Insights

July 25, 2024

Market Commentary: A Rally with Shifting Leadership

In Market Commentary

Unlike gains in the S&P 500 in 2023, gains in the first quarter of 2024 were broad based and driven by companies other than the large mega-cap tech companies. Indeed, the equities of two of the Magnificent Seven suffered significant declines in the first quarter of 2024 with Tesla falling 29% and Apple falling 12%. The S&P 500 was up over 10% and outperformed the tech-heavy NASDAQ index for the quarter.

However, in the second quarter, US mega-cap tech stocks were primarily responsible for the S&P’s 4.28% gain, with NVIDIA alone accounting for about 1/3 of the Index’s returns. For comparison, the “old economy” focused Dow Jones Industrial Average (DJIA) fell 1.27% in the first quarter, while the NASDAQ gained 8.47% for the quarter

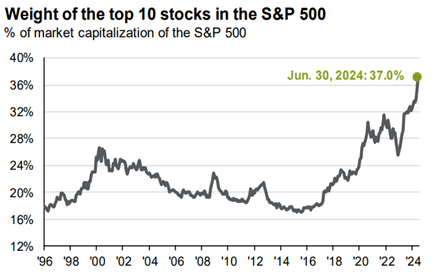

The concentration of these mega-cap tech companies in the S&P 500 is at levels that have not been reached in recent history.

Source: JPMorgan

The Recent Turnaround in US Small Cap Stocks

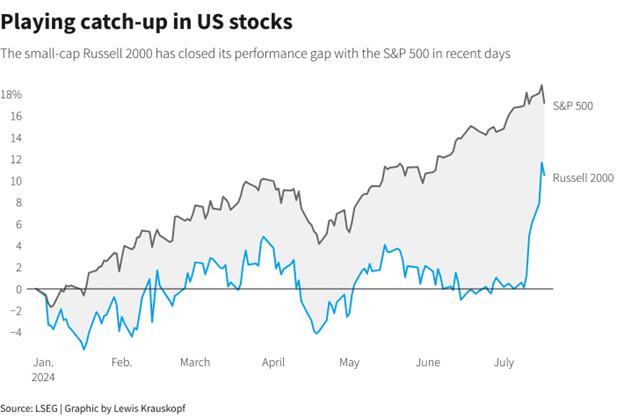

US small cap stocks, as measured by the Russell 2000 index, performed worse than even the DJIA in the second quarter falling 3.28% and continuing its four- year streak of underperformance to the S&P 500. From 2020 through the first quarter of this year, the Russell 2000 gained 20%, while the S&P 500 gained 60%, the largest underperformance between these two indices in 20 years.

High interest rates are a significant headwind for many of the companies in the Russell 2000, as approximately 40% of them are unprofitable and as a whole utilize more leverage than US large cap companies. As a result, movement in the price of the Russell 2000 has become correlated with interest rate movements, and as those rates rose, small cap stocks underperformed.

This trend reversed dramatically in July. Between July 10th and July 17th, the Russell 2000 gained 11.1%.

This remarkable 5 trading day performance was driven primarily by economic data in early July indicating a slowing economy and a slowing rate of inflation, resulting in market participants predicting lower interest rates going forward. It is yet to be seen whether this short term outperformance will last.

Can the rally be sustained?

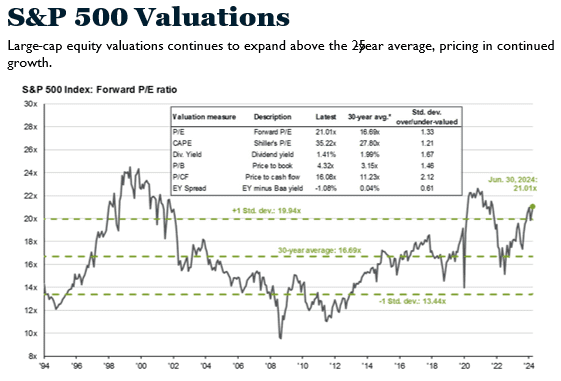

The S&P 500 is now richly valued by historical standards.

Source: JPMorgan

As can be seen from the chart, upward momentum can sustain an equity rally for a period of time, but valuations tend to return to their mean eventually. However, the equity market can rally without valuations increasing if companies exceed their earnings expectations. Currently, analysts are predicting an 11% increase in corporate earnings for the third quarter, and corporations generally appear to be in a strong financial position. Last quarter 74% of S&P 500 companies beat their earnings expectations, and if that rate continues, the market rally could continue. At these valuation levels, however, the stock price of companies often suffers significant losses if the companies miss their earnings target.

The Impact of Inflation and the US Consumer on Corporate Profitability

For many companies, general economic conditions can have a significant impact on their earnings. While US households remain in a good financial position generally, they continue to spend down their pandemic-related excess savings, and lower income households are showing signs of economic stress, as credit card and sub-prime auto loan delinquencies are beginning to rise.

![]()

Source: JPMorgan

If US households decrease their spending or if we suffer another bout of inflation, consumer reliant companies will have difficulty meeting their earnings targets.

What is an Investor to Do

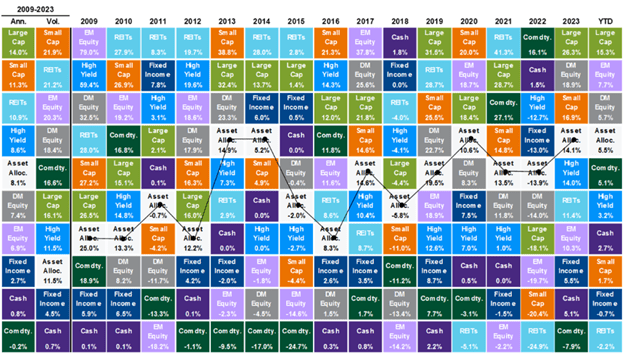

As is almost always the case, there are economic crosscurrents: some indicating the economy will remain strong, and some flashing warning signals. It is impossible to consistently predict how these crosscurrents will resolve. At best, those predictions are an educated guess. Our philosophy is not to create concentrated portfolios based on our macro views. The benefits of diversification can be shown by this “Periodic Table of Returns,” which shows no asset class consistently produces superior returns to other asset classes.

Source: JPMorgan

It is a core principle of our investing philosophy.

As always, we thank you for your trust in us. If you have any comments or questions, please feel free to contact me, your Portfolio Manager, or your Wealth Manager.

Related Articles

April 13, 2026

Watch Coldstream’s MarketCast for Second Quarter 2026

April 9, 2026

Turbulence: Navigating a Complex First Quarter

January 29, 2026

Artificial Intelligence: Boom or Bubble?