Insights

July 29, 2020

A Stalling Recovery?

In Market Commentary

July 28, 2020

After the S&P 500’s downturn, culminating on March 23rd, it rallied 43.36% reaching its post-COVID high on June 5th. Since that time, the index has been essentially flat.

The stalling of the S&P 500 reflects the stalling of the US economy since June. Economic data in May and early June reflected a relatively quick pace of recovery. In the worst US hot spots of New York and New Jersey, the virus was becoming contained. Congress provided fiscal support and the Fed provided monetary support for the economy, which many predicted would keep the economy afloat until the virus was contained and the reopening process was well underway.

At that time, the dominant concern was that there could be a flare-up in the fall, as it was thought the virus may be seasonal like the flu, but at least until then the economy would be on a course of continual improvement. Unfortunately, with the recent COVID-19 flare-ups, particularly in the South and Southwest, the pace of re-opening this summer has stalled, which has resulted in a recent leveling off of economic activity as well as a decline in the US consumer’s confidence that the virus will be contained in the near future.

The Impact on the Consumer and the Economy

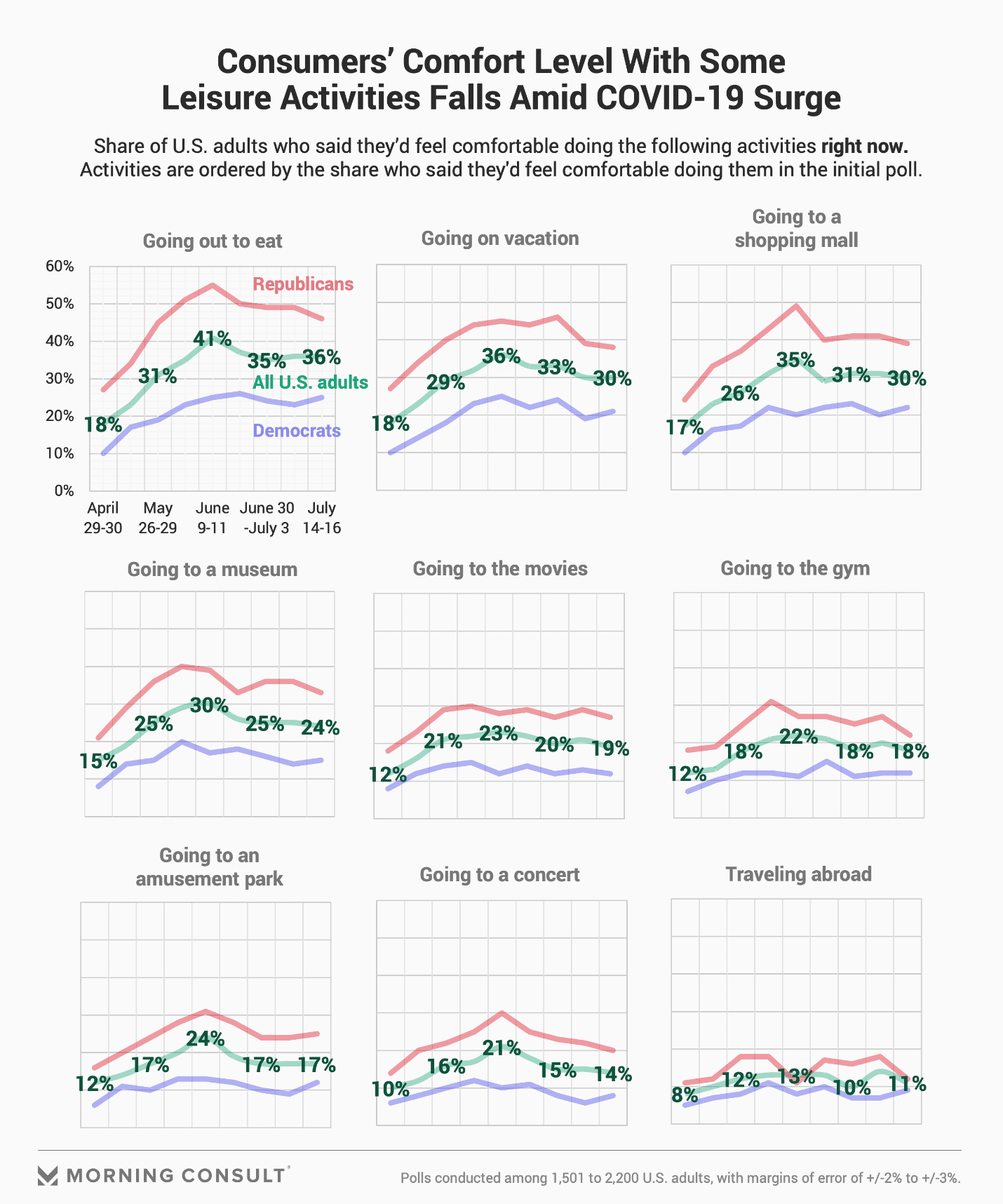

Since the recent outbreaks of the virus, the US consumer’s willingness to engage in leisure activities has declined from its June post-COVID highs.

Source: Morning Consult

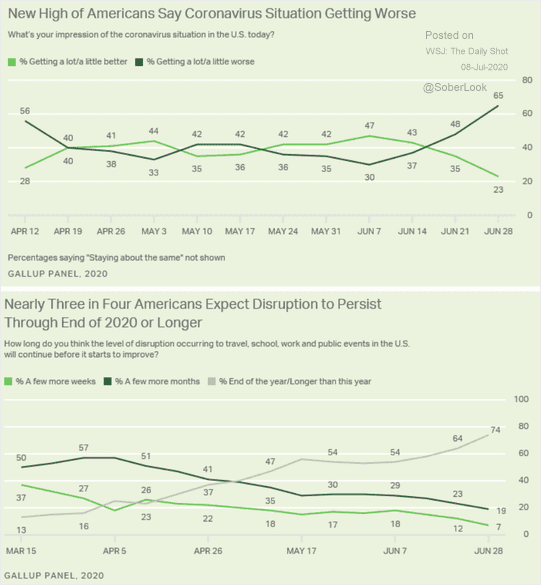

Similarly, the share of Americans believing the virus will get worse and last beyond 2020 has steadily and significantly increased since the middle of June.

Source: Daily Shot

The cyclical sectors of the US economy that were experiencing economic improvement are once again contracting or at best stagnating.

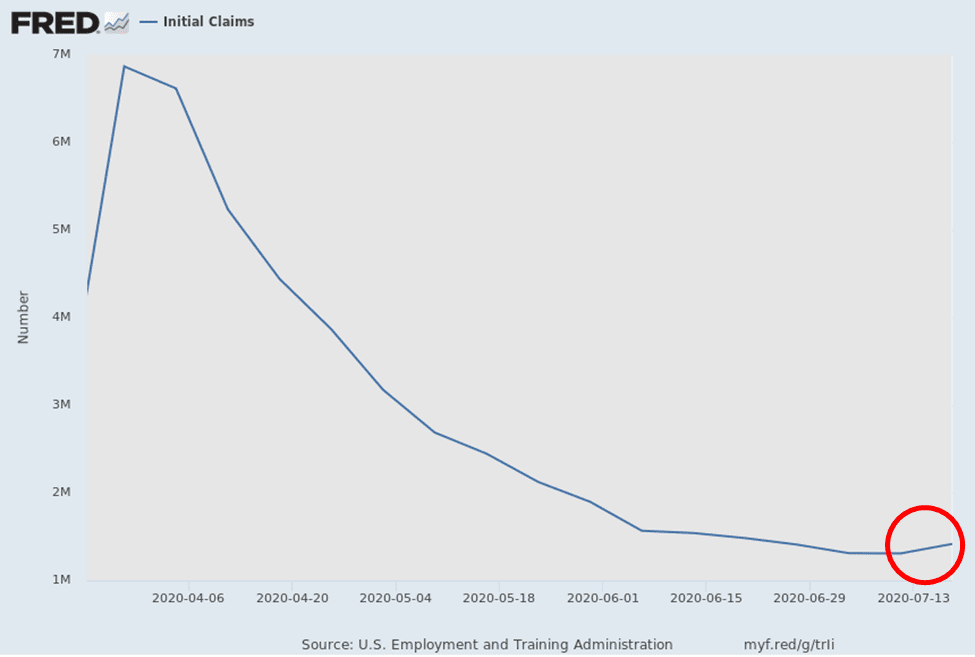

Most economic data published by the US government is monthly or quarterly and has not yet reflected the effects of the recent outbreaks. However, weekly data that does exist is reflecting the economic impact of these outbreaks. For example, initial claims for unemployment benefits are measured weekly. For the first time since March, weekly unemployment claims increased in the week of July 13th.

Source: FRED

While not a government entity, Oxford Economics, a highly respected economic consulting firm, created a weekly “Recovery Tracker”, which also shows a stall in the US economic recovery.

![]()

Source: Daily Shot

This stall has impacted the US equity markets.

The US Equity Markets

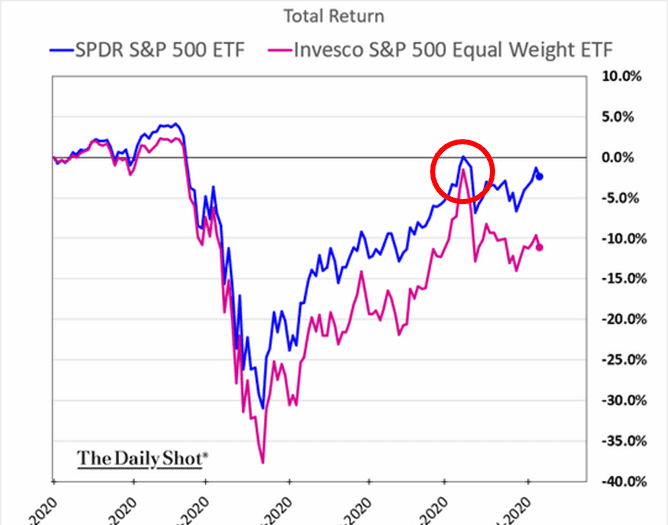

In our previous communications, we have discussed the significant outperformance of Apple, Microsoft, Amazon, Google, and Facebook over the S&P 500 as a whole, which now represent over 20% of that index. As the S&P 500 is a market-cap weighted index (i.e. the larger the total equity value of a company, the larger the percentage the company represents of the S&P 500), the more those five stocks increase in value compared to the rest of the index stocks, the bigger percentage of the index they become. It was not surprising to see those five stocks outperform most other stocks in the index, as the overall businesses of those five companies are not negatively impacted by the COVID related economic curtailment, while the great majority of the rest of the companies in the S&P 500 are significantly impacted.

However, in a recovery, the stock price of many of the companies whose businesses were negatively impacted by the curtailment of the economy could increase significantly. In May and early June, when investors thought the economy was recovering quickly, many of these stocks did outperform the five big tech stocks. This is reflected in a comparison of the S&P 500 with an equal-weighted S&P 500.

Source: Daily Shot

As you can see, there is currently a significant disparity between the equal-weighted S&P 500 and the S&P 500; however, during the period in May and early June, when investors thought the recovery would be quick, the two indices converged. As it became apparent that the pace of the economic recovery had slowed, the two indices diverged again significantly.

The equal-weighted S&P 500 better reflects the US economy as a whole than the S&P 500. And the performance of the stocks of the five large tech companies has cushioned the impact of the economic decline for large-cap US stock investors. However, these companies’ valuations have reached historic high levels while their profitability has not kept pace with the increase in their respective stock prices.

What Next for the Economy and the Markets?

We know that there is a direct relationship between our ability to contain the virus and an economic recovery. Beyond that, there is much uncertainty. Will there be additional outbreaks? Will what appears to be a much broader recent acceptance of wearing a mask and social distancing prevent further outbreaks? When will an effective vaccine or, at least, effective therapeutics be available? Does the virus have a seasonality component? These questions are unanswerable.

The uncertainty around COVID-19 translates into uncertainty in the financial markets. If the economic recovery continues to stall, can the valuations of the five large tech companies continue to increase? How much lower can US Treasury rates go? As many corporations are suspending guidance on future profitability, how can one know whether stocks are cheap or expensive?

While the economy has stalled, it does appear that Congress will significantly increase fiscal spending again and the Fed will continue to provide monetary support to the US economy. These actions should soften the economic impact of a slow recovery and may support equity prices.

Investing in This Environment

In structuring client portfolios, we are proponents of diversification as a means of dealing with uncertainty. A diversified portfolio of stocks, bonds, and, in some cases, alternatives is designed to protect your portfolio in the event of an equity sell-off and allow you to participate in the upside of an equity rally. We recognize that each of you has your own investment goals and risk tolerance, and we will customize your portfolio accordingly, but in the overwhelming majority of circumstances, our client portfolios will be diversified. Currently, within the context of diversification, we do see more risks to the downside in this environment and have positioned client portfolios with a slightly conservative bent. For details on how your particular portfolio is structured, please contact your relationship manager or your portfolio manager.

We hope you are healthy and doing well.

Best Regards,

Howard Coleman

Chief Investment Officer and General Counsel

Insights Tags

Related Articles

April 13, 2026

Watch Coldstream’s MarketCast for Second Quarter 2026

April 9, 2026

Turbulence: Navigating a Complex First Quarter

January 29, 2026

Artificial Intelligence: Boom or Bubble?