Insights

October 7, 2022

Understanding Your Benefits at Virginia Mason

In Company Benefits, Insurance, Wealth Strategy

Virginia Mason offers their employees a robust suite of retirement benefits. When utilized correctly, these benefits can be valuable assets to your financial plan. Throughout this article, we’ve highlighted the pros and cons of the most prominent benefits.

Virginia Mason Retirement Plans

403(b) Plan

With this plan you can defer anywhere from 1% to 80% of your salary each year. However, contribution limits are the same as that of a 401(k). The limits are as follows:

- 2022 Contribution Limit: $20,500 pre-tax, with a $6,500 “catch-up” for those at least age 50.

- 2023 Contribution Limit: $22,500 pre-tax, with a $7,500 “catch-up” for those at least age 50.

The advantages of deferring pre-tax salary into this plan include lowering your taxable income and experiencing tax-deferred growth. A lineup of target-date funds is offered, which also include the distinct advantage of utilizing a Fidelity BrokerageLink® connection. This connection allows participants or their financial advisor to strategically manage investments within the account.

401(a) Plan

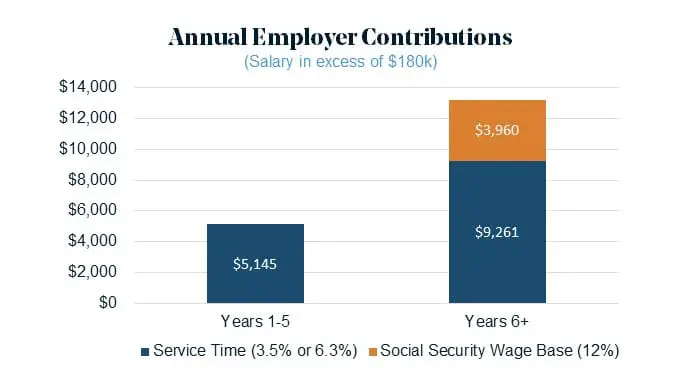

Contributions to this plan are only made by the employer (Virginia Mason), and not you as the employee. How much they contribute is based on two factors: service time and the Social Security Taxable Wage Base (which changes annually).

- Service Time: 3.5% for your first five years of service, increasing to 6.3% after five years.

- Social Security Wage Base: $147,000 in 2022, increases approximately $4,000 – $5,000 annually

After five years of service, employees receive 12% of eligible contribution for participant earnings over the Social Security Wage Base and up to $180,000.

Example A: Recent Employee Reese has two years of service and earns a salary of $200,000 in 2022. Virginia Mason contributes 3.5% of $147,000, which equals to $5,145.

Example B: Experienced Employee Erin has 10 years of service and earns a salary of $300,000 in 2022. Virginia Mason contributes 6.3% of $147,000, and 12% of $33,000 (5-Year Social Security Wage Base cap ($180,000) – standard Social Security Wage Base ($147,000), which equals $13,221.

If you’re thinking, “this plan seems less advantageous as the Social Security Wage Base increases each year,” you would be correct. As currently written, an increasing percentage of contributions are made each year at 6.3% and less at 12%, as long as the $180,000 cap stays stagnant. Either way, it’s a generous incentive to stay for a long career at Virginia Mason given the contribution increase after five years of service.

457(b) Plan

With this plan you can elect to contribute another $20,500 of your salary annually, and a $6,500 “catch-up” contribution if you are 50 years of age or older. There is no employer match, but interest and earnings are allowed to grow tax-free until the funds are withdrawn. What’s unique about a 457(b) compared to other retirement plans is that there’s no 10% penalty for withdrawing before age 59 ½ in certain circumstances. Examples are early retirement, resignation, or “unforeseeable emergencies.”

Example of how these plans work together

If you are under the age of 50, you can defer a total of $41,000 of salary in 2022 using the 403(b) and 457(b) Plans. Taking advantage of the 401(a) Plan offering, you can also receive a generous employer contribution of up to $13,221 if you have at least five years of service at Virginia Mason.

Out-of-Pocket Healthcare Costs

To assist with out-of-pocket healthcare costs, Virginia Mason offers employees the option of both a Flexible Spending Account (FSA) and Health Savings Account (HSA).

Flexible Savings Account

An FSA allows you to put pre-tax money away for certain out-of-pocket healthcare costs (e.g., copayments, deductibles, prescription medications, or other approved medical expenses). FSAs are limited to a $2,850 annual contribution limit.

You may also elect to utilize an FSA to pay for dependent care with tax-free dollars. Keep in mind there is a $570 carryover limit from year-to-year, so any contributions pre-tax to this account should be guaranteed to be spent. Childcare costs are commonly fixed for the year, but should your childcare situation change, you may want to consider decreasing your FSA contributions.

Health Savings Account

An HSA is a medical savings account that allows you to set aside pre-tax dollars to grow tax-free. Withdrawals from an HSA are also tax-free if used to pay for qualified medical expenses. Since most people will face substantial medical costs in their later years, an HSA is also a great option for supplementing your other tax-advantaged retirement accounts. It’s recommended you speak with your advisor to understand the investment capabilities within your HSA and formulate a plan for use of this extremely tax-advantageous account type.

For the 2023 calendar year, the annual contribution limit for an individual HSA has been increased from $3,650 to $3,850. Similarly, the limit for a family contribution has increased from $7,300 to $7,750. If an HSA owner is 55 years of age or older, they can also make an additional $1,000 “catch-up” contribution.

Reviewing Your Benefits

If you are a Virginia Mason employee and have questions about how to optimize your employer benefits, we are here to help. A Coldstream Wealth Manager can help determine which benefits are best suited for your specific tax and financial situation. Contact us today to learn more.

DISCLOSURES

Coldstream analyses are not intended to provide, and should not be construed to constitute, complete accounting, insurance, investment, legal, or tax advice. None of the information provided constitutes a recommendation or solicitation of any particular custodian or account. The investment strategies shown may not be suitable to you. Coldstream does not provide any specific tax or legal advice; you should consult your tax, legal, or other advisors before implementing any changes to your current financial situation.

To ensure compliance with requirements imposed by the IRS, we inform you that any federal tax advice contained in this communication (including attachments) is not intended or written to be used and cannot be used for (1) avoiding penalties imposed under the Internal Revenue Code or (2) promoting, marketing or recommending to another party any transaction or matter addressed herein unless the communication contains explicit language that it is a tax opinion in compliance with IRS requirements. Please contact your tax advisor for guidance on your individual situation.

Insights Tags

Related Articles

June 10, 2026

Setting Up Young Adults for Financial Success: An Ask the Expert Podcast

June 4, 2026

Becoming Financially Independent: A Practical Checklist for Young Adults

May 28, 2026