Insights

August 7, 2025

Planning Your Social Security Strategy: What to Consider When Claiming Benefits

In Financial Planning, Retirement

Claiming Social Security is one of the most important financial decisions you’ll make in retirement—and it’s far from one-size-fits-all. Your choice will affect not only the size of your monthly benefit, but also the total amount you may receive over your lifetime. Factors such as your health, life expectancy, marital status, income needs, and confidence in the future of the program all play a role. The labyrinth of rules and claiming strategies can make navigating the Social Security landscape feel overwhelming, even for well-informed individuals. In this article, Senior Wealth Manager and Planner Rich Merrifield outlines key considerations to help you make an informed decision that supports your long-term financial well-being.

It’s not uncommon for healthy individuals who live into their 90s to receive over $1,000,000 in lifetime Social Security benefits. Given the potential size of this payout, the strategy used to claim benefits can significantly impact one’s financial outlook in retirement. Thoughtful planning around this decision is therefore a critical component of a sound retirement strategy.

Full Retirement Age (FRA)

Understanding your Full Retirement Age (FRA) is essential when planning for Social Security. Your FRA is the age at which you are eligible to receive 100% of your retirement benefit.

- If you were born in 1960 or later, your FRA is 67.

- If you were born between 1955 and 1959, your FRA ranges from 66 and 2 months to 66 and 10 months, depending on your exact birth year.

You have three primary options for claiming Social Security retirement benefits, each with implications for your lifetime payout:

- Claim early – You can begin receiving benefits as early as age 62, but your monthly benefit will be permanently reduced.

- Claim at your Full Retirement Age (FRA) – You’ll receive 100% of your earned benefit.

- Delay your claim – For each year you delay past your FRA (up to age 70), your benefit increases, potentially resulting in a significantly higher lifetime payout if you live a long life.

Choosing when to claim is a strategic decision that should align with your overall retirement goals, health, and income needs.

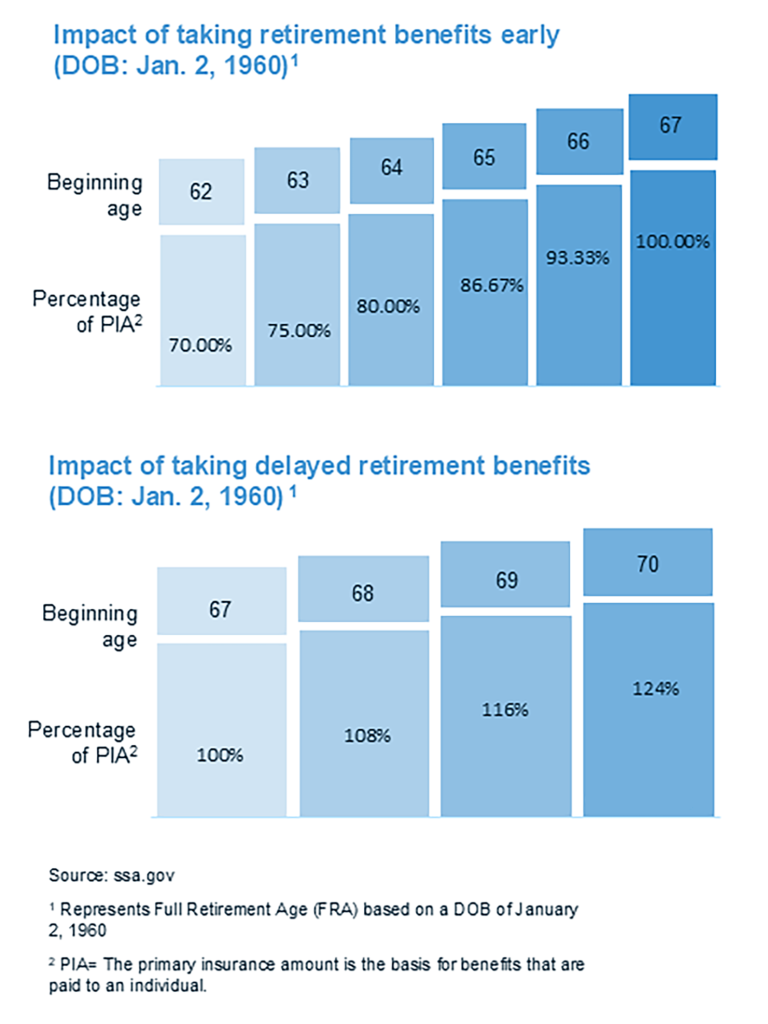

How Early Claiming Affects Your Benefits

You can begin claiming Social Security retirement benefits as early as age 62. However, doing so will result in a permanent reduction in your monthly payments. The reduction is calculated at five-ninths of 1% for each of the first 36 months you claim benefits before your Full Retirement Age (approximately 6.67% per year), and approximately five-twelfths of 1% for each additional month beyond those 36 months (or 5% per year).

To put this into more digestible terms:

- If your FRA is 67 and you start benefits at age 64, your monthly benefit will be about 20% lower than if you had waited until your FRA.

- Claiming at age 62 results in a 30% reduction in your monthly benefit compared to waiting until age 67.

This early reduction remains in effect for life, so it is important to consider your health, longevity expectations, and financial needs before deciding to claim early.

The Case for Delaying Your Benefit

On the other side of the coin, delaying your Social Security benefits beyond your Full Retirement Age (FRA) results in a permanent increase in your monthly payment. Using an FRA of 67 as an example, your benefit increases by 8% for each year you delay, up to age 70. This means that if you wait until age 70 to claim, your monthly benefit would be 24% higher than if you had claimed at 67. This strategy can significantly enhance your lifetime income—particularly if you expect to live well into your 80s or beyond.

Strategizing Your Claiming Decision

Choosing when to begin receiving Social Security benefits is a delicate balancing act with long-term financial implications. Three key factors often guide this decision:

1 – Life Expectancy & Health Status

If you’re in good health and anticipate a longer lifespan, delaying Social Security benefits may be a smart move, as it can lead to higher overall lifetime payouts. The break-even point—where the total value of delayed benefits surpasses benefits claimed at your Full Retirement Age (FRA) typically occurs in your early 80s.

On the other hand, if you or your spouse have health concerns or a shorter life expectancy, claiming benefits earlier may help ensure you receive the maximum lifetime value from the program.

2 – Marital Status

Your marital status can significantly influence your optimal Social Security claiming strategy. Each situation carries unique rules and opportunities:

Married

Couples have several strategic options for coordinating their Social Security benefits, especially when there is a difference in age or income. A common approach is for the higher-earning spouse to delay benefits to maximize the survivor benefit, while the other spouse may claim earlier to provide income in the meantime.

While both spouses are living, the maximum spousal benefit is 50% of the other spouse’s benefit at Full Retirement Age (FRA). Importantly, spousal benefits do not increase if you delay claiming beyond your FRA. However, if you claim them before reaching FRA, the benefit is permanently reduced—the earlier you file, the greater the reduction.

You are eligible to receive either your own benefit or the spousal benefit, whichever is higher, but not both. In addition, you cannot receive spousal benefits unless your spouse has already filed for their own benefit.

Widowed

Surviving spouses may be eligible for survivor benefits as early as age 60 (or 50 if disabled). A common strategy is to claim a survivor benefit first and then switch to your own benefit later (or vice versa), depending on which provides the greater lifetime value.

Unlike during the lifetime of both spouses, a surviving spouse is entitled to receive the greater of the two benefits—their own or their late spouse’s. This includes any delayed retirement credits the deceased spouse earned by postponing their benefit beyond Full Retirement Age. In essence, delaying can enhance not just your own retirement income, but also the survivor benefit available to your spouse.

These decisions are especially impactful and warrant careful analysis.

Divorced

If you were married for at least ten years, are currently unmarried, and are age 62 or older, you may be eligible to claim benefits based on your ex-spouse’s record—even if they have remarried. This does not affect their benefit and can be a valuable option, especially if your own benefit is lower.

Single

For single individuals, the decision often centers on health, life expectancy, and cash flow needs. With no spousal considerations, the choice to claim early or delay is largely about personal longevity expectations and financial independence. When a single person delays their Social Security benefit to age 70, they’re essentially betting on their own life expectancy and not the combined longevity of two lives, as with a married couple. If they live well into their 80s or beyond, the increased monthly payments from delaying can lead to higher total lifetime benefits. However, if they pass away earlier, they may end up receiving less overall than if they had claimed benefits earlier.

3 – Confidence in Social Security’s Future

Many individuals consider the long‑term stability of Social Security when deciding when to claim benefits. Even though the program remains backed by federal law, demographic shifts and funding dynamics have raised questions about potential adjustments to future benefit levels. These considerations sometimes influence decisions around:

- Timing — Some may choose to claim earlier due to concerns that benefit levels could be reduced for future retirees.

- Longevity of payments — Individuals may wonder whether higher delayed benefits will be preserved throughout retirement.

- Policy changes — Public discussion about raising the FRA, modifying cost‑of‑living adjustments (COLAs), or taxing a larger portion of benefits may affect future benefit values.

The Economic Impact of Cutting Social Security Benefits

Creating unnecessary fear among retirees about dramatic Social Security cuts is both misleading and unhelpful. While it’s true that the program faces long-term funding challenges, large, across-the-board benefit reductions are neither economically practical nor politically viable.

Social Security serves as a financial foundation for millions of retirees, and cutting benefits would have broad and potentially severe economic consequences for our country. For many individuals, Social Security is their primary or only source of income. A reduction in benefits could lead to greater financial insecurity, lower consumer spending, and increased dependence on other public assistance programs.

Communities with older populations would likely experience local economic slowdowns as retirees cut back on discretionary purchases. Furthermore, lower-income households—who rely most heavily on Social Security—would be disproportionately affected, potentially widening income and wealth inequality.

With a significant percentage of voters either currently receiving Social Security or expecting to rely on it in the near future, the program remains a politically sensitive issue. Lawmakers are well aware that major benefit cuts would likely result in strong public backlash and risk triggering a significant national economic downturn. This reality reinforces the likelihood that future reforms will focus on gradual, measured adjustments—such as modest tax increases, raising the retirement age, or recalibrating benefit formulas—rather than drastic reductions in benefits.

Final Thoughts

Claiming Social Security benefits is a highly personal decision that should be tailored to the unique circumstances of you and your family—including health, income needs, marital status, and long-term goals. As always, please don’t hesitate to reach out to your advisor for guidance in exploring your options and developing a Social Security strategy that aligns with your overall retirement plan.

* Certified Financial Planner Board of Standards Inc. owns the certification marks CFP®. CERTIFIED FINANCIAL PLANNER™ and CFP® in the U.S., which it awards to individuals who successfully complete CFP Board’s initial and ongoing certification requirements. The Accredited Investment Fiduciary® (AIF®) is administered by the Center for Fiduciary Studies, the standards-setting body of fi360.

Insights Tags

Related Articles

April 29, 2026

Financial Habits Everyone Should Cultivate

March 13, 2026

Navigating Divorce – A Women & Wealth Podcast

March 5, 2026

Choosing the Right Trustee: One of the Most Important Decisions in Your Estate Plan