Insights

February 25, 2022

Our View of the Impact of the Russian Invasion on Markets

In Market Commentary

Update as of 03/10/2022

Like many of you, we greatly admire the determination and perseverance of the Ukrainian people and are appalled by the indiscriminate brutality of the Russian invasion. While it is impossible to predict how this conflict will end, we do expect significant market volatility in the near term largely driven by daily headlines. Our investment focus, however, is on economic and market fundamentals, not daily headlines.

US and Russian Trade: Fundamentally, the direct exposure of the US economy to the Russian and Ukrainian economies is relatively minimal. In 2020, $11 Billion of Russian goods were traded with the US. Comparatively, Canada and Mexico are our top trading partners at $712 Billion and $540 Billion worth of goods respectively. Thus, reducing or even eliminating trade with Russia should have little direct impact on US economic growth.

Natural Gas and Oil: Despite this limited exposure, natural gas and oil prices have risen significantly as the war exasperated an already fragile supply-demand imbalance. While high gas prices are concerning and hurt economically vulnerable consumers the most, US consumers currently on average only spend about 4% of their income on energy. This data is about half of what consumers spent on energy in the 1970s when oil prices significantly affected US economic growth. Thus, the direct impact on the US economy on rising energy prices is far less than it was during the oil crisis of the ‘70s.

Corporate Profits and Economic Growth: Corporate profitability remained strong in the fourth quarter of last year and earnings estimates still indicate good growth, although not nearly as strong as last year’s. In addition, The Conference Board’s US Leading Economic Indicators remain positive. It is possible, however, that the first quarter of this year will show slow or negative growth in the US economy.

Europe: Unlike the US, Europe does have significantly more exposure to the Russian economy than the US does. Trade with Russia constitutes about 30% of Europe’s total trade. As a result, the possibility of a near-term recession in Europe stemming from the war and sanctions is greater than the possibility in the US.

We are actively monitoring risks as this war continues. While we may make some relatively small tactical shifts in portfolios based on our fundamental data analysis, any changes we make will not be at the expense of diversification.

Original post from 02/25/2022

Although this piece will focus on market and economic analysis, first and foremost, our thoughts today are with the people of Ukraine who are currently the subject of an unprovoked attack.

The State of Markets Coming into the Crisis

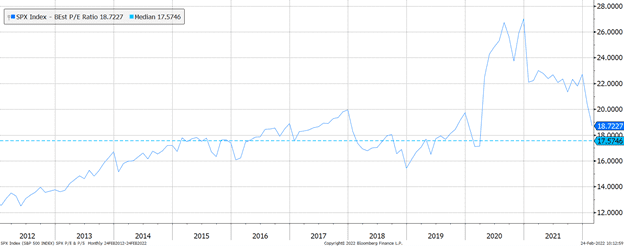

Since the start of 2022, U.S. equity markets have declined. This is primarily due to concerns about rising inflation and Federal Reserve policy changing from expansionary, which is designed to help fuel growth, to contractionary, which is designed to slow growth to dampen inflation. The S&P 500 Index declined 11.3% this year, and the technology-heavy NASDAQ 100 Index declined further at 16.6%. Coming into the year, valuations, which is the price an investor pays for a dollar of earnings, were elevated compared to the 10-year median. Valuations have now fallen to more reasonable levels due to the recent sell-off.

Forward Price to Earnings Ratio for the S&P 500

Source: Bloomberg

Bonds have also declined, with the yield on the U.S. 10-year Treasury rising from 1.51% at the end of last year to over 2% earlier this month. Prior to the build-up to the invasion, bonds did not provide the protection they usually do from a downturn in the equity markets, primarily due to the inflationary concerns in the U.S.

However, fundamentally, the U.S. economy remains strong. During the fourth quarter of 2021, corporate earnings grew over 31% from the previous year, and revenues grew over 14%. Additionally, U.S. GDP growth was strong, with 14% growth in the fourth quarter on an annualized basis. U.S. households remain in a strong economic condition as well.

Debt to Disposable Income

Source: Federal Reserve Board of St. Louis

U.S. LEI

Source: The Conference Board

Currently, the Conference Board’s U.S. Leading Economic Indicators do not imply that a recession is approaching. Additionally, sustained bear markets rarely occur absent a recession. However, sustained inflation and the Federal Reserve’s tightening monetary policy could negatively impact U.S. economic growth.

What Does the Russian Invasion Mean to This Scenario?

U.S. trade with Russia and Ukraine is not significant enough to have a material impact on the U.S. economy. For example, Russia is the 26th largest trading partner with the U.S., lower than Belgium or Malaysia. Ukraine has an even more negligible trading impact on the U.S. In addition, the U.S. is not energy-dependent on Russia. Therefore, cutting off trade with Russia would have a limited impact on U.S. corporate profitability.

However, this does not hold true for Europe as 36.5% of all Russian imports and 37.9% of Russian exports are with the European Union. This is a vital economic relationship for both parties. The fact that this relationship could be impaired is one reason the Russian stock market tumbled over 33% on the day of the invasion. In addition, Germany, the United Kingdom, and other European countries are dependent on Russian for energy sources. Before the Russian invasion, oil prices were already climbing in Europe as demand outweighed supply. European oil prices rose even further after the invasion, with oil prices rising to 103.00 dollars per barrel, which is high compared to historical standards. This explains why the recently announced sanctions against Russia did not include cutting off Europe from Russia’s energy supplies.

What Does this Mean for Portfolios?

While no one can predict how this crisis will ultimately unfold, drawdowns from geopolitical events are typically short-lived and often provide opportunities for investors to take advantage of market dislocations.

Geopolitical Event and the Market Response

Source: Capital Group

This invasion should not materially affect U.S. corporate profitability, as less than 1% of S&P 500 revenues are exposed to Russia and Ukraine.

For the great majority of our clients, maintaining diversification is critical as it allows you to participate in the upside when equity markets rally but dampens the downside in an equity market sell-off. For example, Treasuries rallied as the invasion became imminent, providing the down-side protection that diversification typically provides. For these reasons, Coldstream recommends maintaining your current diversified market exposure, including maintaining an allocation to developed and emerging markets despite the economic challenges that Europe may face, as many corporations in those markets should benefit from a rise in commodity prices.

If you have any questions or comments, please feel free to contact your wealth management team. We thank you for your support.

Header Image: Black smoke rises from a military airport in Chuguyev near Kharkiv, Ukraine, on February 24. Aris Messinis/AFP via Getty Images

Related Articles

April 13, 2026

Watch Coldstream’s MarketCast for Second Quarter 2026

April 9, 2026

Turbulence: Navigating a Complex First Quarter

January 29, 2026

Artificial Intelligence: Boom or Bubble?