Insights

April 5, 2022

How Do I Estimate My Spending?

In Financial Planning, Wealth Strategy

One of the most common questions we receive at the onset of a new relationship is, “how do I know if my spending is reasonable?” High-income families often lack clarity on what their annual budget is and how that spending may change when they decide to retire. Our goal in reviewing expenses is to provide perspective around what level of spending is sustainable and optimal to achieve your long-term goals. Whether ‘vocational freedom’ is a near-term or long-term goal, everyone can benefit from the simple act of tracking household spending. Financial publications often suggest using an expense tracking software application (e.g., such as Quicken or Mint). However, many find that route to be a rather time-consuming endeavor and often causes people to lose steam in the process. Let’s take a look at an alternative approach that is far less time-intensive and designed to arrive at a sufficiently reliable spending figure. This approach can be used for anyone looking to better understand their spending habits, as well as those in the beginning phases of budgeting for retirement.

Use Your Tax Return as a Starting Point

It’s important to understand your spending habits while you are gainfully employed, so you know the amount to be replaced in retirement without your monthly paycheck. For most people, their desired retirement lifestyle closely resembles their pre-retirement lifestyle, but with an extra eight hours of freedom each day! If you’re within ten years of retirement, this exercise is essential.

Once your prior year’s tax return is complete, you can use this simple equation to estimate your annual spending:

Gross Income minus Taxes Paid minus Savings = Spending

This calculation provides a high-level perspective of your spending. Using this figure as a base can allow you to dig deeper into the details and determine how these expenses might change in retirement.

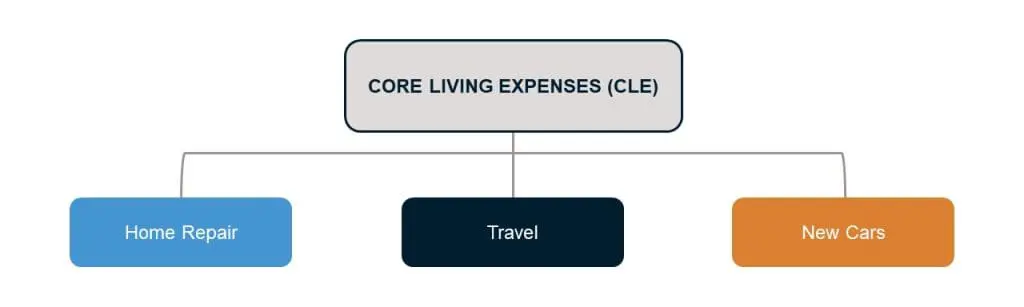

Determine Core Living Expenses

To arrive at a more detailed spending figure, first calculate your Core Living Expenses (CLE). Your CLE represent all those things you pay for monthly, quarterly, semi-annually, or annually and that, for the most part, you can expect to pay for in perpetuity. Your CLE will be the biggest part of your future inflation-adjusted spending in retirement. Once you have a good estimate of your CLE, you can create satellite spending goals for items like travel, major home repairs, and car replacements, which typically don’t neatly fit the reoccurring annual frequency of your CLE.

Break Out Fixed Expenses Versus Variable Expenses

Your CLE includes all your fixed expenses like mortgage payments, property taxes, insurance, and even the cable / streaming bill. As a category, fixed expenditures change the least in retirement. And they are also the simplest to forecast when you do expect a change. For example, if you plan to pay off your mortgage prior to retirement, its removal from retirement spending projections is straightforward.

The variable spending components of our CLE is where most of us struggle to arrive at reliable spending figures. These are items such as groceries, dining, clothing, personal care, and gift giving. If you find it challenging to calculate reasonable estimates for variable spending categories, try the simple technique below before you pull your hair out combing through files and credit card statements.

Visualize Your Variable Expenses

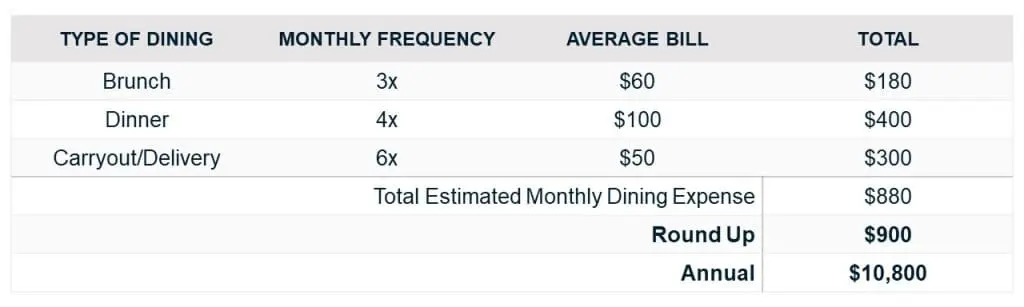

Using dining as an example — try pondering the patterns of your dining experiences. First, estimate how many times in a month you dine out for brunch, and what an average bill comes to. Then, do the same for dinners, carryout, and food delivery. Finally, total the subcategories for dining and round up the figure. Afterwards, you’ll want to begin tracking the accuracy from month-to-month. While the monthly figure will vary, check in after twelve months and see how close you came to your projected annual figure and adjust your projection if necessary. Now identify five variable spending categories you feel the least in touch with and perform this exercise for each. This simple technique will provide insight and add confidence as you work to determine a more specific annual spending forecast.

Review Your Credit Card Summary

Another helpful resource can be your credit card company. Almost all credit card issuers provide an annual spending summary — breaking down your expenditures into dining, travel, transportation, medical care, and other categories. Some transactions won’t be captured correctly, and the categories may not perfectly align if you use multiple credit cards. However, absolute precision isn’t the goal. Check your issuer’s website for past annual summaries and make a quick history of your spending by category. If the figures are relatively stable over time, you probably have a good baseline for future projections. Just don’t forget to add expenses that you pay for by check or direct debit, such as mortgage payments, insurance, and taxes.

Build Your Spending Estimates into Your Financial Plan

Working with a financial planning professional to create a comprehensive financial plan for your family is the best way to track spending in order to achieve your lifestyle goals and adequately prepare for retirement. The key is starting early, and well before you are ready to step away from work. We use estimates of spending in our initial planning, but the real value comes from revisiting those estimates each year and finetuning your patterns of saving and spending. This allows us to make small adjustments as necessary to ensure a successful plan upon retirement. Additionally, it provides peace of mind so you can enjoy ‘vocational freedom’ knowing we’ve diligently thought through the variables and discussed the unknowns. If you would like additional information or guidance on this topic, your team at Coldstream is here to help.

Related Articles

May 28, 2026

Building a Financial Foundation: Books for Young Adults

May 15, 2026

Irrational Decisions in Investing

April 29, 2026