Insights

January 1, 2025

Ready to Use Your 529 Plan?

In Family Needs, Wealth Strategy

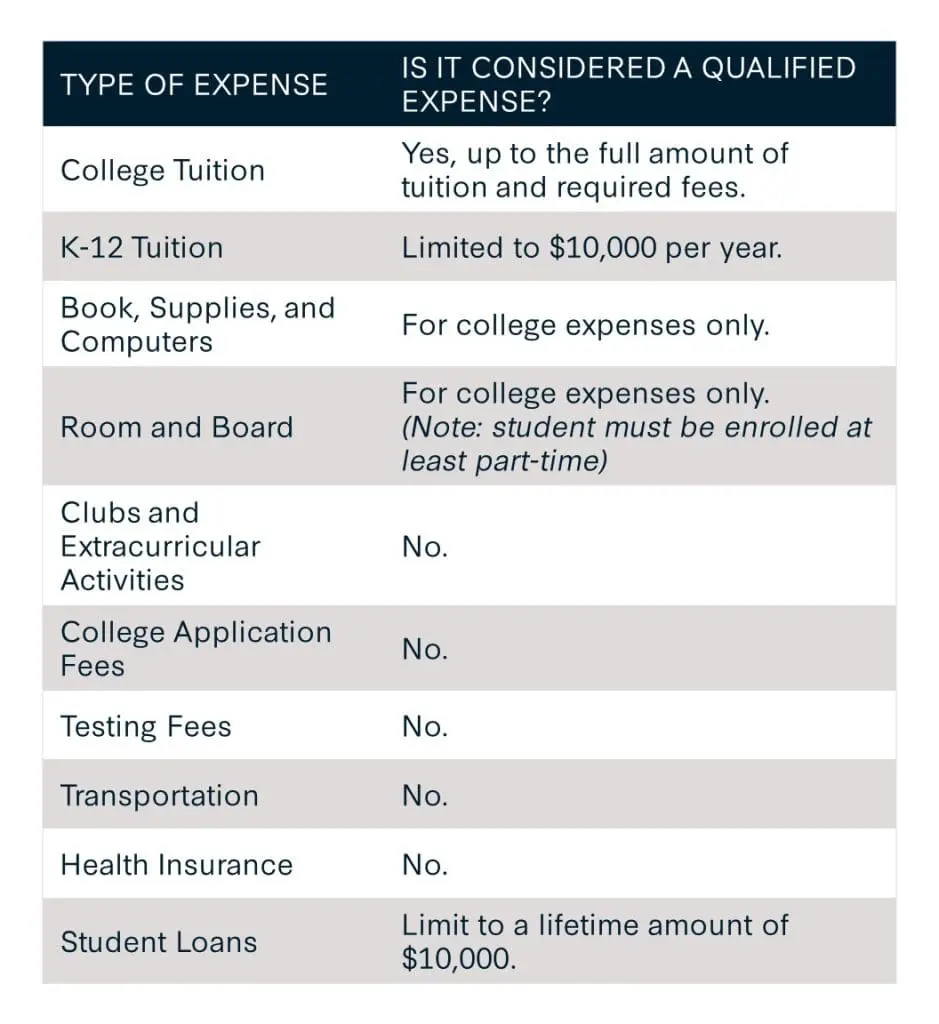

As your college student heads off to campus, you may be wondering what expenses the 529 plan can cover versus which expenses are better paid out-of-pocket. Let’s take a closer look at expenses your student may encounter during their academic year and which of those qualify under your 529 plan.

What Are “Qualified Expenses?”

Qualified expenses are defined as amounts paid for tuition, fees, and other related expenses for an eligible student that are required for enrollment or attendance at an eligible educational institution. The benefit of a 529 account is that contributions can grow tax-free and the earnings are also tax-free (as long as the distributions are used for qualified expenses). However, earnings on distributions used to pay for non-qualified expenses can be subject to ordinary income tax and incur a 10% tax penalty.

Source: “529 Qualified Expenses: What Can You Use 529 Money for?” by Martha Kortiak Mert; Savings for College; Sept. 18, 2024; https://www.savingforcollege.com/article/what-you-can-pay-for-with-a-529-plan

Tuition

Your 529 plan can be used to pay for tuition and fees at colleges, universities, vocational or trade schools, and other eligible institutions. This also includes study abroad programs approved for credit by the student’s home university.

For a complete list of 529-eligible universities in the U.S. and abroad, click here.

Books, Supplies, and Computers

Books and supplies required to participate in a class are considered a qualified expense. This includes textbooks, lab equipment, and other mandatory items. Miscellaneous office supplies or additional reading material not required for coursework would be considered non-qualified.

529 plans can also be used to purchase a computer, computer accessories (e.g., monitor and mouse), software required for coursework, and internet access as long as the beneficiary primarily uses these items while enrolled in an eligible institution.

Room and Board

Room and board can make up a large portion of a student’s total college bill. Aside from tuition, it is often the second largest expense families face. Visit the College Board Trends in College Pricing website for their most recent report on college costs, including the average cost for undergraduate room and board.

Living On-Campus – students enrolled at an eligible college will be eligible to have their 529 plan cover room and board (typically consists of housing and a meal plan).

Living Off-Campus – students living off-campus can still use their 529 to cover rent, groceries, and utilities. However, their reimbursement limit must be less than or equal to the college’s cost of attendance (COA) allowance.

- For example: Wendy is a freshman attending the University of Washington. The stated on-campus housing and meal plan allowance at UW is $3,000 for a 3-month term ($1,000 per month). Wendy has chosen to live off-campus and spends $1,500 per month on rent and groceries. Thus, the 529 account can reimburse her for up to $1,000. Wendy will need to cover the remaining $500 out-of-pocket.

Qualified expenses must be incurred during the academic term in which the student was enrolled. This means that if the student signs a one-year lease for off-campus housing, but is not enrolled in classes over the summer, the housing costs for the summer months would be considered a non-qualified expense and should be paid out-of-pocket.

If the student’s parents own the house or condo in which the student plans to live in during college, you cannot use a 529 plan distribution to pay the mortgage. This would be considered a non-qualified expense. Parents may be able to charge the student rent on this home; however, this strategy is not recommended because the student would use the 529 to pay rent and the parent would pay income tax on the rental income received – thereby negating the tax-free benefit of the 529 withdrawal.

Club and Extracurricular Activities

Extracurricular activities like gym memberships, club fees, or dues for sports, fraternities, or sororities are not qualified expenses covered by a 529 plan. However, if your student plans to live in a fraternity or sorority, you may be able to use your 529 plan to cover fraternity or sorority housing costs (up to the university’s COA allowance for room and board).

College Application and Testing Fees

While college application and testing fees may be required for admission, they are not required for enrollment or attendance. Therefore, they are not qualified expenses.

Transportation

Transportation expenses to and from college are not considered qualified expenses. This includes on-campus parking, bus fare, gas and mileage driving to/from campus, or plane tickets.

There may be an exception: if transportation costs are charged by the university as part of a comprehensive tuition fee or identified as “required for enrollment or attendance,” the expense may be considered qualified.

Health Insurance

If your student is not covered by your family’s health insurance policy, you could be required to purchase health insurance through the college. Health insurance or medical bills incurred while at school are typically non-qualified expenses.

There may be an exception: if health insurance costs are charged by the university as part of a comprehensive tuition fee or identified as “required for enrollment or attendance.” In that case, the expense may be considered qualified.

Student Loans & K-12 Tuition

Thanks to the 2019 SECURE Act, you can use a 529 plan to payoff up to $10k in lifetime maximum student loan debt. Additional legislation from the Tax Cuts and Jobs Act states that qualified 529 education expenses can include up to $10k per beneficiary per year for K-12 education at public, private, and parochial school.

It’s important to note that while these are considered qualified expenses at the Federal level, there are still a handful of states (including California and Oregon) that see the K-12 distributions as non-qualified expenses when it comes to state taxes. In these states, account owners can still be subject to state taxes and penalties.

As a rule of thumb, we recommend using the 529 to save enough to cover college expenses. This is because the beneficiary will benefit more from compounding years of tax-deferred growth the longer the funds remain invested. If the beneficiary has an excess amount saved in the 529 or will have college costs covered by another means, then you can look to use the plan to cover K-12 tuition.

How Much Can I Withdraw Each Year?

The maximum amount you can withdraw tax-free from a 529 plan annually is equal to the total amount of qualified education expenses less any other federal tax benefits or credits. Most federal education tax credits are only available to families who meet income requirements, so Coldstream families with higher income may be phased out or not receive these credits at all.

When Should I Start Withdrawing from a 529 Plan?

We recommend taking 529 plan distributions in the same calendar/tax year as the qualified expense, so they can be properly reported on your tax return. You cannot have a qualified expense in one year and a 529 distribution in another.

529 plans typically allow the owner or beneficiary to have reimbursements deposited directly into their bank account. You can also elect to have a check mailed to the account owner, beneficiary, or directly to the university.

Tip: If you choose to have the 529 send the check to the school directly, be sure to include the Student ID number in the memo line.

If you have any further questions about the benefits of starting a 529 Savings Plan or using an existing 529 account, please reach out to your Coldstream team.

Additional Sources:

- https://www.savingforcollege.com/article/what-you-can-pay-for-with-a-529-plan

- https://www.savingforcollege.com/article/what-you-can-t-pay-for-with-a-529

- https://www.savingforcollege.com/article/using-your-529-plan-to-pay-for-room-and-board

*All of Coldstream’s staff shall attain the required licenses and designations necessary for his/her position. Certified Financial Planner Board of Standards Inc. owns the certification marks CFP® and Certified Financial Planner™ in the U.S.

Insights Tags

Related Articles

June 4, 2026

Becoming Financially Independent: A Practical Checklist for Young Adults

May 28, 2026

Building a Financial Foundation: Books for Young Adults

May 15, 2026

Irrational Decisions in Investing