Insights

July 31, 2025

Qualified Charitable Distributions (QCDs) Are Gaining Momentum: How Retirees Are Rethinking Charitable Giving After the One Big Beautiful Bill (OBBB)

In Financial Planning, Philanthropy, Tax Planning

Attention, Charitable Givers!

The recently passed One Big Beautiful Bill Act (OBBBA) is reshaping how Americans approach charitable giving—especially among retirees. While the legislation introduces a modest above-the-line charitable deduction for non-itemizers, it limits the benefits of itemizing charitable gifts, which particularly impacts higher-income households. In this shifting landscape, Qualified Charitable Distributions (QCDs) are gaining serious momentum—and for those senior taxpayers who are subject to Required Minimum Distributions (RMDs), they are in many cases the most tax-efficient way to give.

What Changed Under the OBBB?

The OBBB extends key provisions from the 2017 Tax Cuts and Jobs Act, including a significantly higher standard deduction:

- $15,750 for single filers (2025)

- $31,500 for joint filers (2025)

- + $1,600 per person for individuals over 65

- + Up to $6,000 per person under the new senior deduction (based on Modified Adjusted Gross Income—the phaseout begins at $150k for married couples and $75k for single filers)

In short, most taxpayers will now benefit more from the standard deduction, making it harder to realize any tax benefit from itemizing charitable donations.

Here are more ways the OBBB reshapes the giving equation:

- New Adjusted Gross Income (AGI) Floor: Itemized charitable deductions now face a 0.5% AGI floor. That means no deduction applies until charitable gifts exceed 0.5% of income.

- New Cap for High Earners: A 35% cap now limits the value of charitable deductions for high-income taxpayers. Even if you’re in the 37% bracket, your deduction maxes out at 35% (e.g., a $10,000 donation yields just a $3,500 deduction instead of $3,700). This takes effect in 2026.

- Above-the-Line Deduction for All: Non-itemizers can now deduct up to $1,000 (single) or $2,000 (married) for cash donations.

These changes weaken the case for itemizing charitable gifts, particularly for retirees with stable income and limited itemized deductions—making QCDs more compelling than ever.

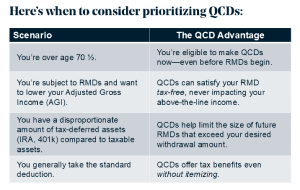

Why QCDs Stand Out

A Qualified Charitable Distribution allows individuals aged 70½ or older to transfer up to $108,000 (2025 limit; indexed annually) directly from their IRA to a qualified charity. For married couples with separate IRAs, that limit effectively doubles.

Here’s what makes QCDs uniquely powerful:

- They count toward your Required Minimum Distribution (RMD) but are not included in your taxable income.

- They reduce your Adjusted Gross Income (AGI), which may reduce overall tax liability and Medicare premiums, while increasing eligibility for other deductions or credits.

- They bypass the need to itemize, offering tax advantages even for those taking the standard deduction.

- They avoid the new 0.5% AGI floor and 35% cap; restrictions that now reduce the effectiveness of itemized charitable gifts.

A Case Study

Consider George, age 74, who is charitably inclined and must take a $50,000 RMD from his IRA this year. He also holds a taxable brokerage account with highly appreciated stock—shares originally worth $5,000 that are now valued at $25,000. George initially plans to donate the stock to his favorite nonprofit to avoid capital gains and support a good cause.

But here are the issues:

- George and his spouse take the standard deduction, which—between the base amount, age 65+ boost, and new senior deduction—totals over $40,000 at their income level.

- Since they don’t have other significant itemized deductions, George’s $25,000 charitable gift won’t clear the standard deduction threshold, so it yields no additional tax benefit.

- Even if he were able to itemize, under the new 0.5% AGI floor, only the portion above that threshold would qualify.

Instead, George opts to make a $25,000 QCD from his IRA. This move:

- Satisfies half of his RMD.

- Excludes the $25,000 from his taxable income.

- Delivers a full charitable impact—without needing to itemize or worry about AGI limitations or deduction caps.

For George, the QCD proves to be more tax-efficient than donating appreciated assets—especially in a world where itemizing is harder to justify.

The Bigger Picture: Planning Around OBBB

The One Big Beautiful Bill encourages broader giving among most taxpayers by offering small incentives to non-itemizers—but for those with significant charitable intent or large RMDs, the math increasingly favors making use of QCDs.

Source: Coldstream

Looking Ahead

While the OBBB brings some welcome enhancements—like the modest universal charitable deduction—it also quietly erodes the tax value of traditional itemized giving. QCDs, by contrast, can sidestep these limitations and offer tax efficiency along with your philanthropic efforts.

For retirees who are charitably inclined and subject to RMDs, QCDs offer a cleaner, more efficient way to give—one that may ultimately help you give more, keep more, and simplify your tax picture.

Should you have any questions, please do not hesitate to reach out to your wealth management team to explore how these changes may impact your specific situation.

Happy giving!

DISCLAIMER: THIS MATERIAL PROVIDES GENERAL INFORMATION ONLY. COLDSTREAM DOES NOT OFFER LEGAL OR TAX ADVICE. ONLY PRIVATE LEGAL COUNSEL OR YOUR TAX ADVISOR MAY RECOMMEND THE APPLICATION OF THIS GENERAL INFORMATION TO ANY PARTICULAR SITUATION OR PREPARE AN INSTRUMENT CHOSEN TO IMPLEMENT THE DESIGN DISCUSSED HEREIN.

CIRCULAR 230 NOTICE: TO ENSURE COMPLIANCE WITH REQUIREMENTS IMPOSED BY THE IRS, THIS NOTICE IS TO INFORM YOU THAT ANY TAX ADVICE INCLUDED IN THIS COMMUNICATION, INCLUDING ANY ATTACHMENTS, IS NOT INTENDED OR WRITTEN TO BE USED, AND CANNOT BE USED, FOR THE PURPOSE OF AVOIDING ANY FEDERAL TAX PENALTY OR PROMOTING, MARKETING, OR RECOMMENDING TO ANOTHER PARTY ANY TRANSACTION OR MATTER.

Certified Financial Planner Board of Standards Inc. owns the certification marks CFP®, CERTIFIED FINANCIAL PLANNER™ and CFP® in the U.S., which it awards to individuals who successfully complete CFP Board’s initial and ongoing certification requirements. Investments & Wealth Institute® (the Institute) is the owner of the certification marks CIMA®, and Certified Investment Management Analyst®. Use of CIMA®, and/or Certified Investment Management Analyst® signifies that the user has successfully completed the Institute’s initial and ongoing credentialing requirements for investment management professionals.

Related Articles

January 2, 2026

New Gifting and Contribution Limit Changes For 2026

November 28, 2025

Gifts to the Grandkids: Key Planning Considerations

November 17, 2025

Charitable Giving After the “One Big Beautiful Bill”: Why 2025 Is the Year to Act