Insights

March 16, 2020

The End of the Bull Market

In Market Commentary

March 13, 2020

First, and most importantly, we hope you are doing well and staying safe.

The longest bull market in the history of US equities came to an end this week as the S&P 500 fell more than 20% from its peak in breathtaking speed. As of yesterday’s market close, the S&P 500 is down 26.3% from that peak and 22.9% YTD. Small- and mid-cap stocks once again underperformed the S&P 500, and international equities also swooned. Risky credit such as corporate high yield and emerging market debt also suffered significant losses, but not to the extent of equity market losses.

THE CAUSE OF THE SELL-OFF

The primary cause of the market sell-off is the uncertainty and fear surrounding the Coronavirus, and the impact that fear and uncertainty will have on the economy in general and corporate profitability specifically. This makes it unique from other bear markets, as the underlying source of the market’s downturn revolves around a lack of clarity surrounding health-related issues. And no one is currently able to quantify how the change in consumer behavior as a result of these health concerns will affect the economy and corporate profitability. The shock is one of both supply and demand. Supply because factories in China and now South Korea have shut down due to the virus, negatively impacting the supply chain. Demand because consumers are curtailing purchases and activities because of the virus. We have seen corporation after corporation suspend guidance regarding future profitability. This has caused extreme gyrations in equity market movements, with some significant up days mixed in with the downtrend due to the uncertainty, and with equity market volatility exceeding levels of the Great Financial Crisis.

The secondary cause of the downturn came last Friday when Russia refused to agree to OPEC’s proposed reductions in oil production due to a decrease in global demand. The generally accepted reason for Russia’s refusal is that Russia wanted to keep oil prices so low that the cost of crude oil production would exceed the price of crude oil for much of the US fracking industry, dramatically curtailing the future US role as an oil producer. Saudi Arabia responded by cutting its prices and increasing its production to prevent losing market share to Russia. The result was a steep decrease in oil prices with equity markets reacting negatively based on fears that this would be deflationary and would put many US oil producers out of business. On the bright side, however, low oil prices will be a “wind at the back” of the US consumer.

WHEN WILL THE DOWNTURN END?

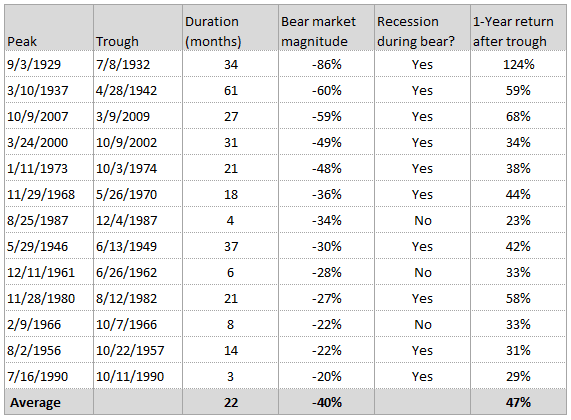

Here is a chart of past bear markets:

Source: ISI, Bloomberg, National Bureau of Economic Research, Haver Analytics, FMRCo (Asset Allocation Research Team) as of February 26, 2020

As you can see, the duration of the bear market and the magnitude of the losses vary greatly, but average 22 months and 40% respectively, but strongly recover a year after the trough. And as you can see, the market is anticipating that the US will go into a recession given that all but two previous bear markets were accompanied by a recession.

It is, however, important to note that the cause of this bear market is unique. We know the virus is a temporary phenomenon and will pass. Once it passes, consumer demand (the principal driver of US GDP) should return to normal. When this will occur is dictated as much if not more by public health policy than by economic policy.

As to economic policy, the Fed cut the Fed Funds rate by 50 basis points last week and is expected to cut rates further at its next meeting, if not before. It has also reinstituted Quantitative Easing (QE)1. Congress and the President also appear to be on the verge of implementing fiscal policy that would stimulate the economy. However, economic policy will not affect reactions to fear of the virus: It will not affect whether you will go out to dinner or not because of virus concerns. Economic policies can calm markets and mitigate the extent of the economic damage caused by the fear of the virus, but they are not as important as efforts to quantify the effect of the virus and minimize its impact.

1This QE was not designed to stimulate the economy, but to enable the smooth functioning of the Treasury market. Banks have been selling Treasuries to raise cash in order to allow their corporate customers to draw on their lines of credit causing some dislocation in the Treasury market. The Fed has now stepped in as a buyer.

As to minimizing impact, we have seen significant action taken to limit social gatherings of large numbers of people. This is a positive development. Historically, limiting social gatherings has had a significant impact on the spread of a virus. During the Spanish flu epidemic of 1918, St. Louis took extreme measures to limit public gatherings, while Philadelphia did not, even allowing a huge parade to go forward. Here is the result:

Source: The Daily Shot

As a nation we appear to be heeding this historical warning.

Unfortunately, as to quantifying the problem so we can manage its scope and limit its spread, our country is woefully behind in testing. Testing is critical so we can identify and isolate carriers of the virus. We have heard anecdotal stories of people who have wanted testing and have been turned down due to the lack of test kits. And the numbers bear out these stories:

Source: FT Research

On a positive note, there is bi-partisan Congressional outrage over this lack of testing, and it appears it will be relatively quickly addressed. However, the lack of early testing could lead to a longer period of resolution than the three month period of containment in Korea due to the aggressive testing that occurred there.

WHAT SHOULD AN INVESTOR DO NOW?

Simply put: stay the course. Maintain diversification.

We have heard some pundits argue that one should now buy equities aggressively and others advocate for selling equities aggressively. We would advise against either extreme course. We strongly believe that maintaining a diversified portfolio balances risk and reward far better than taking big bets on whether the stock market goes up or down next week. However, as you know, within the principal of diversification, we do not run static client portfolios. We do make tactical changes, but well within the overall concept of diversification.

Coming into the year, we had positioned client portfolios with a slight conservative tilt as we saw equity market valuations as frothy and the Conference Board’s Leading Economic Index declining. As the recent drawdown occurred, we have also tactically become slightly more conservative by selling some riskier debt positions and for those of you who use liquid alternatives, we increased our exposure to a manager whose strategy is designed to make money in a volatile environment and redeemed out of a manager who historically has done poorly in volatile environments.

We have seen some significant dislocations in certain markets as a result of this drawdown that should create some attractive buying opportunities. We expect we will leg into some of these opportunities over time.

Once again, these changes are marginal when compared to portfolios as a whole. Stay the course. While there may well be additional drawdowns in the equity markets, this should create opportunities in the future, and hopefully the virus will resolve itself in the near future.

Sincerely,

Howard Coleman

Chief Investment Officer and General Counsel

Insights Tags

Related Articles

April 13, 2026

Watch Coldstream’s MarketCast for Second Quarter 2026

April 9, 2026

Turbulence: Navigating a Complex First Quarter

January 29, 2026

Artificial Intelligence: Boom or Bubble?