuation multiples reflected investor pessimism about future earnings growth, an outlook that reversed abruptly in 2019. While it is impossible to precisely determine the ingredients that constitute the stew of factors that move markets, it appears that two main ingredients were responsible for financial markets being negative in 2018 and positive in 2019: the Fed and trade policy. In 2018, the Fed steadily raised the Fed Funds rate four times, starting the year at 1.5% and ending the year at 2.5%. These sequential rate hikes progressively spooked financial markets, with the final December 2018 rate hike causing significant volatility in both equities and fixed income. Market participants feared that the Fed was moving too quickly and that higher interest rates could choke off the economic expansion.

Contrast this to 2019, when the Fed became increasingly accommodative over the course of the year, cutting the Fed Funds rate three times, and, in September, making outright purchases in the Treasury market once again (a practice it previously stopped in 2017) to replace maturing Treasuries on its balance sheet. These accommodative actions by the Fed resulted in a belief by market participants that interest rates would remain low, providing a tailwind to the ongoing economic expansion, despite tepid corporate profitability.

Source: St. Louis Fed

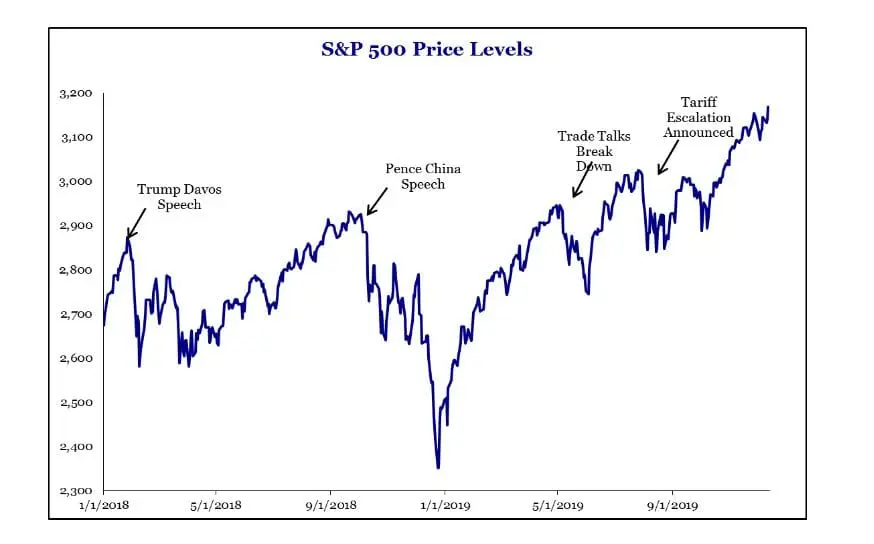

Markets also reacted to the twists and turns of the US trade dispute with China. As this trade dispute appeared to ease in the latter part of 2019, equity markets rallied globally. This is most apparent in the strong equity rally at the end of the fourth quarter of 2019 as the “Phase 1” China deal became more probable. Not only did news surrounding the trade dispute cause broad directional movements in the equity markets, it also caused significant short-term volatility, as demonstrated by the chart below:

Source: Strategas

WHERE ARE WE NOW?

The strong US equity returns in 2019 coupled with relatively weak corporate profitability have resulted in equity valuations above their historical average.

Source: J.P. Morgan

These valuations are, in part, due to optimism about increased corporate profitability in 2020. Equity analysts are predicting an approximately 10% increase in corporate profitability next year. The optimism surrounding corporate profitability appears to be due not only to the two factors discussed above (the Fed and trade), but also to decreased regulation, the ongoing effects of the tax cuts, the “green shoots” of economic improvement in Europe, and the lack of a “hard” Brexit. Additionally, interest rates remain historically low and range-bound and corporations generally have ready access to the capital markets.

Source: FactSet

THOUGHTS ON 2020

As is always true, we enter the year looking at a mix of factors that could cause equity markets to either rise or fall in the short term. Geopolitical events such as trade, the US elections, Iran, and potential tariffs on Europe could all cause significant market volatility. But it is impossible to predict how these events will play out.

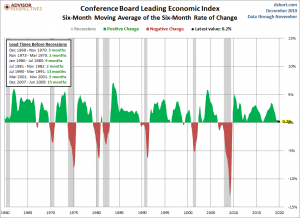

As we have discussed in previous letters, our focus continues to be on economic fundamentals. Geopolitical events do have an impact on short-term volatility, but it is how those events affect the economy fundamentally that have more important investment implications in the medium- and long-term. We monitor many signals to understand economic fundamentals, but historically the Conference Board’s Leading Economic Index (LEI) has been the most reliable predictor of a recession. The US has never gone into a recession without the LEI turning negative. Currently, the LEI that we monitor is still slightly positive, reflecting the slow growth environment the US experienced in 2019.

Source: Advisor Perspectives

Additionally, given how equity valuations are somewhat stretched, corporate profitability will most likely be an important issue for equity markets in 2020, and we will be closely following this important factor.

However, we cannot emphasize enough that the best protection in the event of a market decline is not to make major tactical shifts in an investment portfolio based on the events of the day, but rather to begin with a portfolio constructed of diversified investments in stocks, bonds, and if you are comfortable doing so, alternatives. This type of portfolio is designed to allow you to participate in the upside of a market rally, while cushioning the portfolio in an equity sell-off. We can and will tilt portfolios if and when we see economic fundamentals change. However, those changes will not affect the overriding principal of portfolio diversification.

If you have any questions or comments, please feel free to contact me, your relationship manager, or your portfolio manager.

Sincerely,

Howard Coleman

Chief Investment Officer and General Counsel

Insights Tags

Related Articles

April 13, 2026

Watch Coldstream’s MarketCast for Second Quarter 2026

April 9, 2026

Turbulence: Navigating a Complex First Quarter

January 29, 2026

Artificial Intelligence: Boom or Bubble?