Insights

October 20, 2023

A Reversal of Fortune?

In Market Commentary

At the end of the second quarter, the S&P 500 was up 16.89% for the year, and bonds posted positive returns as well with the yield on the 10-year Treasury falling to 3.84%. With inflation moderating and growth steady, many market participants were predicting a “soft landing” scenario– inflation curtailed without a recession.

From Soft Landing to No Landing

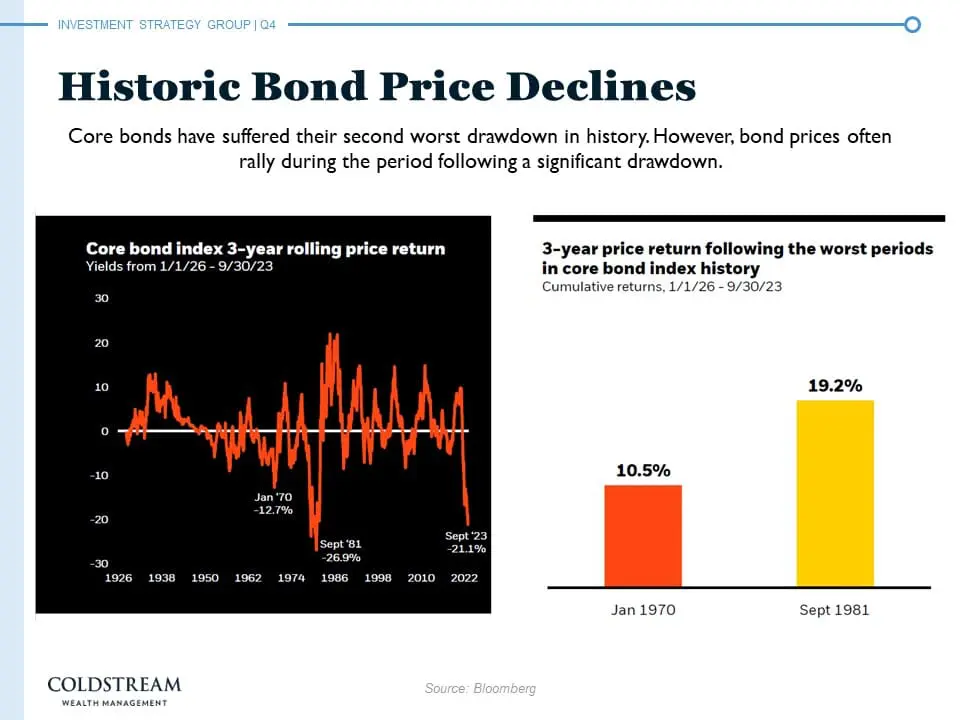

This scenario remained the dominant market theme through most of the third quarter. However, in late September and October, concerns about a “hot” economy and a continued high cost of borrowing changed the narrative from “soft landing” to “no landing”. As this new narrative took hold, both the equity and fixed income markets sold off, with the S&P 500 falling from 17.30% on September 15th to 11.53% on October 3rd and yields on the 10-year Treasury spiking to 4.80%. US core bonds have now had their second worst drawdown in history, and 30-year fixed income mortgages rose to their highest rate in 23 years.

Source: Bloomberg

With equities and fixed income both being down for the quarter, US financial markets fell back into their negative pattern of 2022. Counter-intuitively, these markets sold off, in part, because the US economy remains stronger than market participants anticipated. For example, US household excess savings are at $1.1 trillion dollars, much higher than previously thought which should support consumer spending, the largest component of GDP. While there has been an increase in credit card defaults recently, many households locked in low mortgage rates before the recent spike, and homeowners’ incomes in most cases can easily cover their mortgage payments. Other areas of the economy remain strong as well: corporate profitability, while declining slightly, has also exceeded expectations, and the labor market remains extremely tight.

An overheated economy raises the prospect of continuing inflation. While inflation has softened, it is still well above the Fed’s 2% target. As a result, the Fed indicated that it will keep interest rates higher for longer. The prospect of continuing inflation and high interest rates caused the sell-off in both the fixed income and equity markets.

Source: JPMorgan

Source: JPMorgan

There are two additional concerns that rates will stay higher for longer apart from the strong economy. The first is the necessity to fund the US fiscal deficit. The deficit is currently 98% of GDP, the highest level since the end of the Second World War. The deficit is funded by the issuance of Treasuries. Until 2022, the Fed was buying Treasuries as a means of keeping interest rates low to stimulate the economy. Given the recent bout of inflation, the Fed has stopped buying Treasuries while Japan and China have reduced their purchases of Treasuries as well. With increased issuance needed to fund the deficit and fewer buyers, Treasuries now have a supply/demand imbalance. Additionally, a significant portion of Treasuries mature in the near term, requiring the government to re-issue Treasuries at a higher rate, further increasing the deficit.

Source: Strategas

When rates spike, equities often suffer losses. Stocks that pay dividends often lose money as investors may turn to a Money Market Fund in which they can receive 5% on cash with very little risk, instead of investing in a stock with a dividend at a lower rate. In regard to growth stocks, an investor might ask why I would invest in a company for its future earnings potential when I can receive 5% on cash today. This partially explains why Money Market funds received inflows of $200 billion in the third quarter while the equity and fixed income markets fell.

The Way Out

Higher rates may already be impacting the economy, although the impact may not have shown up in the data yet. Many components of inflation have already started to decline. Shelter is currently the biggest driver of inflation, and the methodology used to determine shelter inflation is a lagging indicator (i.e., the current data is not necessarily what is actually happening in real time). Indeed, indications are that the housing market has begun to cool. We are also seeing some signs of a loosening in the labor market as wage growth has moderated. Although inflation may not fall to the Feds 2% target, we would not be surprised to see it continue to decline. The current higher interest rate environment, coupled with banks’ stricter lending standards, should slow the economy. In that case, the Fed could reduce interest rates and spark a rally in both the fixed income and equity markets. This is why, historically, bonds rally after a severe drawdown, as the “Historic Bond Price Declines” chart shows.

What Does This Mean For You

As we have repeatedly said in these market commentaries: (1) stay diversified and (2) do not try to time the market. In the short term, your portfolio could experience volatility, but if you “stay the course” over a longer period, returns become more predictable, and you should be able to reach your financial goals.

Source: JPMorgan

Again, we greatly appreciate your trust in us. If you have any questions, please feel free to contact your Wealth Manager, Portfolio Manager or me.

Related Articles

April 13, 2026

Watch Coldstream’s MarketCast for Second Quarter 2026

April 9, 2026

Turbulence: Navigating a Complex First Quarter

January 29, 2026

Artificial Intelligence: Boom or Bubble?