Insights

January 22, 2025

Shifting Tides

In Market Commentary

Stocks wrapped up 2024 on a high note, with a robust fourth quarter marked by the broader market reaching record highs. Contributing factors included strong economic growth, expanding corporate earnings, and a Federal Reserve decision to reduce interest rates. Also, investor enthusiasm remained fueled by the ongoing momentum in the artificial intelligence sector.

November’s U.S. election results provided an additional boost, propelling stocks to significant gains. However, the rally was short-lived, with December bringing a shift in sentiment. The Federal Reserve tempered expectations for further rate cuts, citing slower progress on inflation and an uncertain policy outlook. Meanwhile, bonds faced challenges throughout the quarter, with yields steadily rising in October and again following the election.

U.S. equities march higher

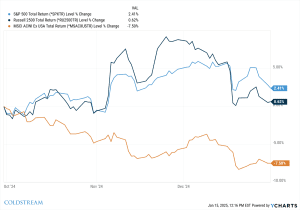

U.S. equities advanced over a volatile quarter with the S&P 500 Index gaining 2.4% while small and mid cap stocks were up a modest 0.6% (using the Russell 2500 Index as a benchmark). The S&P 500 touched a new record high 57 times in 2024, with the last peak reached in November on investor hopes that Trump’s presidential victory would usher in pro-growth policies such as deregulation and tax cuts.

This is typical behavior for equities during bull markets, and new all-time highs don’t necessarily signal an imminent pullback. However, with U.S. equities now at historically high valuations, earnings will need to increase commensurately to sustain momentum. We saw momentum recede somewhat at the close of the year as stocks fell sharply in December after the Fed signaled a slower pace of interest rate cuts.

4Q24 U.S. Large, U.S. Smid, and International Equity Returns

The outlook for 2025 earnings is relatively optimistic. A constructive U.S. economic environment, combined with potential policy tailwinds such as deregulation and lower corporate and individual taxes, could support further growth. Nevertheless, rising bond yields pose a key risk to the bull market. A persistent increase in rate expectations could cap equity gains and create volatility.

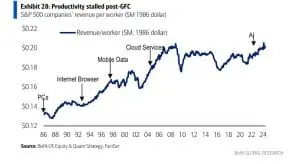

Additionally, the outperformance of the “Magnificent 7” stocks introduces another layer of vulnerability. While their long-term secular growth trends remain intact, their elevated valuations, in conjunction with higher bond yields, highlight the need for investors to consider opportunities among stocks with more attractive valuations. The high valuations on these mega cap companies continue to lean on the premise that they will deliver technologies that improve productivity and drive even further growth across the economy. The exhibit below illustrates the degree to which productivity has been stalled since the Great Financial Crisis.

Small cap stocks showing some signs of life

The robust macroeconomic backdrop indicates that strong earnings growth is likely across a broader range of economically sensitive companies, sectors, and market cap sizes. These areas, which are less stretched in valuation compared to the Magnificent 7, may offer compelling opportunities for investors. Small cap stocks enjoyed a strong rally after the U.S. election, driven by a vigorous economy and deregulation. However, their potential for continued outperformance may be limited by the Federal Reserve’s modest approach to rate cuts, which drove the underperformance that closed out the year.

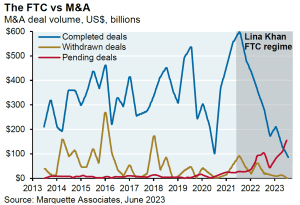

One trend that could benefit small cap stocks, as well as private equity, is a resurgence in merger & acquisition (M&A) activity, which has seen a dramatic decline during Lina Khan’s tenure as Commissioner of the U.S. Federal Trade Commission.

Embracing global opportunities amid diverging markets

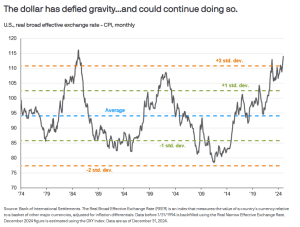

While U.S. equities have certainly experienced a tailwind from both a fundamental and currency standpoint, historically elevated valuations should encourage investors to consider global diversification. It’s true that international stocks saw the largest declines following the election outcome. Some of this was clearly driven by repositioning around the concern of potential tariffs and trade war escalation; however, the strength of the U.S. dollar — which gained 7.6% during the quarter — was the primary culprit for the dramatic underperformance of international stocks during the quarter.

International stocks are widely varied; each region and country requires its own unique analysis. Japan offers a compelling case with valuations that — while not cheap — are less stretched than those in the U.S. Japan has also seen improvements in broad corporate reforms and a governmental focus on overcoming deflation. The United Kingdom, despite grappling with deep structural challenges, is trading at relatively low valuations. Extreme investor pessimism in the region could create opportunities for upside surprises. In contrast, India’s market is near record valuation levels, rivaling those of the U.S., but its strong economic growth and reduced vulnerability to potential U.S. import tariffs position it for continued outperformance.

On the other hand, regions such as Europe, Mexico, and China face significant exposure to U.S. trade tariff policies. Despite their attractive valuations, these risks may overshadow any valuation advantages, leading to a less favorable outlook.

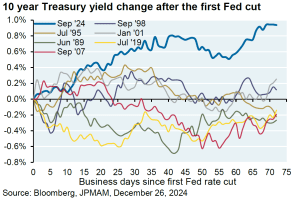

Wait, weren’t bonds supposed to do well once the Fed cut rates?

Since the Federal Reserve began its rate-cutting cycle in September, ten-year U.S. Treasury yields have risen, closing the fourth quarter at 4.6% — nearly 80 basis points higher than at the start of the quarter. This trend defies historical patterns, where yields typically decline during cutting cycles and periods of slowing economic activity.

Several factors seem to be driving this anomaly:

- Pre-emptive Fed easing has tempered expectations for further rate cuts.

- Proposed policies, such as tariffs and immigration restrictions, have heightened inflation concerns.

- Uncertainty around government policies has added to market volatility.

- Fiscal sustainability issues are putting upward pressure on bond yields.

Rising yields translated into losses for bond investors. The Barclays Aggregate Index declined 3.1% during the quarter but remained up 1.3% for the year. Long-term bonds were hit hardest, with the Bloomberg Gov’t/Credit Long Index falling 7.4%, while short-term bonds proved more resilient, ending essentially flat for the quarter, with the Bloomberg 1-3 Year Gov’t/Credit Index down 0.1%. Looking ahead, analysts predict continued volatility in the bond market for 2025, though they do not expect another dramatic surge in yields. Central bankers have made clear that with price pressures remaining sticky, they are in no hurry to cut interest rates too quickly or deeply and investors should likely prepare for an environment in which rates remain significantly higher than their pre-pandemic lows.

Conclusion

As we turn the chapter into a new calendar year, the investment landscape presents both challenges and opportunities. The strength of the U.S. dollar, shifting global equity weights, a potential resurgence in M&A activity, evolving stock-bond correlations, and the uncertain path of interest rates underscore the need for vigilance and adaptability in portfolio management. Staying informed and maintaining a balanced approach will be key to navigating the complexities of the year ahead.

With two remarkable years of stock market performance now behind us, we encourage investors to temper return expectations in the coming quarters and perhaps years. While this market rally won’t necessarily lead to a market correction, the leaders of the rally will now have to deliver on the elevated expectations that have been priced into them.

As always, we are truly honored in the trust you have placed in Coldstream to help guide you through these constantly shifting tides. Please don’t hesitate to reach out if you have any questions.

*All of Coldstream’s staff shall attain the required licenses and designations necessary for his/her position. The CFA Institute owns the certification marks CFA® and Chartered Financial Analyst®. CAIA® is a registered certification mark owned and administered by the Chartered Alternative Investment Analyst Association® in the United States.

Related Articles

April 13, 2026

Watch Coldstream’s MarketCast for Second Quarter 2026

April 9, 2026

Turbulence: Navigating a Complex First Quarter

January 29, 2026

Artificial Intelligence: Boom or Bubble?