Insights

July 23, 2021

Market Commentary: 3Q 2021

In Market Commentary

The US Economy: Will it be too hot, too cold, or just right?

At first glance, the information we consider in evaluating whether the economy will be “too hot, too cold, or just right” appears to be confusing. Depending on what data you focus on, a case can be made for any of these three outcomes:

- Inflation is currently running hot as commodity prices and wages have risen, but yields on treasuries have fallen recently, indicating the bond market anticipates inflation will cool.

- Valuations in the US equity market are high, indicating market participants are optimistic about future earnings and perhaps a “just right” scenario. But we have seen a surge in COVID cases from the Delta variant, which could put pressure on earnings of companies, especially those involved in restaurants, travel, and hospitality.

- Unemployment remains stubbornly high and those participating in the jobs market remains stubbornly low, but the US consumer appears to be in excellent shape as income and savings are well above historical averages and defaults and bankruptcies are at historical lows.

We wanted to share with you how we are making sense of this data and our view of the economy and markets going forward.

THE CRITICAL IMPORTANCE OF THE FED

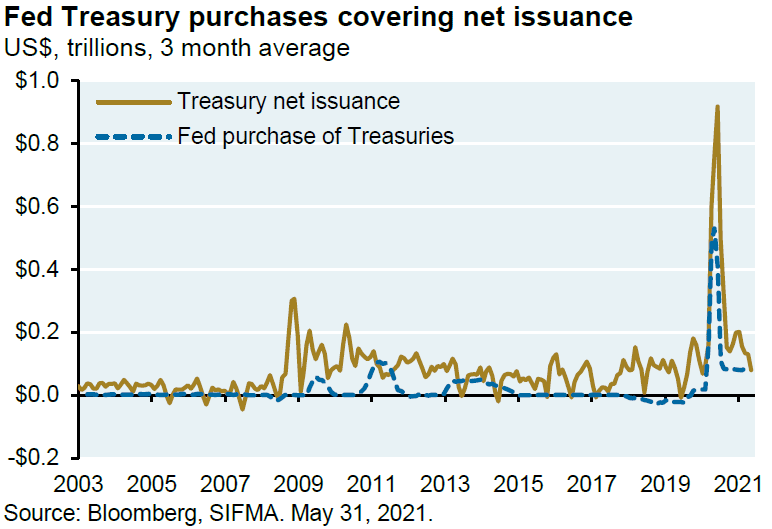

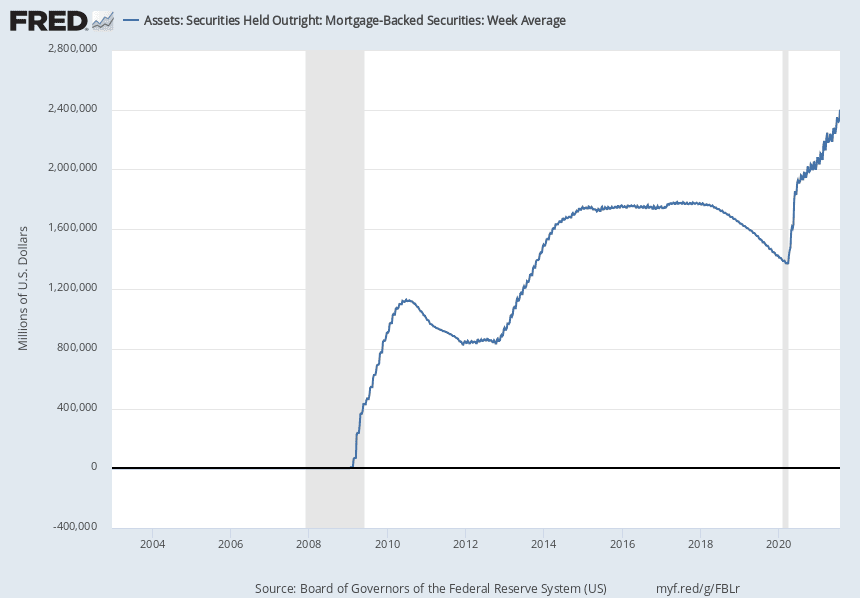

The Fed played a large part in the recovery from the COVID-related recession by spurring lending to support struggling companies and consumers. It did so by moving the Fed Funds rate to zero, buying Treasuries, buying mortgages, and signaling, for the first time in history, that it would buy the debt of private companies. While the Fed is no longer buying the debt of private companies, it continues to buy Treasuries and Mortgage Backed Securities (called Quantitative Easing or QE) at a record pace: currently buying almost all the net issuance of Treasuries and a record amount of Mortgage Backed Securities:

The effect of the Fed’s actions has been to enable corporations and consumers to borrow cheaply and fuel economic growth. Typically, the US economy does not go into recession, nor does the US equity market go into bear market territory, unless the Fed begins “tightening” monetary policy by taking away the “punch bowl” of low rates.

There are two reasons the Fed might take away the punch bowl: inflation or full employment.

INFLATION – PERMANENT OR TRANSIENT

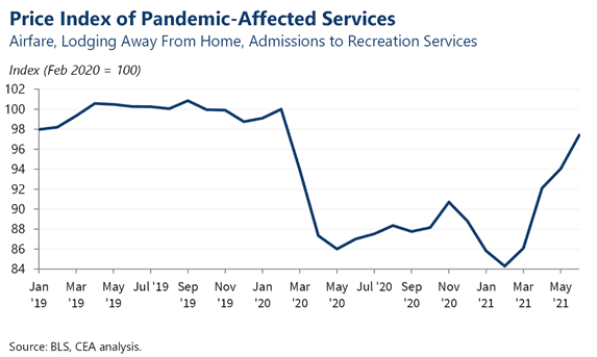

There can be no dispute that we have seen a year-over-year spike in inflation, with the Consumer Price Index rising 5.5% year-over-year in June. The Fed, however, considers this inflation transitory for several reasons. First is the “base effect” – measuring June 2021 inflation against June 2020 when the economy was predominately shut down. The base effect is apparent in services inflation. While year-over-year prices in services have significantly increased, prices have not yet returned to their pre-COVID levels.

Thus, there may be some additional year-over-year inflation due to the base effect, but that only would bring prices back to pre-COVID levels.

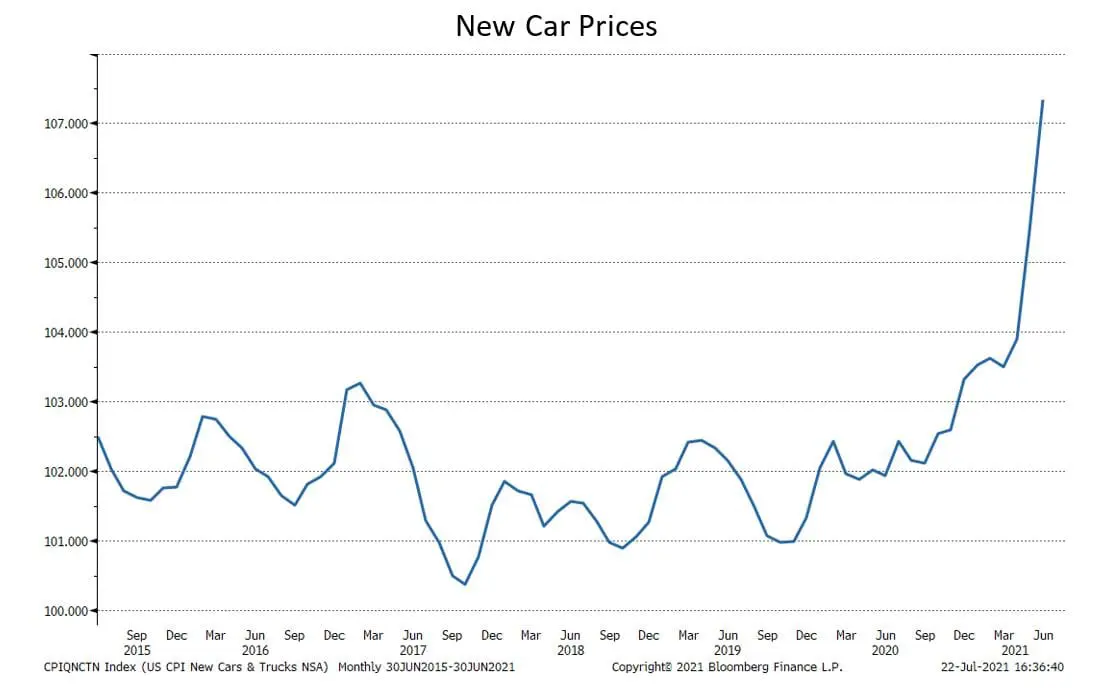

In addition to the base effect, the current increase in inflation is due to the supply/demand imbalance caused by the COVID-related economic shut down when supply was curtailed because demand was limited. Now with the economy recovering faster than expected, demand has dramatically increased, but supply has not caught up. The effect of this supply/demand imbalance is exemplified in new car prices. Car manufacturers cut new car production last year and are currently having difficulty ramping up production due to shortages of component parts. As a result, new car prices have skyrocketed as demand has outstripped supply:

Source: Bloomberg

Like the base effect, the supply/demand imbalance should be temporary, in the Fed’s view.

While we agree with the Fed’s outlook as our base case, we are watching wage inflation. If wage inflation continues to rise it could have ripple effects through the economy causing inflation to become sticky and forcing the Fed to curtail QE and begin to raise rates earlier than expected to reduce it (although even in this scenario, we would be surprised if the Fed begins tightening in 2021).

FULL EMPLOYMENT

The other factor that could cause the Fed to raise rates is if the economy reaches full employment. In this scenario, the Fed’s expectation is that the economy would be strong enough to withstand a rate increase without going into recession. While, in the great majority of cases, recessions do not happen unless the Fed is tightening, recessions do not always occur when the Fed tightens, and a strong economy could withstand a tightening without going into recession.

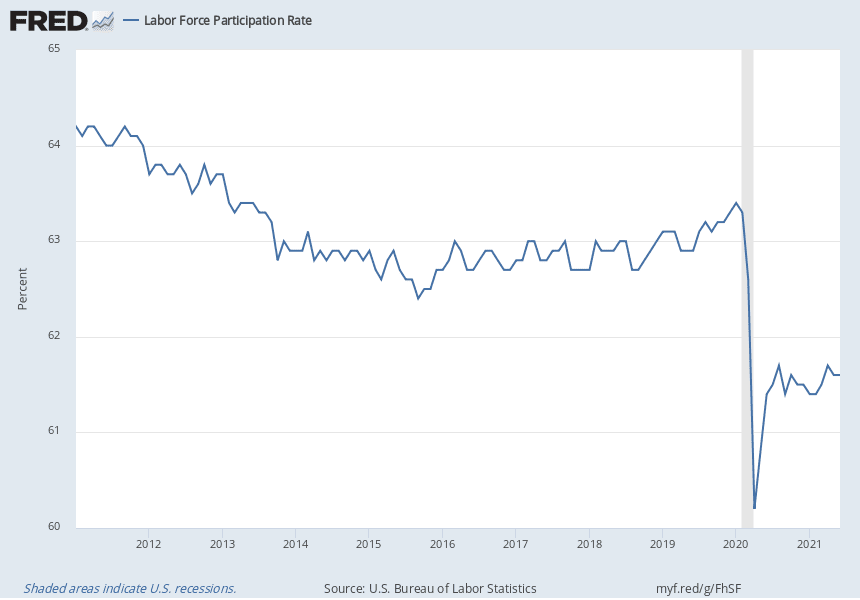

In addition, it does not appear that the economy will reach the Fed’s employment goals this year or early next year as the unemployment rate remains elevated and the labor participation rate remains low by historical standards.

Given the Fed’s view that current inflation is “transitory,” and that unemployment remains stubbornly elevated, our base case is that it is unlikely the Fed will begin tightening in the near term.

Of course, the global recession last year was not spurred by Fed tightening, but by the economic curtailment caused by COVID.

THE DELTA VARIANT

Recently, Treasuries rallied (yields on Treasuries fell) apparently over concern that the Delta variant would curtail economic growth. Indeed, the number of COVID cases in the US has significantly increased recently, although from a low base. While the Delta variant is significantly more contagious than the “original” COVID strain, vaccinations appear to be effective against the Delta variant and very effective in preventing serious illness or death in vaccinated people.

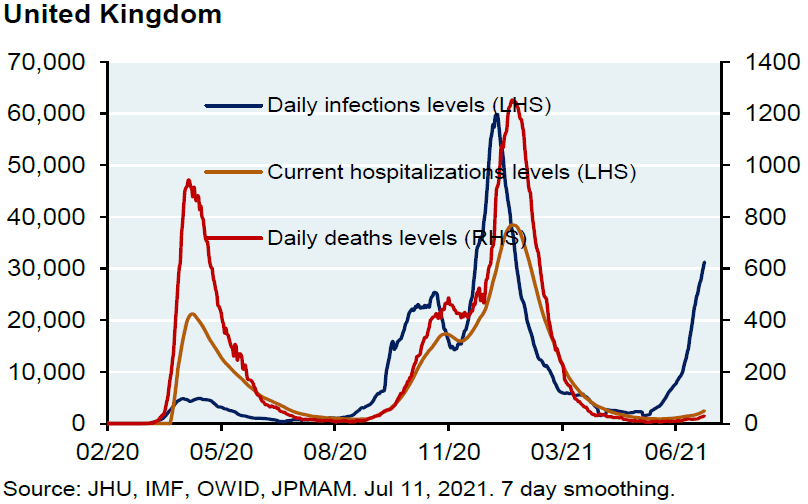

The United Kingdom is about five weeks ahead of the US in the spread of the Delta variant and has a similar vaccination rate to the US. So, its experience may well be instructive.

Source: JP Morgan

As this chart shows, while cases have significantly increased in the UK, severe illness has been contained. If this experience is mirrored the US, it will probably not cause a significant curtailment of economic activity.

THE US CONSUMER

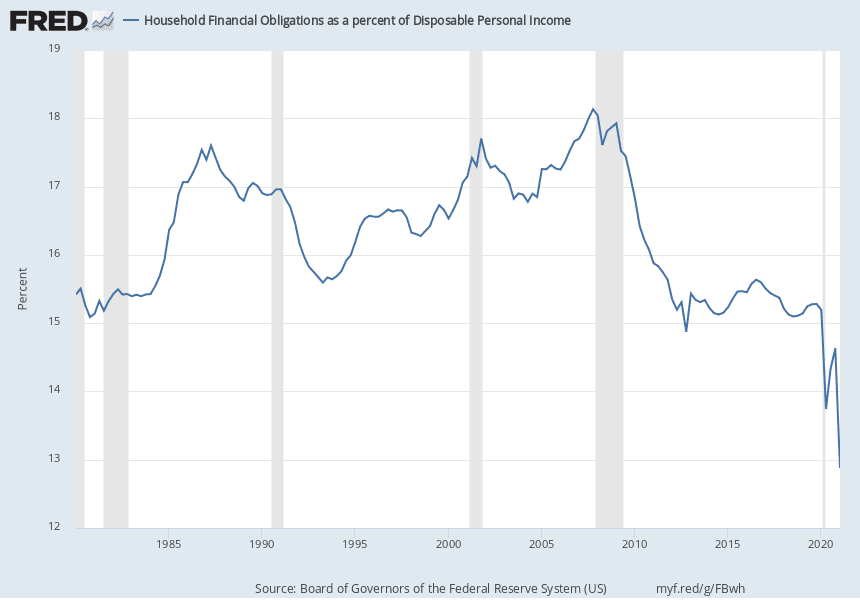

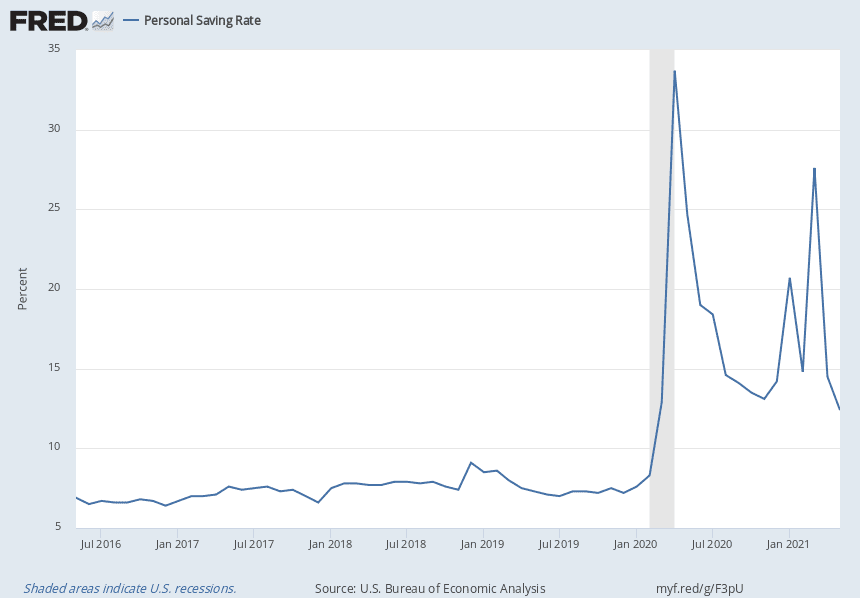

The behavior of the US consumer has a significant impact on economic growth, and the US consumer appears to be in a very good financial position – the ratio of financial obligations to disposable income is very low by historical standards, personal savings are high, and personal bankruptcies are at historical lows.

The strength of the US consumer bodes well for the continued economic recovery.

EQUITY MARKETS

Since their March lows, the US equity markets have continued to stage a strong rally, and valuations remain stretched. Accordingly, we would not be surprised to see the market pull back a bit at some point, as it does almost every year; however, the risk of a bear market currently remains muted with potential inflation or an unexpected spread of COVID as two of the major risks to that scenario. With recovery continuing, interest rates remaining low, and the US consumer in good financial shape, the prospects of the equity markets continuing to trend upward over the medium-term are good.

WHAT DOES THIS MEAN TO YOUR PORTFOLIO?

Stay diversified and stay the course. Even though our base case is relatively optimistic, no one has a crystal ball, and it is our view that trying to time the market is a fool’s errand. While we do make tactical shifts to take advantage of market opportunities or mispricing, it is not at the expense of diversification. We are acutely aware that we could be wrong in our outlook or that an event could occur (like COVID) that cannot be foreseen. Unlike going “all in” or going all cash, diversified portfolios allow you to participate in the upside when markets run and provide a cushion when markets fall.

As always, we greatly appreciate your confidence in us. If you have any questions or comments, please feel free to contact me, your Relationship Manager or your Portfolio Manager.

Sincerely,

Howard Coleman | Chief Investment Officer and General Counsel

Insights Tags

Related Articles

April 13, 2026

Watch Coldstream’s MarketCast for Second Quarter 2026

April 9, 2026

Turbulence: Navigating a Complex First Quarter

January 29, 2026

Artificial Intelligence: Boom or Bubble?