Insights

January 13, 2026

Perspective After a Volatile Year: What 2025 Reinforced About Diversification and Discipline

In Market Commentary

2025 Highlights

Global growth has proven resilient, despite trade shocks.

“Liberation Day” on April 2nd, 2025, when President Trump’s package of tariffs went into effect, sent shockwaves through markets. Since then, however, the outlook for markets has rebounded and even improved for 2026. Still, inflation and a weaker U.S. dollar remain the lingering scars of tariff escalation — adding to rising fiscal concerns worldwide.

Equities delivered strong gains across regions and styles.

U.S., international, and emerging market equities all produced double-digit returns for the year. While markets still favored growth and AI-related themes, sector participation broadened as the year progressed.

Diversification finally worked again.

After years of narrow U.S. leadership in equity markets, 2025 marked a meaningful shift as international equities — in both developed and emerging markets — substantially outperformed U.S. stocks. Global diversification was rewarded as a weaker U.S. dollar, improving overseas earnings trends, and supportive fiscal policy abroad drove international outperformance.

Fixed income returned to its traditional role.

Bonds delivered positive real returns, with high-quality fixed income providing both income and diversification. After several difficult years, fixed income once again contributed meaningfully to portfolio outcomes.

Policy uncertainty remained elevated, but markets proved resilient.

Trade tensions, fiscal debates, and geopolitical events led to volatility throughout the year, yet markets consistently looked through short-term disruptions toward a backdrop of optimism around long-term growth.

Valuations moved higher, tightening the margin for error.

Strong returns compressed future expected returns and reinforced the importance of discipline as we enter 2026.

Volatility, Patience, and Perspective

In last year’s market commentary, Shifting Tides, we highlighted the growing case for diversification after an extended period of narrow U.S. market leadership. That framework proved timely. In 2025, those shifting tides did more than change leadership — they lifted nearly all boats, as U.S. equities, international markets, emerging markets, and fixed income all delivered positive returns. While the growth drivers differed by asset class, the common theme was resilience in the face of policy uncertainty and elevated macro noise.

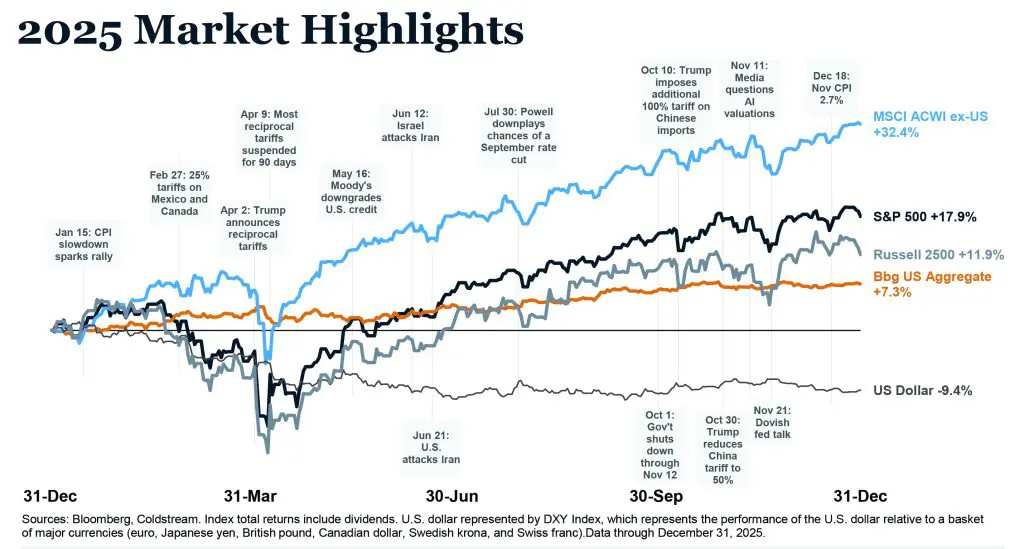

Importantly, the path to these outcomes has been far from smooth. Throughout the year, investors navigated sharp drawdowns, policy-driven volatility, and an almost constant stream of unsettling headlines, from trade escalation and government shutdowns to geopolitical tensions and shifting expectations around inflation and interest rates. At several points in 2025, reacting to the news flow alone would have made reducing risk feel not only rational, but prudent. The chart below highlights the return path for U.S. Large Cap (S&P 500), U.S. Small/Mid Cap (Russell 2500), International Equity (MSCI ACWI ex-US), U.S. Bonds (Bbg US Aggregate) and the U.S. Dollar throughout 2025 along with notating some noteworthy highlights.

Yet it was patience, not prediction, that ultimately captured the year’s broadly positive returns. Markets consistently proved more resilient than sentiment, rewarding investors who remained disciplined through periods of uncertainty. As we enter 2026, the lesson is not that volatility has disappeared, but that staying invested through it remains one of the most powerful contributors to long-term outcomes. Balanced portfolios, grounded in diversification and risk management, continue to offer a foundational framework for navigating markets where the headlines rarely tell the full story.

Economy: Resilient Growth but Not Without Friction

The global economy closed 2025 in better shape than many feared at the start of the year. U.S. consumers remained resilient, supported by wage growth and strong employment, while corporate investment, particularly in AI-related capital expenditures, continued to expand. Europe benefited from a meaningful pivot toward fiscal stimulus, while China stabilized with targeted policy support despite ongoing structural challenges.

Inflation continued to trend lower but remained sticky in key services categories, allowing central banks to begin easing cautiously rather than aggressively. The Federal Reserve cut rates gradually, framing the cycle as insurance against downside risk rather than a response to economic weakness.

Fiscal policy became a more prominent growth driver. In the U.S., the One Big Beautiful Bill provided a modest tailwind into 2026, while Europe’s shift away from austerity supported regional growth prospects. At the same time, rising government debt and persistent policy friction underscore longer-term structural challenges.

Overall, the economic backdrop entering 2026 is constructive but not without vulnerabilities — a combination that argues for participation without complacency.

U.S. Equities: Broad Participation Within Strong Returns

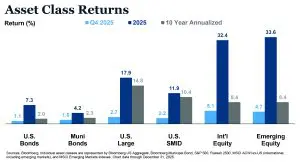

Looking at the chart above, U.S. equities delivered another strong year, with the S&P 500 advancing roughly in the mid-teens in 2025. Returns were supported by solid corporate earnings, continued adoption of productivity-enhancing technologies, and a resilient economic backdrop that sidestepped recession fears. Rather than a narrow handful of mega cap names single-handedly driving performance, dispersion across sectors and market capitalizations contributed meaningfully to overall market gains.

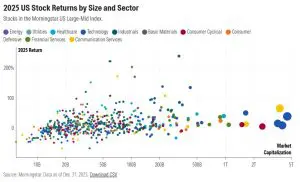

Morningstar created an illustrative chart (shared below) that highlights U.S. stock returns in 2025 by company size and sector. The horizontal axis shows company size while total 2025 returns are displayed on the vertical axis. The color shading distinguishes which sector each stock resides in. While a few of the “Magnificent Seven” — the stocks illustrated by the larger circles (based on company size) on the far-right hand side of the chart — generated strong returns, many were also essentially flat for the year. What is more notable is just how colorful the chart is, which highlights the dispersion within and across sectors as well as market capitalization. In many cases, mid- and smaller-capitalization companies posted returns comparable to, or exceeding, their large cap peers, underscoring that 2025’s gains were supported by broader participation across the market, rather than by a single style, size cohort, or narrow group of companies. This reflected a broader thaw in risk appetite and an environment where earnings revisions and economic sensitivity began to matter more to performance than pure sentiment alone.

Sector performance was similarly varied. Technology and communication services, often associated with innovation themes, performed well, but so too did industrials, consumer discretionary, and financials at different points in the year, reflecting a rotating leadership that broadened beyond the narrowest corners of the market. Additionally, the Russell 2000 Small Cap Index finished the year with a respectable return, underscoring that gains were not confined exclusively to the largest names.

As we look into 2026, this dispersed performance profile suggests a market that has not fully committed to one dominant style or capitalization bucket, and reinforces the value of diversified exposure across both size and style. While valuations remain elevated in some pockets, the diversity of performance drivers reflects an environment in which earnings delivery, sector rotation, and fundamental quality are likely to play an increasingly central role in differentiating returns.

International Equity: The Return of Global Leadership

International equities were among the strongest performers in 2025, with both developed international and emerging markets substantially outperforming U.S. stocks. While a weaker U.S. dollar amplified returns for U.S.-based investors, the leadership shift was supported by a broader set of fundamentals, including improving earnings trends, more attractive starting valuations, and increasingly supportive fiscal and monetary policy across several regions.

The chart below places 2025’s international outperformance in historical context, highlighting that shifts in market leadership have typically persisted across multi-year cycles. While 2025 performance may raise questions about whether the opportunity has already passed, history suggests that periods of leadership transition often unfold over time, not all at once.

Europe benefited from a meaningful pivot toward fiscal stimulus after years of restraint, while corporate earnings expectations improved alongside moderating inflation. Emerging markets were supported by stabilizing growth conditions, selective policy easing, and renewed interest in regions that had spent much of the past decade priced at significant discounts to U.S. assets. In both cases, returns reflected a normalization of relative value rather than speculative excess.

From a portfolio perspective, 2025 served as a reminder that global diversification often delivers its greatest value after long periods of disappointment. Leadership shifts rarely occur smoothly or predictably, but when they do, they tend to arrive quickly. Maintaining disciplined international exposure helped portfolios participate in this rotation without the need for reactive repositioning.

As we enter 2026, we view international equities as an important complement to U.S. exposure rather than a replacement. Relative valuations remain supportive, policy conditions are less restrictive than in prior years, and earnings differentiation is improving. While regional leadership will continue to ebb and flow, the case for maintaining diversified global equity exposure remains intact.

Fixed Income: Income Restored, Discipline Required

Fixed income delivered positive returns across most sectors in 2025, with the Bloomberg U.S. Aggregate Bond Index up over 7% for the year. Falling yields and attractive starting income levels allowed bonds to reclaim their role as both an income source and a stabilizer within portfolios. For additional information, refer to the Asset Class Returns chart above.

Credit markets remain supported by healthy corporate balance sheets, though spreads are tight by historical standards. As a result, income, rather than price appreciation, is likely to be the primary driver of returns going forward.

We continue to favor high-quality fixed income and municipal bonds, where yields remain attractive relative to risk. While opportunities exist across credit markets, selectivity and diversification are increasingly important late in the cycle.

Conclusion: Finishing the Race Matters More Than Winning It

If 2024 was about Shifting Tides, then 2025 was about recognizing that those tides lifted nearly all boats. Diversification worked, patience was rewarded, and both equity and fixed income investors benefited from a resilient economic environment and supportive policy backdrop.

As we enter 2026, stronger starting valuations, tighter risk premiums, and evolving policy dynamics suggest a need for a more measured approach. We believe staying invested, without overreaching for incremental returns, remains the most effective strategy.

Portfolio construction in this environment emphasizes balance, quality, and diversification across regions, asset classes, and sources of return. The objective is not to lead every lap, but to remain competitive through changing conditions and finish the race intact.

That discipline has served long-term investors well through many market cycles, and we believe it will continue to do so in the year ahead.

* Information is current as of 12/31/2025, drawn from third-party sources believed to be reliable but not guaranteed as to accuracy, timeliness or completeness. None of the information provided constitutes an opinion or a recommendation or a solicitation of an offer to buy or sell any particular security. Coldstream analyses are not intended to provide, and should not be construed to constitute, complete accounting, insurance, investment, legal, or tax advice. The investment strategies and securities shown may not be suitable to you. Past performance is no guarantee of future returns. Questions and comments may be directed to your advisor.

* The CFA Institute owns the certification marks CFA® and Chartered Financial Analyst®. CAIA® is a registered certification mark owned and administered by the Chartered Alternative Investment Analyst Association® in the United States.

Related Articles

January 12, 2026

Watch Coldstream’s MarketCast for First Quarter 2026

December 5, 2025

10 Trends to Watch For in 2026: Welcome to the Future

October 16, 2025

Watch Coldstream’s MarketCast for Fourth Quarter 2025