Insights

October 19, 2020

3Q 2020 Market Commentary

In Market Commentary

October 19, 2020

If, on December 31, 2019, we were told that the total return on the S&P 500 for the first three quarters of 2020 would be 5.57% (which is what it was), many would have concluded that 2020 would be a relatively normal/uneventful year in the equity markets with the slow but steady economic recovery that began in 2009 continuing. While, as we all know, this is not what occurred, it is an important reminder to avoid overreacting to short-term market volatility, even when that volatility is spurred by unprecedented events.

MARKET SUMMARY

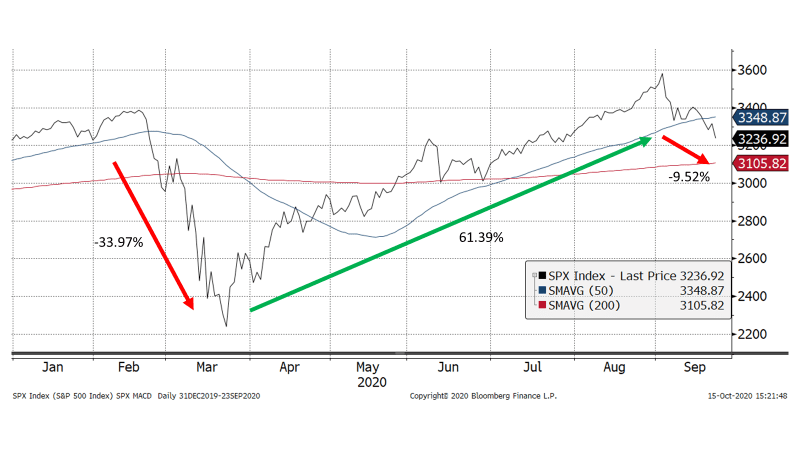

The S&P 500 has essentially undergone four phases this year. The first was a pre-COVID phase that occurred in January and the first part of February, in which US large cap equities reached new highs on the prospect of continuing low interest rates facilitating an on-going economic expansion. In the second phase, from late February until March 23rd, we witnessed the fasted decline into a bear market ever, spurred by fears of the spread of COVID-19 and the attendant economic shutdown. During this period, the market took only 20 days to reach bear market territory and declined 34.0%. This was followed by the third phase, quickest recovery from a bear market ever as the S&P 500 gained 61.4% in 126 days, reaching new highs on August 18th. The apparent rationale for the market’s recovery was that deaths from and cases of COVID-19 were declining, that parts of the economy were re-opening, and that the massive fiscal and monetary support enacted by Congress and the Fed would provide “bridge financing” to the US economy until the spread of the virus was curtailed or an effective vaccine developed. The fourth phase saw a decline in the S&P 500 of 9.5% occurring mostly in September when the progress in curtailing the virus and the reopening of the economy appeared to have stalled and Congress could not agree on additional fiscal stimulus.

Source: Bloomberg

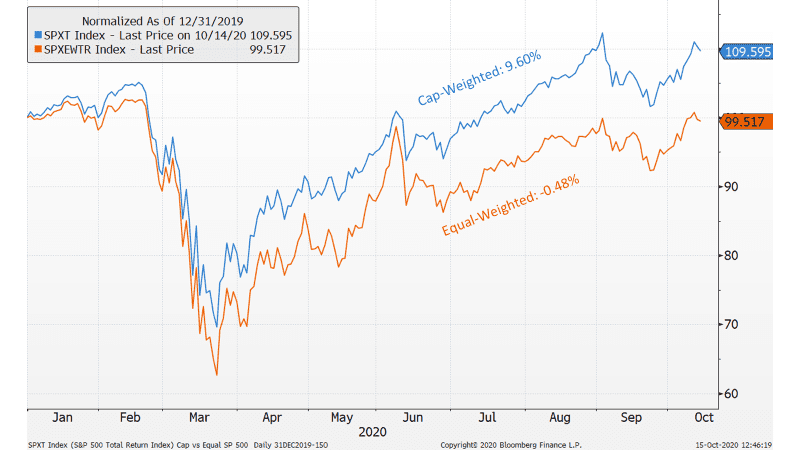

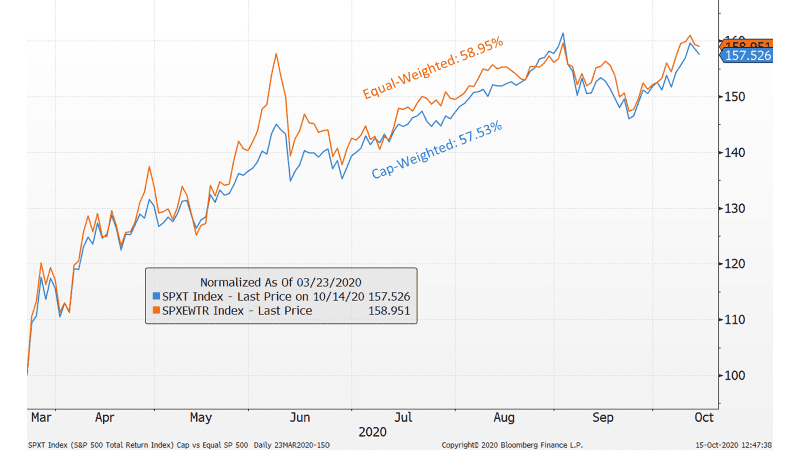

The stocks and sectors within the S&P 500, however, have not moved in lock step. Market participants have distinguished between stocks that benefit from people staying at home and stocks that benefit from an economic recovery. The “stay at home” trade has far outperformed the “recovery” trade over the course of the year, but not since the market lows of March 23rd when the whole market moved up in tandem. This is borne out by comparing the performance of the cap-weighted S&P 500 to the equal-weighted S&P 500. The cap-weighted version is the typical S&P 500 index in which five “stay at home” tech stocks (Apple, Microsoft, Google, Facebook, and Amazon) constitute over 20% of the Index, while the equal-weighted version simply counts each company equally.

Year to Date Return of S&P 500 to Equal Weighted S&P 500

Source: Bloomberg

Return of S&P 500 to Equal Weighted S&P 500 from March 23rd to Date

Source: Bloomberg

The flight to the “stay at home” trade caused valuations of the five large tech stocks to soar. Earnings per share for these companies have improved in 2020, but not nearly as much as the price of their common stock. While the S&P 500’s price to earnings ratio (P/E) at 21.6 is high compared its historical average of 16.5, the five large tech stocks’ P/E at the end of the third quarter was over 51, driven by Amazon with a P/E of 121. The influence of those stocks on that index is also demonstrated by the fact that only 41% of the stocks within the S&P 500 are up for the year, despite the index being up over 5.5%.

Small cap stocks may be a better representation of the US economy than the S&P 500, and investors have recognized that, on the whole, smaller companies have less resources to weather an economic shutdown than larger companies do. This has resulted in a wide disparity between the 2020 returns for the S&P 500 and small cap stocks as measured by the Russell 2000, which is down over 15% for the year. While we do believe that valuations, especially in the tech sector, are stretched by historical standards, the dispersion in returns among equity sectors and by company size does have an underlying rationale.

THE ECONOMIC REBOUND AND GOVERNMENTAL SUPPORT

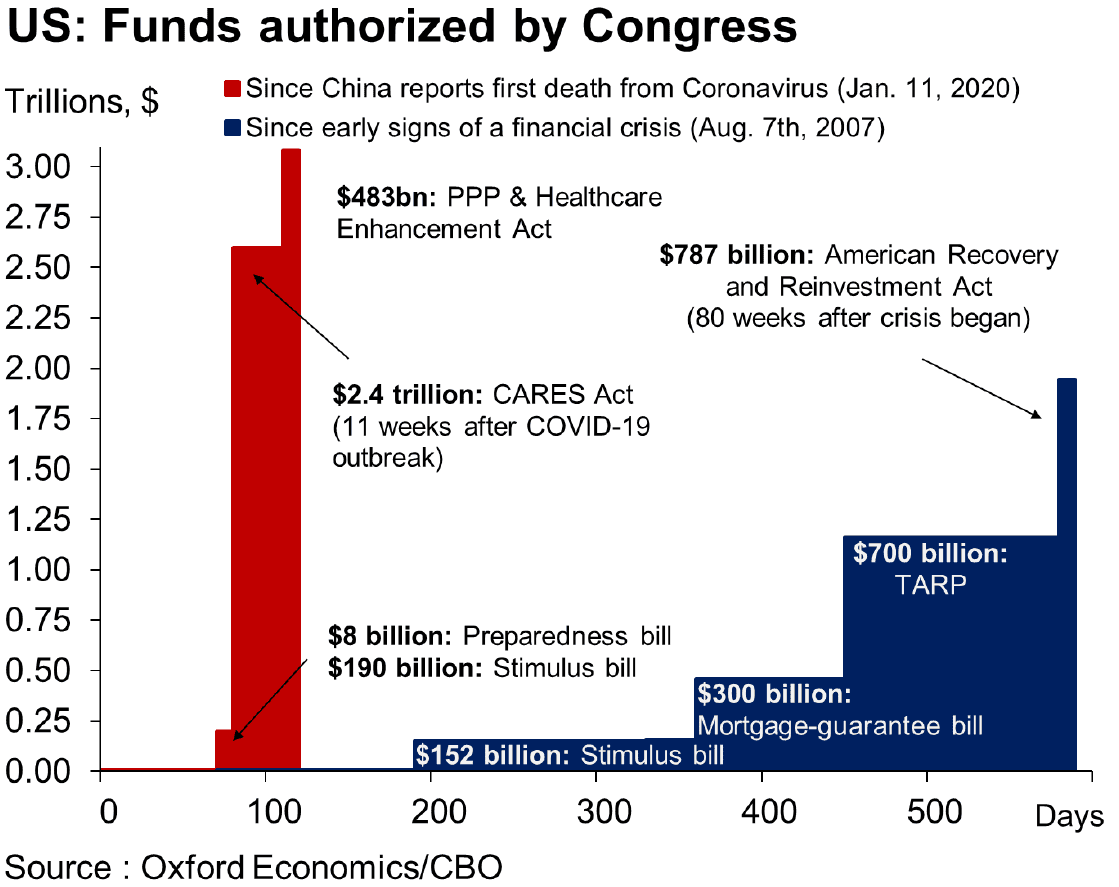

Congress and the Fed responded to the COVID-19 related economic shutdown with unprecedented governmental support in both the amount and speed in March and April. Among other measures, Congress provided direct payments to individuals and increased unemployment benefits, and the Fed intervened in the fixed income markets to stabilize those markets and keep interest rates low. The amount of support Congress and the Fed provided far exceeded the support they provided after the 2008 Financial Crisis.

The intervention prevented an economic collapse. Personal income actually increased as a result of Congress’ economic support. The unemployment rate, which reached 14.7% in April, has fallen below 8% for September. GDP fell over 30% in the second quarter but according to some estimates will gain as much as 35% in the third quarter. Fed intervention caused the corporate bond market to stabilize and enabled corporations to issue debt so they could survive a deterioration in earnings. Low interest rates also spurred record activity in the housing market in the third quarter.

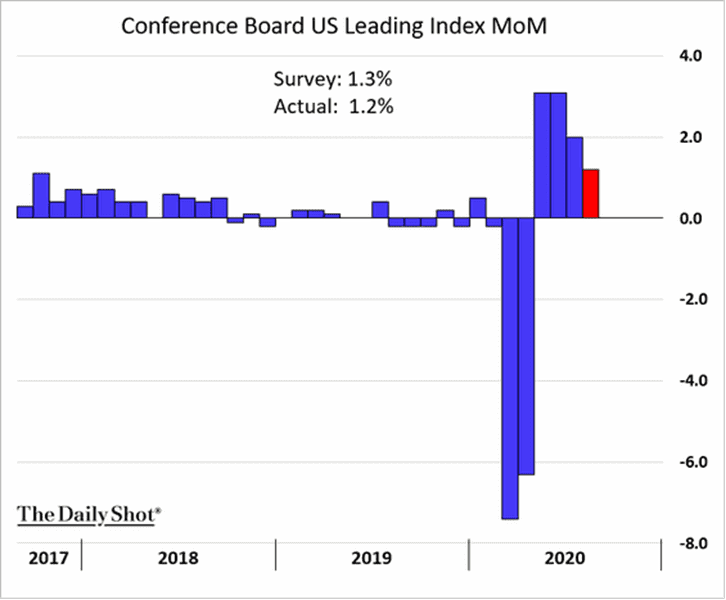

However, there are warning signs that the support is starting to wear off. The Conference Board’s Leading Economic Indicators, while positive again, are declining.

Source: The Conference Board, The Daily Shot

While the unemployment rate has fallen, permanent unemployment is increasing. And real personal income, including governmental payments, is declining again. These indicators are why Chairman Powell has strongly urged Congress to implement more fiscal support soon.

THOUGHTS GOING FORWARD

In the near-term, we anticipate that market movements will be governed by: (1) how quickly we can develop an effective vaccine, or at least make additional progress in containing the spread of COVID-19 and reopen the economy, (2) whether there will be additional fiscal support that will limit lay-offs and bankruptcies until the economy reopens, and (3) whether the presidential election is contested. In the medium-term, assuming the virus is contained, market movements will be impacted by the time it takes after reopening for the economy to return to its pre-COVID levels and whether the massive amount of debt the country has incurred to stabilize the economy will ultimately be inflationary. In the longer-term, assessing how much of the economic behavioral changes we have all experienced will remain permanent, and what impact those permanent changes will have on both market movements and the structure of the economy, will be critical (e.g., in real estate, will the trend of people moving from dense urban areas to less dense areas continue and will the traditional office setting return; in travel, will business travel return; in retail, will in-store shopping come back).

The VIX index, which measures equity market volatility, remains elevated, and we agree that investors should expect continuing volatility in the markets in the short-term. This does not mean you should change your investment game plan. As the first three months of this year have demonstrated, despite periods of extreme volatility, staying with your plan is, in the great majority of cases, the best course.

As always, we appreciate the opportunity to work with you and please let your Relationship Manager or your Portfolio Manager know if you have any questions or concerns.

Best Regards,

Howard Coleman

Chief Investment Officer and General Counsel

Insights Tags

Related Articles

April 13, 2026

Watch Coldstream’s MarketCast for Second Quarter 2026

April 9, 2026

Turbulence: Navigating a Complex First Quarter

January 29, 2026

Artificial Intelligence: Boom or Bubble?