Insights

January 19, 2021

Market Commentary: A Year Like No Other

In Market Commentary

January 19, 2021

First, and most importantly, we hope you are safe and doing well, and we look forward to being able to see many of you in person in 2021.

Since March, financial markets and the global economy have been dominated by the spread of COVID-19, the curtailment of economic activity, and the massive governmental response. As the virus surged in March, Congress reached rapid bipartisan agreement on a massive fiscal package to support the US economy. The Fed also acted quickly and aggressively in providing the most comprehensive package ever of monetary support to financial markets and the US economy. Unlike the political polarization that occurred over the course of the year, the fiscal package response was wholly bipartisan, passing 96-0 in the Senate and by voice vote in the House. It significantly softened the economic blow caused by COVID-19. Equity markets rebounded, corporations were able to issue cheap debt to avoid cash shortfalls, Americans below a certain income level received direct payments, and the unemployed received financial support. In addition, the housing market benefitted from both low interest rates and a moratorium on foreclosures for homeowners who were delinquent on their mortgage payments.

Currently, the economic curtailment and governmental support has created a unique set of market and economic dynamics.

THE IMPACT OF FISCAL SUPPORT

While the unemployment rate has remained elevated, personal income and savings are higher than they were pre-pandemic due to governmental support through increased unemployment benefits and other transfer payments. Additionally, the concentration of low wage workers among the unemployed, had less of an impact on total income and savings than if high income workers lost their jobs, resulting in the odd combination of both high unemployment and an increase in total income.

Personal Savings

While the personal savings rate has declined from its highs, economists expect it to rise again after the additional December stimulus package gets distributed.

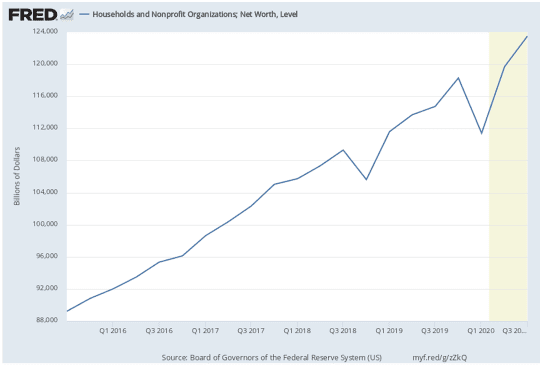

Net Worth

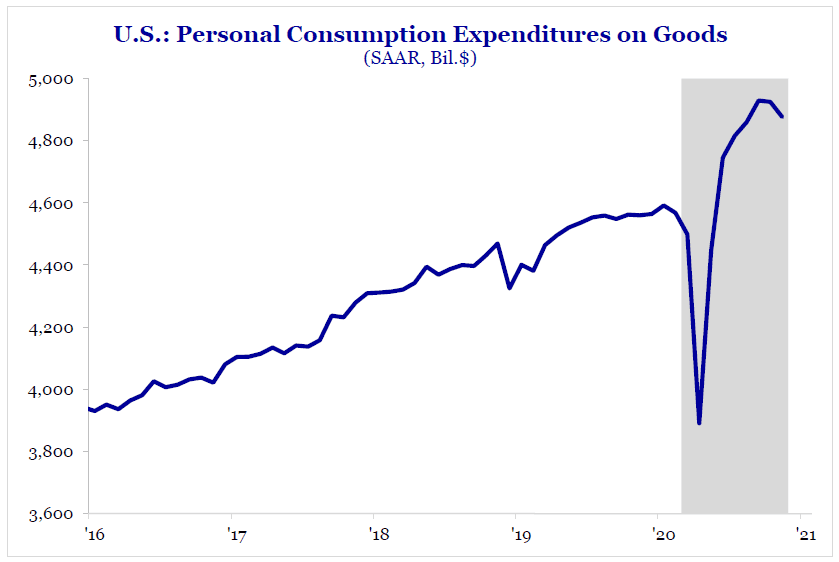

Because income and savings were not affected for many Americans, spending on goods in the latter part of 2020 exceeded pre-pandemic levels.

Source: Strategas

Source: Strategas

Similarly manufacturing, which produces goods, also returned to pre-pandemic levels.

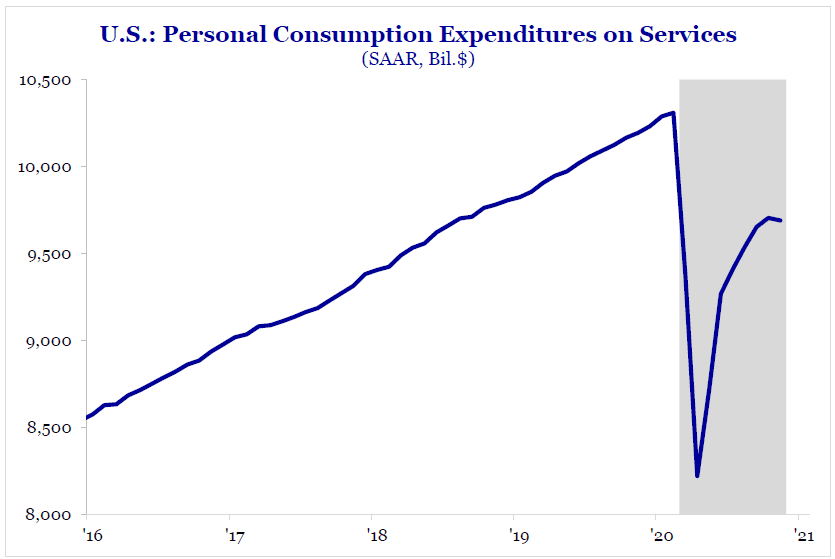

However, consumers have not spent nearly as much on services, which represent about 70% of US GDP, as they did prior to the pandemic. Spending on restaurants, hospitality, transportation etc. plummeted.

Source: Strategas

Source: Strategas

THE IMPACT OF MONETARY SUPPORT

The Fed instituted a suite of measures, which supported both the financial markets and the economy. For example, the Fed took the Fed Funds rate (the overnight borrowing rate for banks) to zero and indicated that it would remain at zero for the foreseeable future. These low rates encouraged borrowing, which supports economic growth.

The Fed also ramped up its Quantitative Easing (QE) program, whereby the Fed buys Treasuries. QE keeps Treasury rates low and indirectly spurs the housing market, as the interest rates paid on mortgages bear a close relationship to the interest rate paid on 10-year Treasuries. The Fed also declared an intention to buy both investment grade and certain high yield bonds. The mere announcement of this backstop caused the interest rates on corporate bonds to tumble and enabled many corporations badly in need of cash to borrow money at very low interest rates. The Fed initiated numerous other measures to support individuals and businesses through the crisis.

THE EFFECT OF FINANCIAL MARKETS

In large part due to these fiscal and monetary measures, both the US equity market and bond market staged remarkable rallies off their March lows. The 2020 total return for US large cap stocks as measured by the S&P 500 was 18.40%, and total return for US bonds as measured by the Bloomberg Barclays US Aggregate Bond Index was 7.51%.

The steep and swift equity decline into a bear market in March was followed by a swift and steep recovery, which occurred in two phases. In the first phase (referred to as the “stay at home” trade), stocks of the big tech companies which benefitted from people staying home rallied, resulting in gains in the S&P 500. Although the rally was not broadly spread across the market, these large tech companies represented over 20% of the index, resulting in the index showing gains as well.

In the latter part of the year, investors began to anticipate a return to a “normal” economy, and the “recovery trade” replaced the “stay at home” trade. This part of the rally was more broad-based than the “stay at home” rally and particularly benefitted small cap stocks, which arguably more closely represent the US economy as a whole. These small cap stocks declined significantly more than large caps in March, but their recovery from the March lows outpaced the large cap recovery: The Russell 2000 gained 19.96% for the year, comparable to the gain in large caps, but rallied 99.05% off its March lows.

As to fixed income, the Fed’s intervention in the market kept interest rates low and spreads tight. (“Spreads” are the difference between the interest you would receive on a corporate bond over what you would receive for a Treasury bond – it is a measure of corporate bond risk: tight spreads = less perceived risk). This enabled corporations to borrow cheaply and led to a strong rally in the bond market as well.

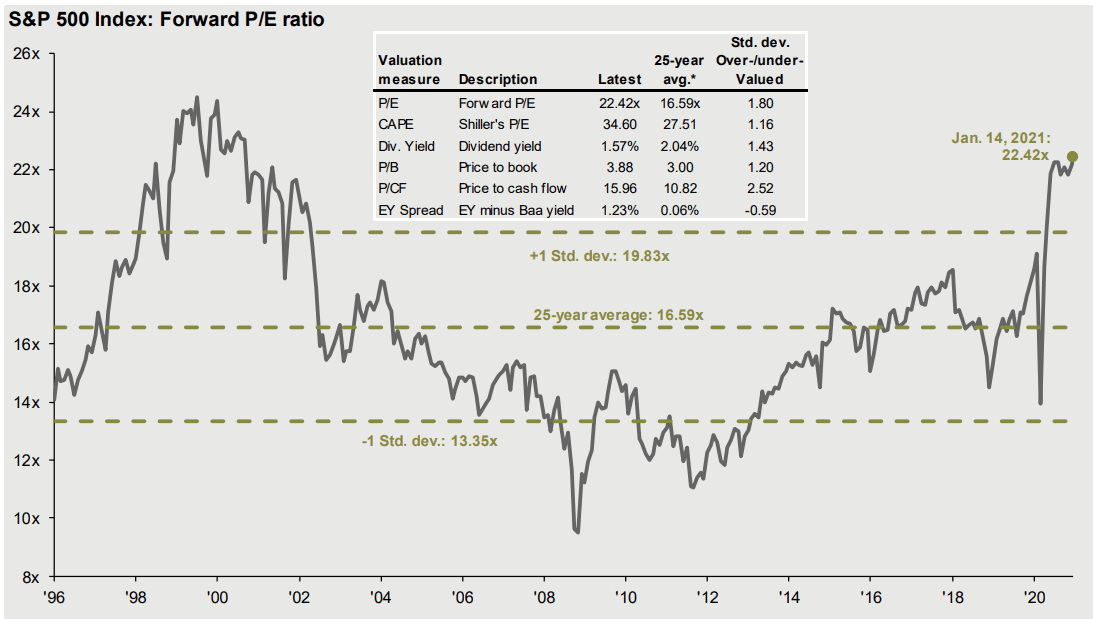

Currently, stocks and bonds are expensive. Equity valuations are frothy and bond yields are low.

Equity Valuations Far Above Historical Averages

Source: JP Morgan

Investment Grade Spreads Historically Tight

Source: JP Morgan

Source: JP Morgan

LOOKING FORWARD

It is widely anticipated that the US economy will grow quickly later this year as the vaccine becomes widely distributed. The consensus view is that a significant portion of the abundance of savings Americans have accumulated will be spent on services, which will spur GDP growth to significantly higher levels than the US economy has experienced in the recent past, for at least a few quarters. Service businesses such as restaurants, bars, hotels, and airplanes should experience strong demand as the health risk subsides and people feel safe gathering again. It is unknown what level GDP growth sustains after the anticipated surge, as is the long-term effect of the massive accumulation of governmental debt on long term growth.

As to the financial markets, it is extremely difficult to predict what markets will do in the short run, and we are not in the business of day trading portfolios. However, there has been strong positive momentum in the equity markets that has resulted in a departure from traditional measures of fundamental value.

In most years equity markets experience corrections, and we would not be surprised if we experience one during the course of this year as well. However, bear markets rarely occur when the Fed is accommodative, and there are no signs that it will be anything other than accommodative over the next year. There is also the possibility that the equity markets will become more reasonably valued if corporate profitability exceeds expectations. While corporate profitability significantly declined in 2020, it beat estimates by approximately 20%, which historically is a remarkable “beat”. If that trend continues, valuations will look a bit more reasonable.

WHAT NOW?

Simply put, stay with your plan. How quickly the economy normalizes depends on how quickly vaccines get distributed and used. It is also dependent on how quickly people return to their pre-pandemic routine after the vaccination is rolled out, and on what changes to behavior caused by the pandemic are permanent or temporary. These issues are unknowable, but all will have an impact on the US economy and financial markets.

We do not take big “bets” on how these issues are resolved in constructing client portfolios. We will make tactical shifts as we see various market opportunities, but these shifts are all done within the context of broad diversification. As we customize client portfolios, please feel free to contact your Relationship Manager or Portfolio Manager to discuss how your current portfolio is presently constructed.

Best Regards,

Howard Coleman | Chief Investment Officer and General Counsel

Insights Tags

Related Articles

April 13, 2026

Watch Coldstream’s MarketCast for Second Quarter 2026

April 9, 2026

Turbulence: Navigating a Complex First Quarter

January 29, 2026

Artificial Intelligence: Boom or Bubble?