Insights

December 15, 2025

Volatility: The Price of Admission to Long-Term Returns

In Investments, Wealth Strategy

The term “volatility” often carries a bit of a charge because it’s common for investors to conflate “volatility” with losses or danger. But volatility and risk are not synonymous, and understanding what volatility is and the role it plays in an investment strategy can help investors make smarter decisions.

What is volatility?

Volatility is a measure of the degree of variation in the price of an investment or portfolio over time. All investments come with some level of volatility as their prices change over time, but volatility isn’t an inherently negative factor.

Volatility is most commonly measured by standard deviation, which looks at how spread out a group of numbers are from the average. Higher standard deviation means returns are more spread out; for example, consider two hypothetical stocks with the same average annual return of 8% but different standard deviations:

- Stock 1 has a standard deviation of 5%, meaning its price generally fluctuates between 3% and 13%.

- Stock 2 has a 20% standard deviation, with swings usually ranging from -12% to 28%.

It’s important to note that measures of volatility don’t indicate the direction of movement, nor do they tell you how likely any given return is given historical data.

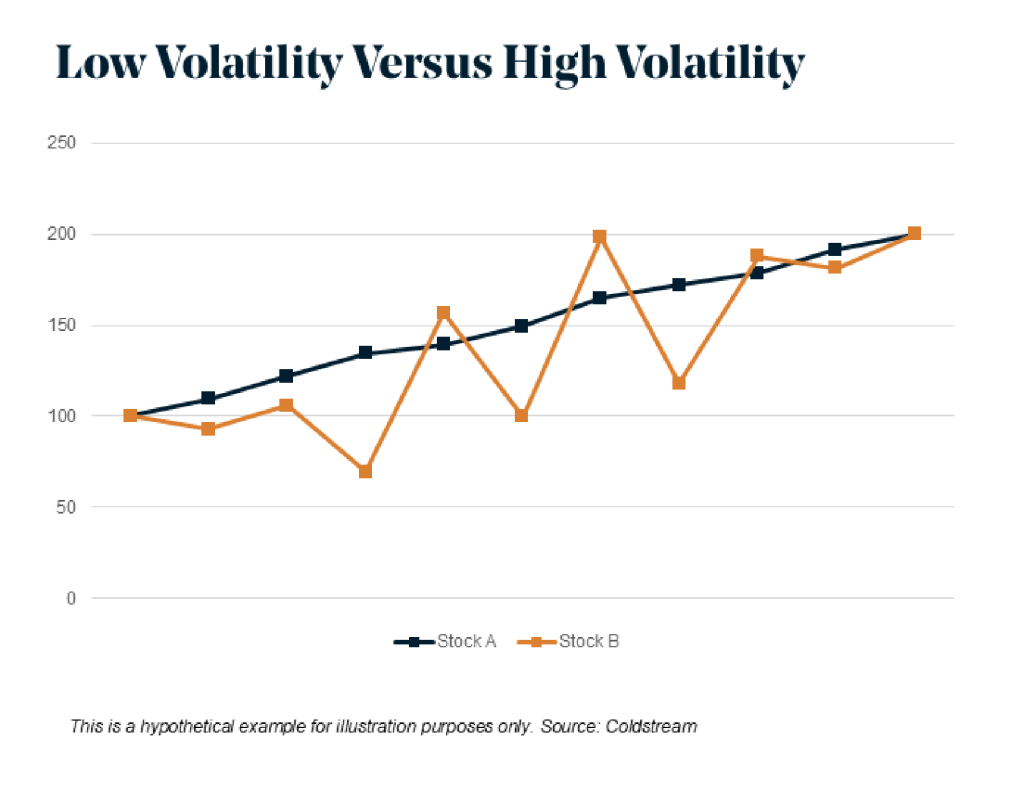

The example below shows ten years of returns of hypothetical investments Stock A and Stock B. They both start and end at the same values—$100 at the beginning and $200 at the end—but Stock A has a fairly smooth path along the way, whereas Stock B fluctuates significantly. They have the same average rate of return, but Stock B has a much higher standard deviation or—in other words—much higher volatility.

What drives volatility?

Volatility is driven by changes in demand and expectation. There is no one driver behind changes in stock prices—many factors can contribute, ranging from company-specific changes such as innovations, changes in leadership, and earnings reports to economic factors such as interest rate changes and political changes, and even including broader influences like swings in market sentiment. Volatility often increases with uncertainty, which can lead to fear and cause investors to react, affecting short-term market movements. The reality is that the market is highly complex, and volatility can be caused by a wide variety of factors.

How does volatility compare with risk?

Risk refers to the likelihood of losing capital or failing to achieve investment objectives, both primary concerns for most investors. Volatility, on the other hand, is neutral—it just describes variability in prices. Volatility can contribute to risk in a portfolio, but it also represents opportunity for long-term investors who are patient and disciplined. The reason investors take on the risk of [hopefully temporary] losses is to achieve the longer-term goal of capital growth.

The general rule of thumb is that the more risk you are willing to take on, the more potential you have for long-term gains. Higher volatility—or wider fluctuations—in addition to presenting a higher risk of loss also represents a higher chance of gains as well. This is why investors with a higher tolerance for risk can invest more aggressively: those who are willing to weather greater volatility have historically generally been rewarded with higher returns over the long term.

Loss aversion

Knowing that taking greater risk in a portfolio is a path toward potentially greater returns doesn’t make it any easier when we experience volatility. Behavioral economists have demonstrated that people feel the pain of losses more strongly than they feel the pleasure of gains. The result of this phenomenon, called “loss aversion,” is that large price swings downward can trigger strong emotional reactions and lead investors to equate volatility with danger. The emotional distress of seeing portfolio losses can interfere with the ability to exercise discipline and objectivity.

The answer is to understand volatility, to tailor your portfolio to your tolerance for risk, and to ensure your portfolio has adequate diversification. Often, the worst thing an investor can do is react to short-term market swings by trying to time the market, which can result in selling low and missing out on the best days—which often occur following a downward market swing.

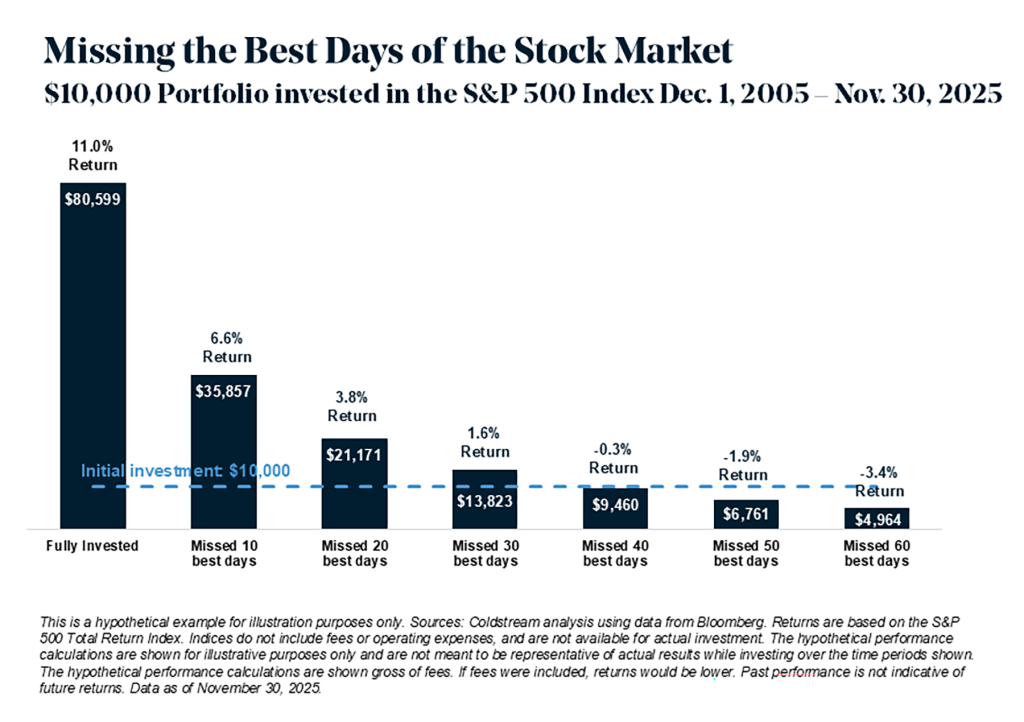

The example below shows a portfolio with a starting value of $10,000 invested in the S&P 500 Index over 20 years from Dec. 1, 2005 to Nov. 30, 2025. Over that time, a portfolio that stayed invested would have earned an 11.0% annualized return, with an ending value of $80,599. Missing just the ten best days of the stock market during that time cuts the portfolio’s growth to an annualized return of only 6.6% and an ending value of $35,857, a reduction of more than 50%. Missing the 20, 30, 40 or more best days would have resulted in even worse outcomes.

Managing Volatility

Focus on the long term

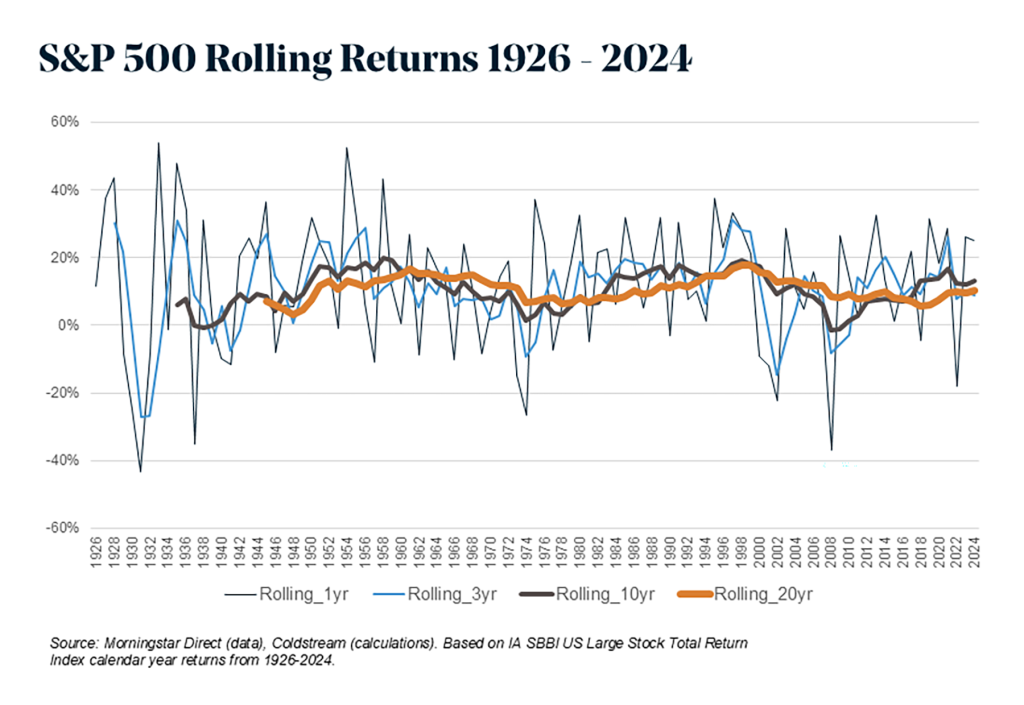

Volatility looks less significant when measured over longer time periods. In the chart below, each line represents the S&P 500 Index return from 1926-2024, but showing different rolling periods. The shorter periods of one and three years are highly volatile, whereas the longer 10-year and 20-year rolling returns are greatly smoothed out.

Investors who stay focused on long-term investing are less affected by short-term fluctuations and can weather greater volatility. That said, investors with a shorter time horizon may want to limit volatility in order to avoid the impact of large downward swings at a time when they will need to access their capital.

Diversify

In addition to long-term investing, another important tool for mitigating the impact of volatility on a portfolio is diversification. Spreading investments among different asset classes that experience differing levels of fluctuations can reduce exposure to any single source of volatility and help smooth out portfolio returns.

Know your Tolerance for Risk

Finally, knowing your tolerance for risk can help you feel comfortable staying invested and weathering volatility. Your investment advisor can help you build a portfolio tailored to your comfort level, with an expected standard deviation that you are willing to tolerate in exchange for long-term growth potential.

Conclusion

Volatility is part of the territory when it comes to investing. The market can be noisy, particularly during periods of uncertainty or upheaval. No one can consistently predict the right time to get in or out of the market; successful market timing is extremely difficult. But investors who are willing to experience some ups and downs in the market are often rewarded with better long-term outcomes. Patience, discipline, and objectivity are critical qualities for successful long-term investing. Think of volatility as opportunity—the price of admission to long-term return.

Your Coldstream wealth manager can work with you to craft a long-term investment strategy that suits your tolerance for risk and investment objectives, helping you manage volatility through discipline and diversification.

Related Articles

January 2, 2026

New Gifting and Contribution Limit Changes For 2026

December 5, 2025

10 Trends to Watch For in 2026: Welcome to the Future

November 3, 2025

Maximizing Your Employer Benefits