Insights

January 30, 2023

SECURE 2.0 Act – Good or Bad?

In Tax Planning, Wealth Strategy

As we were wrapping the last of the holiday presents, Congress had their hands full finalizing the SECURE Act 2.0, which included 100+ different changes to retirement accounts. Most of these changes impact either a very narrow group of people, or the related dollar amount is so small that it leaves us wondering if there are real impacts to our financial security. Let’s focus on a few key changes in the SECURE Act 2.0 that are meaningful to our favorite fictional character, Kate Washington, and evaluate whether the impact on her family is good or bad for their financial success.

More About Kate

Kate Washington reflects many of the qualities of the clients we serve. She’s busy, successful, smart, and has a lot of her plate. Kate and her husband, Victor, are in their late forties, and have three children ages 10-18. Kate founded a quickly growing small business, and her husband, Victor, is an executive at Microsoft. They are high-income earners on track to build substantial wealth over the next decade and appreciate the benefits of thoughtful advice as they navigate financial decisions and balance their time between their family and their careers.

Key Impacts for Kate

RMD starting age is pushed back yet again… Good, if there is proactive Roth conversion planning

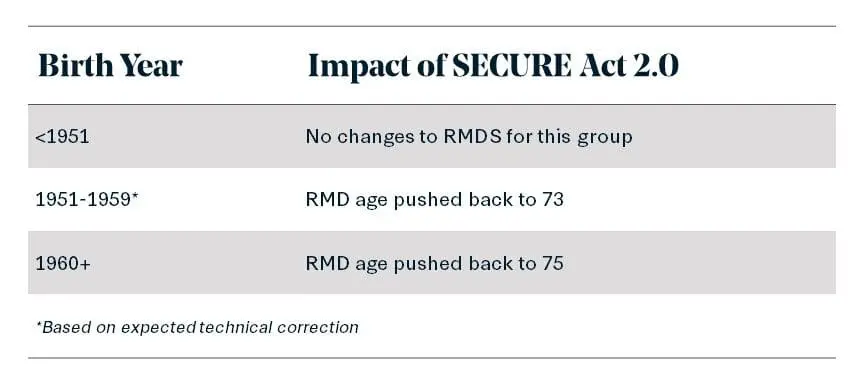

Currently, distributions from IRAs are required starting at age 72. However, the Secure Act 2.0 changes the start date to age 73 for those turning 73 in the next 10 years, and to age 75 for those thereafter. Since Kate was born after 1960, this means the start date for Kate’s Requirement Minimum Distributions (RMD) will now be the year she turns 75. At first glance, this seems like a good thing as it allows Kate to delay starting distributions and accumulate an even larger pre-tax IRA balance. However, this also means when Kate does start her RMDs, she’ll have to distribute more over a shorter period – thus, forcing her to pay income tax on these distributions in what may end up ultimately being a higher tax bracket. Without proper planning, this change in the Secure Act could be a negative for Kate and result in her (or her heirs, who will have to distribute an Inherited IRA over a ten-year period) paying much higher tax rates on her IRA distributions. The solution is for Kate to proactively do Roth conversions after she and Victor retire. They intend to retire at age 55, and because the plan is to delay Social Security until age 70, Kate and Victor would likely be in a lower tax bracket from age 55 to 70, making it an optimal time for Roth IRA conversions.

The Takeaway: Overall, this change is good for Kate and her family. However, it’s easy to see how this change might lead some families to pay more income tax if they’re not engaged in proactive Roth conversions.

Ability to convert 529’s to Roth IRA’s… Good, but effective only with thoughtful planning

Kate and Victor had always been convinced that their oldest son, Max, would follow his dream and attend NYU film school, so they contributed more to his 529 plan to prepare for this expense. However, much to their surprise, he fell in love with their alma matter, the University of Washington, and their out-of-pocket costs were much lower than expected. SECURE 2.0 includes a provision that would allow Kate to convert any leftover funds in a 529 to a Roth IRA for Max. At first glance, this change seems like a win! However, it comes with many nuanced restrictions: Max must have earned income to receive a Roth IRA contribution from his 529 plan, the annual contribution limit is $6,500, and the lifetime contribution limit per beneficiary is $35,000. However, if Kate is savvy in updating the beneficiary of a leftover 529 plan balance, it looks like the law is written that she could change the beneficiary and max out the $35,000 limit for each of her three children, and potentially other eligible beneficiaries.

The Takeaway: This change in the Secure Act now gives Kate more options as far as what to do with leftover 529 funds and offers the potential to kickstart her children’s Roth retirement savings at a young age.

Catch up contributions in retirement plans… Not great, but better than nothing

Kate is not thrilled about her upcoming 50th birthday but the SECURE Act 2.0 includes a small positive for those in the Over 50 club: catch-up contributions will now be indexed for inflation! Before you get too excited, there are strings attached. SECURE Act 2.0 also introduces a new income limitation for those who elect to make catch up contributions: if you earn over $145,000, you will be required to make Roth catch-up contributions; you cannot elect pre-tax catch-up contributions. Kate is self-employed and has a self-employed 401(k) plan, so the new rules are applied differently to her than her husband Victor, who works at Microsoft. Because Victor’s income exceeds $145,000 per year, his catch-up contributions are required to be made in a Roth. For Kate’s self-employed 401(k), as currently written, it appears that sole proprietors’ catch-up contributions will not be subject to this income limitation; therefore, Kate can still make pre-tax catch-up contributions. Kate and Victor had been pursuing a strategy of deferring as much pre-tax income as they could since they are currently in the highest tax bracket. They know that when they retire early, they will drop into a lower tax bracket and that will be an optimal time to pursue Roth conversions. So, while the ability to contribute more to their retirement plans once they turn 50 is a good thing, the requirement to make catch-up contributions in a Roth is not ideal.

The Takeaway: It’s better than not being able to make catch-up contributions at all. We’d still prefer the ability to put funds in a pre-tax Traditional IRA as opposed to accumulating savings in a post-tax Roth IRA account.

One more benefit that Kate can look forward to as she reaches another milestone birthday: If Kate continues to work into her 60’s, the SECURE Act 2.0 offers a four-year window when she can make even larger catch-up contributions. For those ages 60-63, you can make a catch-up contribution equal to the greater of $10,000 or 150% of the catch-up contribution limit.

SECURE Act 2.0… Overall good or bad?

- We are grateful (and somewhat surprised) that SECURE Act 2.0 did not make any changes to the ability to do back-door Roth contributions or Roth conversions.

- It’s shocking that SECURE Act 2.0 fails to provide any clarity on whether RMDs are required for those subject to the new 10 year rule rolled out in the original SECURE Act.

- On the positive side, SECURE Act 2.0 does include additional assistance for first responders, military members, disaster area victims, victims of domestic abuse, and disabled individuals.

While it’s a step in the right direction, the changes aren’t significant enough to meaningfully impact most of our clients. The number of changes and the strings attached will require individuals to exercise careful tax planning and enlist help to determine when the myriad of rules included in this bill could potentially benefit them. We continue to advocate thoughtful and proactive wealth strategy as a key part of your overall financial management. Our Wealth Management teams are here to provide guidance and navigate this new territory together. Please reach out with questions.

Information contained herein is subject to legislative changes and is not intended to be legal or tax advice. Consult a qualified tax advisor regarding specific circumstances. This material is furnished “as is” without warranty of any kind. Its accuracy and completeness are not guaranteed and all warranties expressed or implied are hereby excluded. To ensure compliance with requirements imposed by the IRS, we inform you that any federal tax advice contained in this communication (including attachments) is not intended or written to be used and cannot be used for (1) avoiding penalties imposed under the Internal Revenue Code or (2) promoting, marketing or recommending to another party any transaction or matter addressed herein unless the communication contains explicit language that it is a tax opinion in compliance with IRS requirements.

Related Articles

May 15, 2026

Irrational Decisions in Investing

April 29, 2026

Financial Habits Everyone Should Cultivate

April 14, 2026

Finding Tax Efficiency in an Era of Increasing Tax Obligations