Insights

January 19, 2024

Market Commentary: “What, Me Worry?” – Alfred E. Neuman

In Market Commentary

What a difference a year makes. In 2022, both the equity and fixed income markets suffered significant declines over market participants’ fears that Fed tightening would lead to a recession but not curb inflation. Contrast this to 2023 when the Fed indicated the tightening cycle was coming to an end, inflation was receding, growth remained strong, and the profitability of S&P companies, although flat for 2023, exceeded analysts’ expectations. As a result, both the equity and fixed income markets rallied in 2023 with the S&P 500 gaining 26.29%, the tech-heavy NASDAQ gaining a remarkable 44.64%, and due to a strong fourth quarter rally, fixed income produced profitable returns for the year as well.

The Anticipated Soft Landing

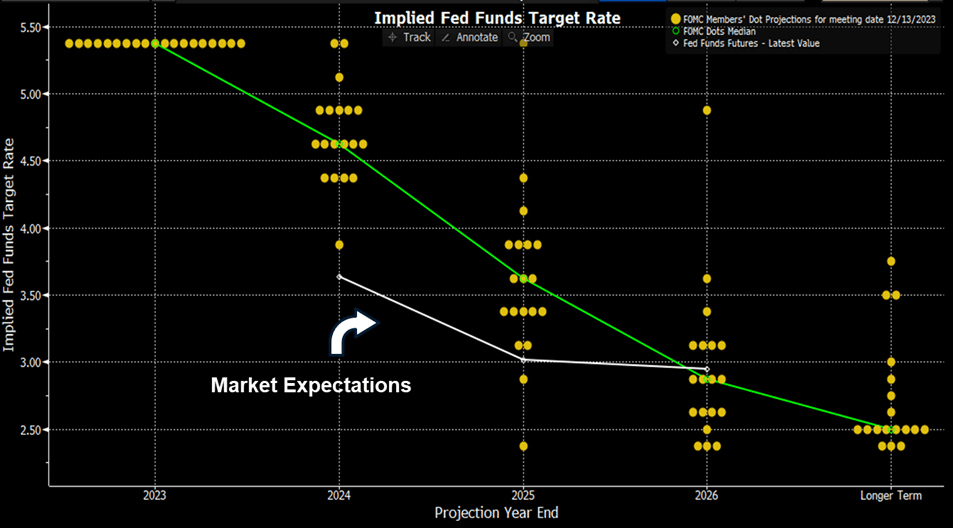

By the end of 2023, pricing in the large cap equity and fixed income markets appeared to incorporate a view that the Fed could aggressively cut interest rates because inflation would be tamed but economic growth would continue apace (a “Soft Landing”). This view is evidenced by the difference between market participants’ predictions of Fed rate cuts and the Feds own predictions. The chart below shows the median number of rate cuts predicted by the members of the Fed (yellow dots, with the green line being the median) compared to market participants prediction of future rate cuts (the white line).

RATE CUT COMPARISON – THE FED’S VIEW VS. THE MARKET’S VIEW

Source: Bloomberg

Aggressive rate cuts in this scenario means the Fed would have gone from trying to restrict growth to curtail inflation by creating higher borrowing costs to the Fed encouraging growth through lower borrowing costs, which would result in increased corporate profitability. As a result, equities became more expensive with the multiple an investor was willing to pay for a company’s earnings in the S&P 500 going from 16.65x on December 31, 2022, to 19.51x on December 31, 2023. In addition, both the investment grade and risky corporate credit markets were pricing in limited default risk.

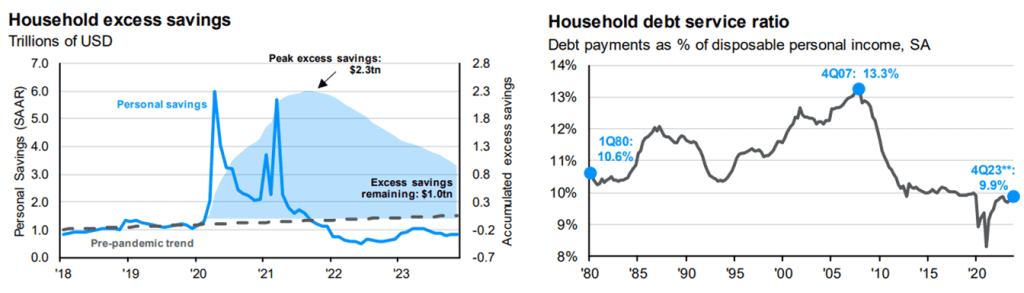

There is economic data to support this optimistic view that the Fed’s mission is being accomplished. US GDP was up 4.9% for the 3rd Quarter (data for the 4th Quarter is not available as of the time of this letter), and inflation as measured by CPI decreased to 3.2% in that quarter. In addition, the labor market remained strong but was loosening with labor costs receding, and US households had ample savings and plenty of income to pay off any indebtedness.

CONSUMER STRENGTH

Source: JPMorgan

Risks to the Optimistic View

There are two major risks to the anticipated soft landing. The first is that the Fed’s tightening over the last two years has a lagged effect and could push the economy into a recession. Higher interest rates take time to filter through the economy and may curtail growth that is not yet evident in the economic data. For example, with the Fed Funds rate still in restrictive territory, shelter costs, a large component of inflation, may be lower than the Consumer Price Index (CPI) indicates. The CPI shows rent costs are still elevated but more real time data shows it has already declined significantly.

Source: JPMorgan

And two historically reliable indicators, the Conference Board’s Leading Economic Indices and the inversion of yield curve are both pointing to a recession in the near future.

The second risk is the opposite of the first risk: that the Fed lowers rates too quickly and the US economy experiences a new bout of inflation. This occurrence happened twice before, most recently in the 1970s.

DOUBLE BOUT OF INFLATION

Source: The Federal Reserve

The Magnificent Seven

No discussion of 2023 can be complete without mention of the impact the 7 mega cap technology stocks had on the market as a whole. Those seven stocks accounted for approximately 60% of the gains for the S&P 500. Much of these gains were driven by optimism over the prospects of Artificial Intelligence. At first glance it appears that these stocks are overvalued. At the end of 2023, investors paid 26.9x for $1 of earnings for the ten largest companies by market cap in the S&P 500 when combined, well above any historical averages for the S&P 500. When those stocks are excluded from the index, investors paid 17.1x for $1 dollar of earnings, still higher than the median price paid historically, 16.59x, but much closer. However, the anticipated growth in earnings and the free cash flow from the Magnificent Seven is far greater than the market as a whole.

CHART OF 7 V. S&P FCF

Source: JPMorgan

If these predictions of growth come to fruition, these valuations are not unreasonable, and their stock price could continue to climb; however, if their growth slows, there is significant downside risk for their stock prices.

What This Means for You

At Coldstream, we are investing to meet your financial goals. Our core belief is that diversified portfolios are the best strategy for achieving this outcome. Diversified portfolios allow you to participate in the upside when markets rally but seek to mitigate losses when the market falls. Over the long run, few, if any, can time the market successfully. And although we may make small tactical shifts to take advantage of market dislocations, we will not abandon the fundamental concept of maintaining a diversified portfolio. The “Periodic Table of Returns” chart below demonstrates that market leaders and laggards come and go. Placing big bets on which asset class will be the next leader carries far too much risk, in our view, especially when our focus is to meet your long-term financial goals.

PERIODIC TABLE OF ASSET CLASS RETURNS

Source: JPMorgan

As always, we greatly appreciate your trust in us. If you have any questions or comments, please feel free to contact me, your Wealth Manager or your Portfolio Manager.

Related Articles

April 13, 2026

Watch Coldstream’s MarketCast for Second Quarter 2026

April 9, 2026

Turbulence: Navigating a Complex First Quarter

January 29, 2026

Artificial Intelligence: Boom or Bubble?