Insights

August 10, 2025

Save More for Retirement with Your Health Savings Account

In Company Benefits, Retirement, Wealth Strategy

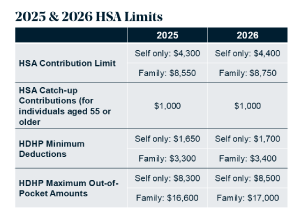

As you plan for retirement, consider using one of the best options for building tax-advantaged savings—a Health Savings Account (HSA). An HSA is a medical savings account available to anyone enrolled in an HSA-compatible high-deductible health plan (HDHP), are covered under a “direct primary care service arrangement” (in which the monthly fee does not exceed $150 per month for individual coverage or $300 per month to cover multiple people), or are enrolled in a bronze or catastrophic health plan offered through the Marketplace. For the year 2025, the IRS defines an HDHP as a plan with a deductible of at least $1,650 for an individual or $3,300 for a family; in 2026, that increases to a deductible of $1,700 for an individual and $3,400 for family coverage.

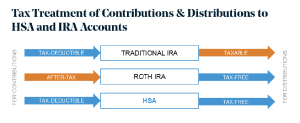

Funds are contributed to an HSA pre-tax and grow tax-free. As long as the money is spent on qualified expenses, withdrawals are also tax-free. Since most people will face substantial medical expenses in their later years, an HSA is a great option to supplement IRAs, 401(k)s, and other tax-advantaged retirement accounts. Below are some frequently asked questions regarding this savings strategy.

How much can I contribute to my HSA?

For the 2025 calendar year, the contribution limit for individual HSAs is $4,300 per year, and the contribution limit for a family is $8,550 per year. For the 2026 calendar year, that increases to $4,400 for an individual and $8,750 for a family.

If the HSA owner is 55 years of age or older, they can also make an additional $1,000 catch-up contribution annually.

Note: The maximum HSA contribution includes both employer and employee contributions.

Sources: https://www.irs.gov/pub/irs-drop/rp-24-25.pdf, https://www.irs.gov/pub/irs-drop/rp-25-19.pdf, https://www.fidelity.com/learning-center/smart-money/hsa-contribution-limits

How will an HSA affect my taxes?

HSA contributions are made on a pre-tax basis. You can withdraw the money at any time, and distributions are also tax-free as long as you spend the money on qualified medical expenses incurred after the HSA was established.

Source: Coldstream

What is a qualified withdrawal?

“Qualified” medical expenses include deductibles, fees, and other healthcare expenses incurred on behalf of yourself, your spouse, and any dependents. There is no time limit for claiming a reimbursement from your account, but you’ll need to document your claimed expenses.

Can I withdraw money to pay other expenses?

Non-qualified withdrawals are permitted at any time but will be included in your taxable income. If you are under the age of 65, you will also pay a 20% tax penalty. The penalty is waived if you are permanently disabled or when withdrawals are made after your death.

Can an HSA be used to pay insurance premiums?

Generally speaking, funds from your HSA may not be used to pay insurance premiums; however, there are a few exceptions where you can use your HSA to pay for the following:

- Long-term care insurance

- Healthcare continuation coverage (such as coverage under COBRA)

- Healthcare coverage while receiving unemployment compensation under federal or state law

- Once you reach age 65, you may use your funds free of taxes and penalty for qualified medical expenses, as well as to pay for Medicare Parts A, B, and D premiums, and Medicare HMO premiums. However, premiums for a Medicare supplemental policy such as Medigap do not qualify as eligible expenses.

Do HSAs include fees?

Yes, and they vary from plan to plan. We have found that Fidelity Investments offers a competitive HSA. Some of the benefits Fidelity’s HSA currently offers are:

- Opening Fee:There are no account opening fees or transfer fees.

- Minimum Balance:There is no minimum balance to open a Fidelity HSA.

- Maintenance Fees: There is no monthly or annual maintenance fee and there is no minimum balance that must be held in cash.

- Integration: They offer one integrated account with no transfers back and forth between different entities. (Other HSA plans generally require clients to open a separate brokerage account along with the cash that is being held with the HSA custodian.) Fidelity has consolidated these two accounts into one account.

Do HSAs come with investment options?

Many plans offer investment options. At Fidelity, all the investment options available in a regular Fidelity brokerage account are also available within their HSAs, including commission-free, low-cost index funds.

How can I use my HSA to save more for retirement?

Begin by fully funding your account each year. Many people use HSA funds to cover current medical costs, which provides immediate tax savings. However, if you can afford to pay current medical expenses out-of-pocket, your HSA balance can continue to grow tax-free. This effectively increases your retirement savings and your tax savings.

Does this strategy make sense for everyone?

For some people, paying current medical costs out-of-pocket may be challenging. The deductible alone can be several thousand dollars, with fees and co-pays adding further expenses. But for people who are young, healthy, or wealthy, this strategy is especially appealing:

- Young people have ample time for the HSA funds to grow over years, or even decades.

- Healthy people, with lower medical bills, will have more disposable income to contribute to their HSA, with fewer occasions for withdrawals.

- For wealthy people, with the ability to pay current medical costs and fully fund their retirement savings, an HSA provides a great option for accumulating tax-free funds.

Remember that no other retirement vehicle gives you tax advantages on both contributions and distributions. However, if you do use your HSA to supplement your retirement funds, it’s important to invest in assets that will grow over time—similar to your IRA. Using cash accounts or other low-return investments will diminish the HSA’s advantage.

If you have questions about HSAs, or if you are interested in how an HSA might fit into your retirement strategy, your Coldstream advisor would be happy to discuss your options.

Supplemental Q&A

Do I need earned income to contribute to an HSA account?

No. Contributions may be made by you or on your behalf, even if you are retired, have no income, or your income is less than your contributions.

Are employer contributions to an HSA taxable income?

Generally, contributions made by an employer to the account of an eligible employee are excludable from an employee’s income and are not subject to federal income tax, Social Security, or Medicare taxes.

Can both spouses make a catch-up contribution?

If both spouses are eligible and have established an HSA in their name, and turn 55, then both can make catch-up contributions. If only one spouse has an HSA in his or her name, only that spouse can make a catch-up contribution.

If I am turning 65 this year, can I still make an HSA contribution?

Once you enroll in Medicare, you can no longer contribute to your HSA. However, you may be eligible to make a prorated contribution during the year you turn 65 before you enroll in Medicare.

Is there a deadline to make contributions to an HSA account?

Yes, yearly contributions should be made by your tax filing deadline, generally April 15th of the following year.

How does a spouse’s health coverage impact contribution limits?

If you have an HSA, but your spouse has separate health coverage, the following special rules may apply:

- If your spouse has an individual HSA-qualifying plan, then you would have to subtract your spouse’s contribution from the maximum that you could otherwise contribute. In other words, although the IRS treats married couples as a single tax unit, if both spouses have self-only coverage, each spouse may only contribute up to $4,300 in 2025, in separate accounts.

- If your spouse has non-qualifying family coverage that includes you, it makes you an “ineligible individual,” and you may not contribute to an HSA.

Can I transfer my IRA into an HSA?

Yes, the law allows a one-time transfer of IRA assets to fund an HSA. The amount transferred may not exceed the amount of one year’s HSA contribution and individuals must be otherwise eligible to open an HSA.

Transfers are not taxable as IRA distributions. On the other hand, amounts transferred into an HSA from an IRA cannot be deducted as an HSA contribution. (Recall that HSA contributions are deducted from your paycheck before taxes if you contribute to an HSA through your employer, or, if you make your own HSA contributions, you deduct it on the first page of your tax return. IRA transfers are not eligible for this tax return deduction.)

A few other key reminders on IRA transfers:

- A transfer can only occur once per lifetime.

- The IRA and the HSA must be in the name of the same person.

- Traditional and Roth IRAs are straightforward and allowed. SEP or Simple IRAs are a bit more complicated and not allowed by the IRS.

- Most importantly, any transfer that takes place counts toward your annual HSA contribution limit (see 2025 contribution limits above). This means that in the year in which you execute the transfer, plus the 12 months following the transfer, you must be eligible (i.e., covered by a high-deductible health plan) to contribute into an HSA. It would make sense to wait until you are certain that you will be eligible for 12 full months of coverage to take advantage of this one-time opportunity. Remember that if you change jobs, retire, or for any other reason change health plans, you may not be eligible for the entire year. Please also note: waiting until you are 55 to use your transfer opportunity will allow you to take advantage of the extra $1,000 catch-up contribution, giving you more tax savings.

Are HSA funds portable?

The plans are portable and can be rolled over year after year (no “use it or lose it”). The IRS allows each HSA account holder to “roll over” their funds to a new HSA provider every 12 months and still maintain the tax-advantaged status of the HSA. However, there is no limit on the number of trustee-to-trustee transfers (e.g., payments to doctors, pharmacies, etc.) you can make.

Can I use my HSA to pay for other elective procedures?

A partial list of items that you can include in figuring your medical expense deduction and HSA-qualified medical expenses can be found in IRS Pub 502.

Can I use the money in my HSA to pay for medical care for a family member?

Yes, you may withdraw funds to pay for the qualified medical expenses of yourself, your spouse, or a dependent, without tax penalty.

What happens when I pass away?

There are three basic scenarios outlining what happens to your HSA funds after your death:

- If your spouse is the beneficiary of your HSA, the account just becomes his/her HSA. (That is, it’s not an “inherited HSA,” it is just a normal HSA, now owned by your surviving spouse.)

- If somebody other than your spouse is the beneficiary of your HSA, the account loses its HSA status. It becomes a regular taxable account, and the full value of the account is taxable as income to the beneficiary in the year of your death, but for the exception listed below. *

- If your estate is the beneficiary of your HSA, the account ceases to be an HSA, and the value of the account is included as income on your final tax return.

*If, within one year of the date of death, your non-spouse beneficiary (other than your estate) pays any of your qualified medical expenses that were incurred before your death, the amount of those expenses is subtracted from the amount that is taxable to the beneficiary.

DISCLAIMER: THIS MATERIAL PROVIDES GENERAL INFORMATION ONLY. COLDSTREAM DOES NOT OFFER LEGAL OR TAX ADVICE. ONLY PRIVATE LEGAL COUNSEL OR YOUR TAX ADVISOR MAY RECOMMEND THE APPLICATION OF THIS GENERAL INFORMATION TO ANY PARTICULAR SITUATION OR PREPARE AN INSTRUMENT CHOSEN TO IMPLEMENT THE DESIGN DISCUSSED HEREIN.

CIRCULAR 230 NOTICE: TO ENSURE COMPLIANCE WITH REQUIREMENTS IMPOSED BY THE IRS, THIS NOTICE IS TO INFORM YOU THAT ANY TAX ADVICE INCLUDED IN THIS COMMUNICATION, INCLUDING ANY ATTACHMENTS, IS NOT INTENDED OR WRITTEN TO BE USED, AND CANNOT BE USED, FOR THE PURPOSE OF AVOIDING ANY FEDERAL TAX PENALTY OR PROMOTING, MARKETING, OR RECOMMENDING TO ANOTHER PARTY ANY TRANSACTION OR MATTER.

Insights Tags

Related Articles

May 15, 2026

Irrational Decisions in Investing

April 29, 2026

Financial Habits Everyone Should Cultivate

April 14, 2026

Finding Tax Efficiency in an Era of Increasing Tax Obligations