Insights

April 12, 2021

Market Commentary: ALL ABOARD!

In Market Commentary

April 12, 2021

THE US ECONOMY

What a difference a year makes. After some glitches early on, the vaccine roll-out in the United States appears to be going well, especially when compared to the roll-out in the great majority of other countries. As the US has begun to control the spread of the virus, the US economy has started to open again, despite some concerns about COVID-19 variants and a “fourth wave”. We expect that this opening up will be reflected in the 2021 GDP growth rate, which the consensus of economists estimates will be about 6%, the largest year-over-year GDP increase since 1984. It is important to remember, however, that this is a year-over-year comparison and last year’s GDP was negative.

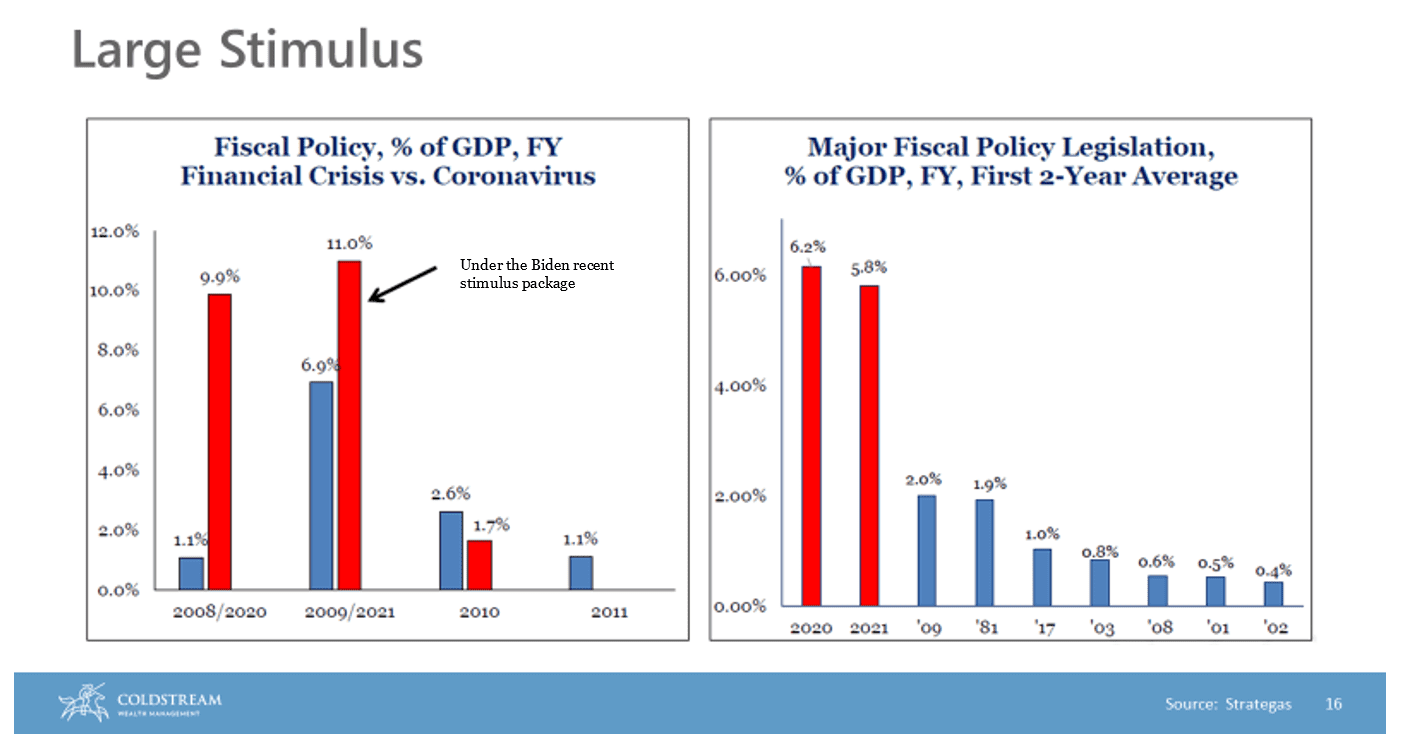

A significant factor in the ability of the US economy to rebound from the COVID-19 induced recession has been the unprecedented amount of fiscal stimulus Congress has poured into the US economy. To recap, in March 2020, Congress passed a $2 trillion dollar rescue package. In December 2020, it passed another $900 billion package, and, just last month, Congress passed another $1.9 trillion stimulus package – a total of almost $5 trillion in support/stimulus funds to sustain and bolster the economy, far greater than the stimulus passed during the Great Financial Crisis of 2008 or any other post World War II period.

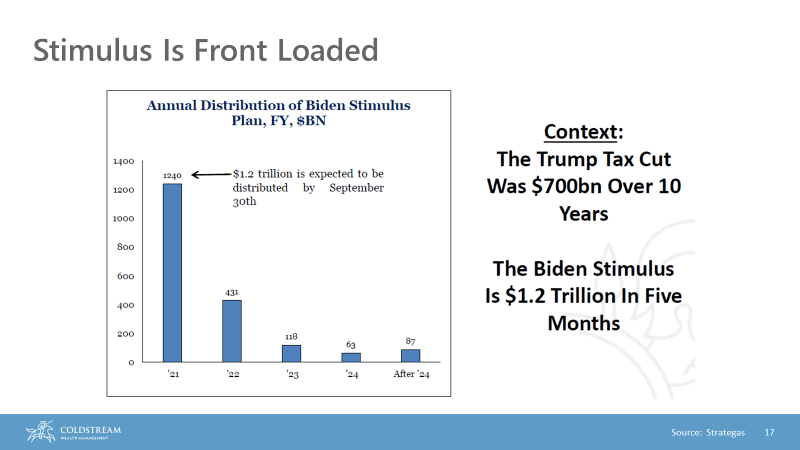

In addition, the recently passed stimulus package is front loaded, with the great majority of benefits being distributed by the end of the third quarter of this year.

In addition to Congress’ fiscal stimulus, the Fed has continued to provide its own monetary stimulus: it has kept its overnight lending rate at or close to 0 and is continuing to buy government debt through its Quantitative Easing (QE) program. Low rates spur corporate, consumer, and mortgage borrowing, which in turn spurs economic growth. With the economy, on its own, reviving from very low levels, with Congress passing massive fiscal support, and with a very dovish Fed, it is no surprise to see strong economic growth projections.

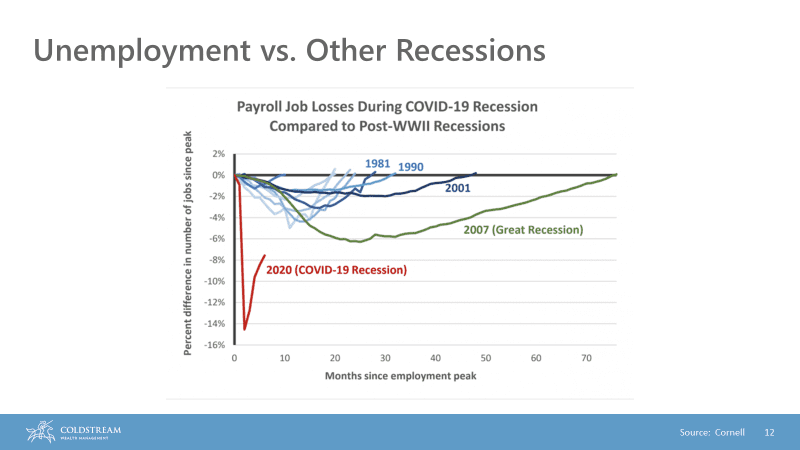

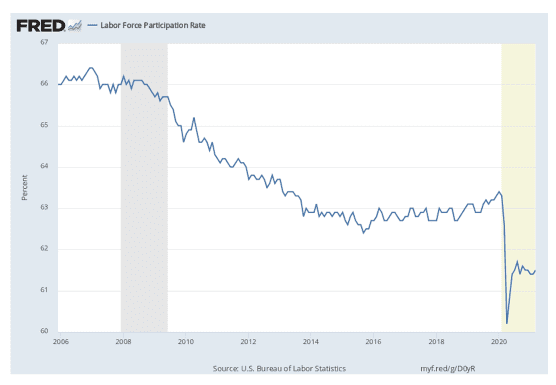

In explaining why the Fed should maintain such low rates in the face of what appears to be strong economic growth, Fed Chair Powell points out that although the unemployment rate has fallen from over 14% to 6%, 6% is still an elevated rate. In addition, the percentage of people participating in the jobs market has significantly declined and initial claims for unemployment also remain elevated.

Labor Force Participation Rate

The Fed believes this data indicates that there is still significant “slack” in the US economy.

All of this leads to the obvious question: isn’t all this stimulus in an economy growing on its own inflationary? The current consensus (including from the Fed) is that we will see a significant pick-up in inflation this year. The debate is whether this inflation will be temporary – will it decline again after the fiscal stimulus passes through the US economy and the year-over-year comparisons to 2020 fall away. The Fed and many economists believe so; however, this belief is far from uniform and those concerned about the inflationary effects of the massive stimulus include economists on “both sides of the aisle.” So far, financial markets seem not too concerned. Long term inflation expectations currently hover between 2 and 2.5%, which is right in line with the Fed’s target. Of course, these expectations can change quickly.

FINANCIAL MARKETS

In the first quarter, financial markets reflected the optimism surrounding a US economic recovery, as the rally in US equities continued. However, while the rally off the March lows of last year was led by big tech, the first quarter rally was led by small cap stocks, which gained a remarkable 18.24% in the quarter, an indication of the anticipated recovery of “Main Street”. Gains in tech, as reflected by the NASDAQ index, were muted on a relative basis, but not on an absolute basis, as the NASDAQ rose 2.95%. And the S&P 500 index rose 6.17%.

While equities rallied on the anticipated recovery, bonds sold off. Anticipated growth and the specter of some inflation drove Treasury yields higher (which results in lower bond prices), and the bond market as measured by the Bloomberg Barclays Aggregate US Bond Index declined by 3.37%. Although rising significantly, interest rates are still low by historical standards, and the rising rates did not reach a level that spooked equity investors.

WHERE FROM HERE

So far this year, there has been both robust economic growth and rising equity markets in the US. We anticipate growth to continue to rise for most of this year given fiscal stimulus, a dovish Fed, and a US economy that should continue to re-open. But a stronger US economy does not necessarily translate into a rising equity market. Currently, equity valuations are very high by historical standards, which could put some restraint on how high equities can go and has some analysts believing that the recovery is already built into equity prices. However, corporate profitability continues to exceed expectations, which could result in valuations looking a bit more reasonable. In addition, upward equity momentum is strong and trying to time exactly when that momentum will reverse is difficult at best.

With valuations at these levels, we would not be surprised if we see an equity market correction this year; however, current economic conditions do not indicate that equities will fall into a bear market in the near future. Oftentimes, the Fed eliminating stimulus or raising rates is a catalyst for a market decline. While we would be surprised if this happens in 2021, it remains a possibility for 2022, especially if inflation expectations change.

What does all this mean for your portfolio? It shows the benefits of diversification. Although bonds lost money this quarter, they should do well if economic growth fails to meet expectations, which should help offset potential losses in equities. The fact that stocks and bonds often react differently to economic scenarios demonstrates why in most instances, it is important to have both in a portfolio. While we customize client portfolios, we tweaked most portfolios in the fall of last year and early this quarter by adding some positions that would benefit from a growing economy, while still maintaining broad portfolio diversification.

As always, we thank you for your confidence in us. If you have any questions or comments, please feel free to contact your Relationship Manager, Portfolio Manager or me.

Best Regards,

Howard Coleman | Chief Investment Officer and General Counsel

Insights Tags

Related Articles

April 13, 2026

Watch Coldstream’s MarketCast for Second Quarter 2026

April 9, 2026

Turbulence: Navigating a Complex First Quarter

January 29, 2026

Artificial Intelligence: Boom or Bubble?