Insights

March 13, 2023

The Silicon Valley Bank Collapse: A Significant Event But Not a 2008-Like Threat to the Financial System

In Market Commentary

As many of you may have seen, Silicon Valley Bank (SVB) experienced a classic “run on the bank” last week and, on Friday, was placed in receivership by the Federal Deposit Insurance Corporation (FDIC). As part of Coldstream’s mission, we thought it important to communicate our views on why the bank failed, what the potential implications of the failure are, and what the rules are regarding accounts you may hold with financial institutions.

Why SVB Failed

SVB was unique among banks as its customers were primarily start-up companies. The great majority of those start-ups were not profitable and were funded through selling a significant amount of equity in a “funding round”, the proceeds of which were deposited in SVB. These proceeds far exceeded the $250,000 limit on the FDIC’s deposit insurance.

Prior to the recent rise in interest rates, start-ups were often able to raise additional financing when the proceeds from their previous equity raise dwindled, and the start-ups replenished their deposits from the proceeds of those financings. SVB took those deposits and invested in longer term bonds, most of which paid very little interest as they were purchased prior to the recent rise in rates. Accounting rules allowed SVB to price these bonds at the amount they paid for them, not at the price the same types of bonds were trading for in the open market.

However, since the Fed began aggressively raising interest rates, start-ups have had an extremely difficult time raising additional financings and began withdrawing their deposits at SVB at a rapid rate. To meet those withdrawals, SVB sold those longer- term bonds, and since the coupon on those bonds were paying far less than inflation or short-term interest rates, SVB had to sell those bonds at a significant loss. After the loss was announced, SVB tried to sell additional stock, but no one would buy it. SVB had an unusually high concentration of depositors who held far more in deposits than the FDIC insurance maximum and, those depositors became very concerned that they would suffer losses if SVB failed. As a result, large numbers of them tried to withdraw their deposits, causing the bank to fail.

The Potential Implications from the Failure

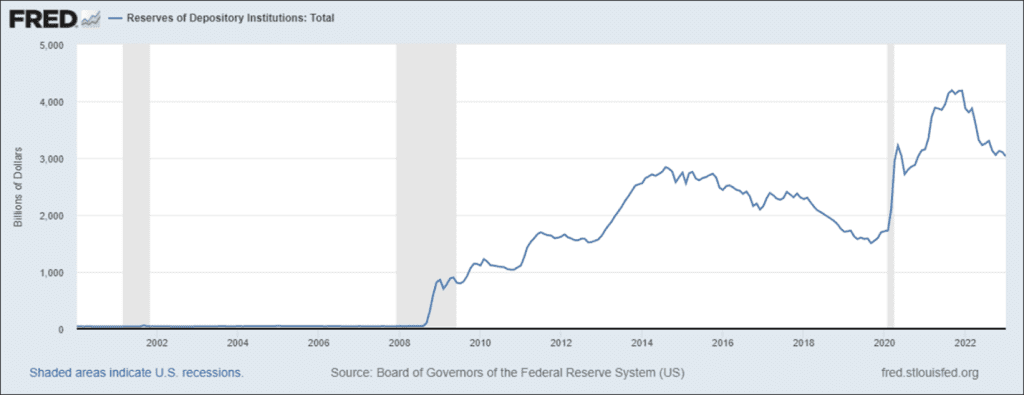

Most importantly, SVB’s failure is not a 2008-like event that threatens the US financial system. Large US financial institutions are in far better economic condition than they were in 2008. Laws and regulations coming out of the Great Financial Crisis required banks and other large financial institutions to own a significant amount of extremely safe assets, far more than they were required to own in 2008. Large banks are also extremely limited in the amount of risky assets, such as junk bonds and sub-prime mortgages, that they are allowed to own. Those regulations also require banks to keep cash reserves at the Fed that can be used in the event the bank suffers losses. Currently, financial institutions have over $3 trillion dollars on reserve at the Fed, compared to only $45 billion on reserve in 2008.

Bank Reserves:

Although the financial system as a whole is secure, we may well see additional fall out from SVB’s collapse in other small to mid-sized regional banks. Even though SVB’s depositors were very different from typical bank retail depositors, a bank failure often causes “contagion” as depositors worry about the strength of their financial institution. While small- and mid-sized regional banks may be well run, they do not have the financial wherewithal of the large US banks. In fact, on Sunday, a New York regional bank also failed as a large number of their depositors closed their accounts. Recognizing the danger of contagion, the Fed announced that they would make SVB’s depositors whole even if they exceeded the FDIC’s insurance limit. Hopefully, the Fed’s actions will calm depositors; however, we would not be surprised to see some additional bank casualties from the SVB fall out.

What This Means for Your Accounts

The FDIC insures up to $250,000 per account holder at a single bank regardless of how many accounts the account holder has at the bank. Thus, whether a depositor has one account or five accounts at a single bank, the total amount of insurance the depositor has is $250,000 at that bank. For joint accounts, each account holder is insured separately. If each account holder has equal rights to withdraw funds from the account, the FDIC will assume the account is owned equally. Thus, if you have one joint account in a financial institution with equal withdrawal rights, you and your co-account holder will each be insured for $250,000, and the total insurance for the account will be $500,000. If you would like to discuss the best way to maximize your FDIC insurance in various types of accounts (for example revocable and irrevocable trust accounts), please contact your Wealth Manager or Portfolio Manager.

Securities positions in brokerage accounts held by our custodians – Charles Schwab, TD Ameritrade, and Fidelity – are legally segregated from the assets of those custodians and are not affected if the custodian becomes insolvent. Similarly, money market mutual funds own liquid short-term instruments and are not subject to the risk of the sponsor of the fund or the custodian holding the fund. Cash balances in Fidelity accounts are swept to money market funds owning short-term government securities. However, cash balances at Charles Schwab and TD Ameritrade are swept to a number of underlying banks, including banks affiliated with Schwab and TDA, where they are subject to FDIC coverage limits for each bank as described above. We are closely monitoring cash positions in client accounts that could be in excess of coverage limits, and for managed accounts, we may take action to reduce excess cash balances by substituting other cash positions (such as money market funds) that do not have this exposure.

In regard to your portfolio, these events may lead to continued volatility in both the equity and bond markets. However, to date, other than in the stocks of regional banks, the decline in equity markets has been contained, and Treasuries have rallied, serving their traditional role of protecting portfolios in times of volatility. One of the significant mistakes some investors make is to overreact in stressful environments such as this one. We do not pretend to be able to successfully time the market, but we do know that maintaining portfolio diversification over the long run should enable you to meet your financial goals.

We appreciate your trust in us. If you have any further questions, comments, or concerns, please feel free to contact your Wealth Manager, Portfolio Manager or me.

Related Articles

April 13, 2026

Watch Coldstream’s MarketCast for Second Quarter 2026

April 9, 2026

Turbulence: Navigating a Complex First Quarter

January 29, 2026

Artificial Intelligence: Boom or Bubble?