Insights

July 11, 2025

The Return of Diversification

In Investments, Market Commentary

Quarter Highlights

- Stabilizing Global Growth Amid Evolving Trade Dynamics

Despite recent macroeconomic, policy, and geopolitical challenges, global economic resilience is strengthening. Investor attention is shifting from U.S.-centric growth to a more diversified global perspective. - U.S. Tariff Policy Presents Ongoing Growth and Inflation Risks

While recession fears have eased, lingering tariff threats and policy uncertainty may weigh on growth and inflation. Strong household and corporate balance sheets help buffer against major economic setbacks. - Fiscal Policy Takes Center Stage with the “One Big Beautiful Bill” (OBBB)

A renewed wave of federal spending is expected to drive investment in U.S. infrastructure, defense, and advanced manufacturing, favoring industrial equities, municipal bonds, and real assets. However, elevated deficits and inflation concerns may pressure long-duration Treasuries and complicate the Fed’s policy flexibility. - Federal Reserve Awaits Clear Signals for Rate Cuts

The Fed is likely to hold rates steady into late 2025 unless inflation or labor data weakens meaningfully. Fiscal improvements may occur but could come at the cost of slower economic growth. - U.S. Equities Remain Resilient Despite Volatility

Markets have fully recovered, but policy disruptions and valuation concerns leave little margin for error. Moderate economic growth continues to support earnings and upward market momentum. - Fixed Income Yields Remain Attractive in a Low-Spread Environment

With credit spreads tightening near historic lows and a supportive global economic environment, fixed income assets with higher yields remain appealing for investors. - Diversification Gains Importance in a Shifting Global Landscape

With active global policymaking and persistent higher interest rates, diversifying across geographies and asset classes is increasingly vital. While U.S. structural strengths persist, the country’s relative outperformance may moderate as other global economies gain traction.

Global Economic Resilience in a Shifting Landscape

The global economy in 2025 has navigated a turbulent year marked by trade disruptions, geopolitical tensions, and concerns over monetary and fiscal stability. As the barrage of alarming headlines subsides, a clearer economic narrative is emerging, often described as “headline fatigue.” This shift allows for a more focused assessment of growth prospects, with resilience becoming a defining theme across major economies despite earlier setbacks.

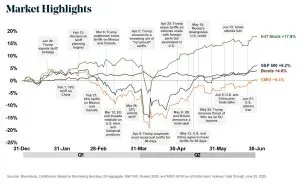

Source: Coldstream, Data through June 30, 2025

In the U.S., recession fears have faded. Forecasts have stabilized, with strength in consumer spending and corporate balance sheets supporting a more constructive outlook—even as tariff uncertainty lingers. China’s growth remains firm, underpinned by aggressive policy support, while Europe, despite energy and geopolitical challenges, shows signs of a 2026 rebound driven by fiscal stimulus.

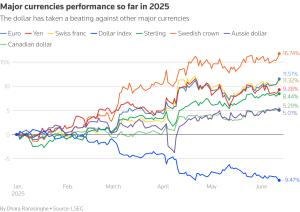

Investor sentiment is adjusting accordingly. The U.S. dollar has weakened to a three-year low, despite favorable rate differentials and ongoing market volatility. This evolving dynamic underscores the need for greater geographic diversification as global leadership becomes less concentrated.

Source: Reuters, Data through June 2025

U.S. Tariff Policy Outlook: A Moderated but Persistent Challenge

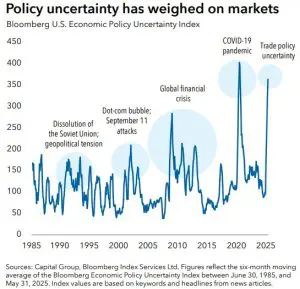

The Trump administration’s retreat from its most aggressive tariff proposals has alleviated fears of severe economic fallout, significantly lowering recession risks for 2025. With peak trade policy pessimism fading, the U.S. economy is on a more stable footing, supported by resilient consumer and corporate fundamentals. However, the lingering effects of elevated tariffs are expected to create challenges, with the average effective U.S. tariff rate projected to reach 17%—the highest since the 1930s Smoot-Hawley era—compared to 2% at the start of 2025.

Despite the moderated tariff stance, trade policy uncertainty remains a concern. Legal challenges to unilateral tariff actions suggest a shift toward sector-specific tariffs rather than broad country-based measures. Additionally, the administration is likely to leverage tariffs as a negotiating tool, embedding ongoing “tariff noise” into the economic landscape. While less severe than initially feared, these dynamics will continue to shape U.S. growth prospects, requiring businesses and investors to navigate a more complex trade environment. Trade deals typically take 18 months to finalize, making deadline extensions and renewed tensions possible.

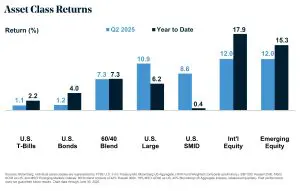

Source: Capital Group, Data from June 30, 1985 through May 31, 2025

One Big Beautiful Bill: Investment Implications

The “One Big Beautiful Bill” (OBBB), signed into law on July 4, 2025, introduces significant fiscal and economic changes, driving investment opportunities while fueling concerns about debt and inflation. The legislation’s tax incentives and spending initiatives are projected to boost U.S. equity markets, particularly in manufacturing, small businesses, and traditional energy sectors, as policies favor domestic production and fossil fuels over clean energy. However, the bill’s substantial debt increase could push Treasury yields higher, making high-yield corporate and municipal bonds attractive amid tight credit spreads and a solid economic backdrop. Real estate investments, especially in Qualified Opportunity Zones, also stand to benefit from enhanced tax breaks.

The OBBB’s fiscal expansion may further weaken the U.S. dollar, already at a three-year low, which could prompt investors to look overseas, particularly in light of the recent outperformance of international equities. Cuts to social programs like Medicaid and Medicare may dampen consumer spending for some, though tax relief for workers and seniors could support discretionary sectors.

Federal Reserve and Fiscal Policy Outlook: A Tightrope Walk

The Federal Reserve faces a challenging environment in 2025, balancing trade uncertainties, persistent inflation, and resilient jobs data. With inflation above target, the potential to rise further in Q3 due to tariffs, and short-term inflation expectations climbing, the Fed risks policy missteps. Currently the market is anticipating two rate cuts in the second half of 2025; however, Fed Chair Jerome Powell has indicated there is no urgent need for action.

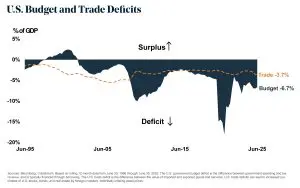

Fiscal policymakers are equally constrained, focusing on debt sustainability while managing growth. The OBBB is expected to boost growth, but its benefits will likely be somewhat neutralized by the combined impact of tariffs—in what could effectively be a tax hike—and reduced federal spending. This mix should gradually improve the budget deficit but at the cost of slower economic growth. Policymakers must proceed cautiously to avoid a sharp slowdown that could exacerbate historically high deficits, requiring careful coordination to maintain economic stability.

Source: Coldstream, Data from June 30, 1995 through June 30, 2025

U.S. Equities Outlook: Navigating Challenges with Resilience

The U.S. equity markets have demonstrated robust recovery, with the S&P 500 achieving a new record high in late Q2 2025, erasing earlier losses in the quarter. Key sectors such as Financials, Industrials, and Utilities contributed to the rally, but the Technology sector—led by the “Magnificent 7″—was the primary catalyst. Strong earnings from major tech firms and growing optimism about AI-driven productivity gains since the April 9 low have fueled this rebound. However, the broader economic environment suggests that investors should be prepared for continued near-term market volatility.

Source: Coldstream, Data through June 30, 2025

U.S. Bond Market Dynamics: Rising Risk Premiums

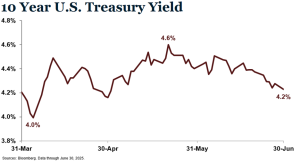

The U.S. bond market experienced some volatility in the second quarter, as 10-year Treasury yields rose from a low of 4.0% early in April to a peak of 4.6% in mid-May, before settling at 4.2% at quarter-end. Nominal bond yields reflect two components: breakeven yields, which indicate stable inflation expectations, and real yields, which signal growth outlooks and risk premiums. Real yields have risen significantly and remain high, even with Federal Reserve rate cuts, driven by increased Treasury supply, concerns over fiscal sustainability, and waning demand for U.S. dollar-based assets.

Source: Bloomberg Data through June 30, 2025

The yield curve’s longer end has steepened, reflecting these risk premiums, as both private and foreign investors shift toward shorter-duration Treasuries. This trend suggests that even if inflation remains contained, elevated risk premiums at the long end could sustain higher borrowing costs. The bond market’s dynamics highlight growing investor caution, with fiscal and demand concerns likely to keep yields volatile and borrowing costs elevated in the near term.

Conclusion: Embracing a Broader Investment Approach

For much of the past decade, U.S. mega-cap tech stocks dominated returns, overshadowing the benefits of diversification across assets, sectors, or regions and leading to elevated valuations. However, early 2025 marked a shift, with a rebound in Chinese tech, Europe’s pivot to expansionary fiscal policies, and concerns over the U.S. economic outlook driving investor interest toward global markets. A weakening U.S. dollar further bolsters the case for international exposure, highlighting opportunities beyond the U.S.

Looking forward, diversification—both geographic and across asset classes—will be essential. While U.S. structural strengths in innovation, scale, and productivity persist, its relative outperformance is likely to moderate as other global economies gain traction. Broader diversification—including alternatives and private markets—alongside active management, will be critical to managing risks, enhancing returns, and capitalizing on emerging opportunities in this evolving cycle.

As always, we are truly honored in the trust you have placed in Coldstream to help guide you through the ever-changing market landscape. Please don’t hesitate to reach out if you have any questions.

Information is current as of 6/30/2025, drawn from third-party sources believed to be reliable but not guaranteed as to accuracy, timeliness or completeness. None of the information provided constitutes an opinion or a recommendation or a solicitation of an offer to buy or sell any particular security. Coldstream analyses are not intended to provide, and should not be construed to constitute, complete accounting, insurance, investment, legal, or tax advice. The investment strategies and securities shown may not be suitable to you. Past performance is no guarantee of future returns. May not be reproduced, republished, or distributed without prior written consent. Questions and comments may be directed to your advisor.

* The CFA Institute owns the certification marks CFA® and Chartered Financial Analyst®. CAIA® is a registered certification mark owned and administered by the Chartered Alternative Investment Analyst Association® in the United States.

Related Articles

January 29, 2026

Artificial Intelligence: Boom or Bubble?

January 13, 2026

Perspective After a Volatile Year: What 2025 Reinforced About Diversification and Discipline

January 12, 2026

Watch Coldstream’s MarketCast for First Quarter 2026