Insights

July 21, 2023

A New-Found Optimism (But Will It Last)

In Market Commentary

A year ago, stagflation was considered a plausible scenario for the US economy for the first time since the early 1980s. The Consumer Price Index (CPI) rose 9.1% in June 2022, and the Fed was unambiguously stating that it would “do what it takes” to curb inflation regardless of whether its actions put the economy into a recession. The Fed admittedly was late in switching from an accommodative to a restrictive monetary policy and many wondered whether the Fed, by aggressively raising the Fed funds rate, would cause a recession but not curb inflation. The US equity and fixed income markets reflected these concerns with both posting a yearly loss in 2022 for the first time in almost 50 years.

Contrast that economic environment to the environment this year. In June, inflation rose 4.6% using the Fed’s preferred measure, the Personal Consumption Index, and the economy is growing with GDP estimates at about 2% growth for the second quarter. Concerns about stagflation have been replaced with hope for, if not expectations of, a “soft landing” – a reduction in inflation to close to the Fed’s target of 2% without a recession. The US large cap equity and corporate debt markets have reflected this optimism with the S&P 500 up 17.04% at the end of the second quarter and high yield and investment grade debt markets predicting a low likelihood of significant corporate defaults.

Despite the current optimism, a soft landing is far from a certainty. Fed policy going forward, the resilience of US household spending, and corporate profitability will play a significant role in determining whether inflation can be contained while the economy continues to grow.

Fed Policy

The Fed’s primary tool for slowing inflation is to raise the Fed Funds rate, which accomplishes this by curtailing lending and slowing demand. The Fed has used this tool aggressively, raising the Fed Funds rate from 0% in January 2022 to 5.0 % today. These rate hikes successfully brought down the demand for goods and many types of services, but housing and labor costs are still rising. As inflation has not reached the Feds 2% target, the Fed has indicated that it will raise the Fed Funds rate again at its next meeting and could raise it more going forward depending on what the economic data shows.

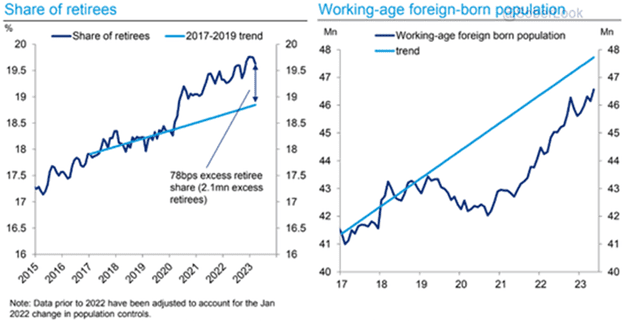

The US large-cap equity market reflects a belief that the Fed’s strategy is working and is pricing in a soft landing, but other economists, investors, and analysts do not agree. Some think that the Fed has already raised rates too high. They argue that it takes time for labor and housing costs to be impacted by rising rates, and once those rate hikes impact those and other costs, it will result in a recession. Others think the opposite: that the Fed will not be able to bring inflation down to its 2% target, and the rate of inflation will exceed the rate of growth despite the Fed’s rate hikes. They argue that there is a structural labor shortage that will keep costs high given the number of workers retiring and the US’ tight immigration policy.

Source: The Daily Shot

Recognizing that rate hikes can have a lagged effect, the Fed paused at its last meeting to analyze that impact.

US Households

Ultimately, whether the Fed is successful in executing a soft landing depends on the US consumer’s behavior. Consumer spending makes up approximately 70% of GDP. The pent-up demand for services after COVID has continued to fuel consumer spending but whether the US consumer continues spending despite the rise in interest rates will be a key determinant of whether the Fed can execute a soft landing. If consumers curtail spending, the need for labor should decline causing costs to fall. If, however, they curtail it too much, the US economy will most probably go into a recession. While the US consumer is still in a strong financial position, cracks are beginning to show.

Source: JPMorgan

Financial Markets

The equity and Treasury markets appear to be predicting different levels of confidence in the Fed’s ability to execute a soft landing. The S&P 500 is reflecting continuing confidence in the soft-landing scenario, returning 8.74% in the second quarter. Seven mega-cap tech stocks drove performance, with returns this year ranging from approximately 40% for Microsoft and Google to almost 200% for Nvidia. The pervasive attention focused on artificial intelligence (A.I.) was a significant reason for these stocks advancing, but so were the prospects of the end of the Fed’s tightening cycle, as lower interest rates would make these companies’ future earnings more attractive. Further, equity market volatility, a measure of market participants’ perception of risk, is at very low levels.

Source: JPMorgan

The VIX – an index of equity volatility

Source: Bloomberg

However, the calmness of the equity market is not reflected in the market for US Treasuries, which is driven by interest rate forecasts. Interest rates rose and prices fell in the fixed income markets generally for the second quarter on inflation and rate uncertainty. Volatility in the Treasury markets, measured by the MOVE index remained elevated, reflecting far more concern about the path of inflation and rates than the large-cap equity market has been displaying.

The Move – an index of treasury volatility

Source: Bloomberg

Corporate Earnings

As a result of the recent equity market rally, large cap equity market valuations are lofty. The typical justification for those valuations is that company earnings will grow into their valuations. Consensus earnings estimates for 2023 earnings are currently at 10.8%. For this rally to continue, earnings will most probably have to at least meet these estimates and probably beat them. While analysts have been reducing their earnings estimates, earnings are generally exceeding expectations so far this year. Corporate profitability will be impacted, however, if the economy falls into a recession or inflation re-accelerates.

As discussed above, it takes time for higher rates to impact economic activity, and increased borrowing costs could be a headwind for profitability going forward. Currently, however, corporate balance sheets are relatively strong, and most companies have sufficient cash to cover increased borrowing costs. Nonetheless, there are some early warning signs regarding corporate health as well, as corporate bankruptcies have increased significantly so far this year.

Source: Goldman Sachs

Our View, You, and the Uncertainty

Recent economic data has increased the possibility of a soft landing, but a recession in 2024 remains a plausible scenario. However, if the economy does go into a recession, we expect the recession to be relatively mild given the strength of the current economy.

Whether the Fed executes a soft landing, the economy goes into a recession, or inflation is persistent are all potential outcomes from the current economic situation. It would be a mistake to dramatically alter a diversified portfolio based on a view of which of these three outcomes might prevail. Concentrating portfolios based on a view of which outcome occurs could result in high returns but also result in steep losses. We may make small tactical shifts based on our views, but our investment philosophy is to maintain portfolio diversification. In the medium- to long-term, maintaining a diversified portfolio should enable you to participate when the equity market rallies and cushion losses when it declines. Staying with your financial plan should enable you to meet your financial goals.

As always, we thank you for your trust in us. If you have any questions or comments, please feel free to contact your Portfolio Manager, your Wealth Manager, or me.

Related Articles

April 13, 2026

Watch Coldstream’s MarketCast for Second Quarter 2026

April 9, 2026

Turbulence: Navigating a Complex First Quarter

January 29, 2026

Artificial Intelligence: Boom or Bubble?