Insights

October 8, 2013

The 3rd Quarter Winds Down

In Market Commentary

September 2013 marks the five-year anniversary of the financial market collapse in 2008; we have certainly come a long way in those five years. With the S&P 500 and the Dow eclipsing all-time highs and interest rates having stayed low for the longest stretch in 50 years, most investors have already received quite a benefit from the fount of cheap money. Since September 2008, a meaningful economic recovery has taken place. Look at the results since the equity markets bottomed out in March of 2009:

- Dow up 160.52%

- S&P 500 up 172.76%

- Russell 2000 small cap up 225.68%

- Emerging Markets up 160.59%

- International Developed Markets up 225.68%

This strong performance occurred despite slow global economic growth, political stalemate in Washington, a debt crisis in Europe, and a generally gun-shy investment community. Similarly, there is no shortage of concerns today, including Fed policy timing, government shutdowns, the debt ceiling debate, unemployment at 8%, and GDP growth stuck in the 2% range. However, we believe that many of these issues are unpredictable in the short term and almost impossible to base sound, long-term investment decisions on.

Instead, we focus on creating asset allocation strategies geared toward a client’s long term financial goals; selecting quality managers through sound due diligence, risk management, and based on long term investment results. It is our philosophy that long term earnings growth of great businesses, economic growth over time, and investments that capitalize on those trends should win out. We believe they will offset monetary inflation and provide for a quality retirement down the road. In other words, we focus on fundamental investment blocking and tackling over knee jerk short-term decisions or trying to predict the unpredictable.

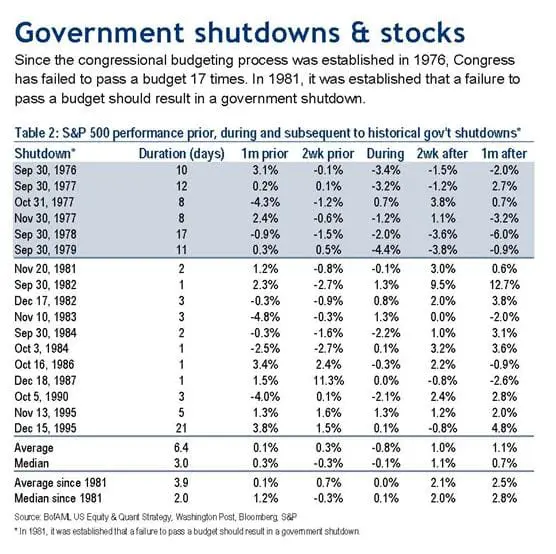

Having said this, as we look into the final quarter of 2013, the government shutdown is front and center. It is not the first time the markets have had to weather a government shutdown so we believe it is instructive to look at how the markets performed during these prior periods. This Merrill Lynch chart illustrates the performance of the markets during these periods historically.

It is mildly comforting to see that, overall, the market performed reasonably well ‘on average’ during these periods. No real big dips down or large rallies from this seemingly avoidable predicament. That being said, there is a much bigger event looming in mid October…the debt ceiling debate. If the debt ceiling is not raised, the Federal Government will run out of money and could potentially default on its debts. The specter of a US Government debt default is a much more serious calamity for the financial markets that the government shutdown on many fronts. At this time, the consensus is that lawmakers will once again carry these debates over the debt ceiling into the last hour but not allow a default to actually occur. Let’s hope so!

Overall, the economy is in the middle of a meager recovery. The recent turmoil out of Washington D.C. has the potential to derail the recovery but we feel that, in the end, it will not turn out to be a game changer for the economy. Cooler heads will eventually prevail and we will be on to the next crisis! In the meantime, corporate earnings and the markets have performed well and 2013 is shaping up to be another great year for investors and wealth creation.

Insights Tags

Related Articles

April 13, 2026

Watch Coldstream’s MarketCast for Second Quarter 2026

April 9, 2026

Turbulence: Navigating a Complex First Quarter

January 29, 2026

Artificial Intelligence: Boom or Bubble?