-

DISABILITY ADVISORY SERVICES

IN PURSUIT OF BETTER OUTCOMES

Disability Advisory Services

DAS OVERVIEW

BETTER OUTCOMES

Living with a disability can be complex – financially, physically and emotionally.

Coldstream Disability Advisory Services (DAS) combines experienced Wealth Management and disability advocacy services in pursuit of better outcomes for clients.

We are the trustworthy handoff attorneys seek.

WEALTH MANAGEMENT

Coldstream’s experienced financial fiduciary team create sustainable investment plans focused on the following:

- Investment Advisory Strategies

- Personalized Financial Planning

- Broad Diversification

- Risk Management

- Tax and Estate Planning

ADVOCACY

Knowledge is power. Our DAS Project Managers have the experience, relationships, and resources to navigate a wide array of disability-related challenges that transcend money management and financial planning.

Examples of DAS advocacy in action:

- Accessibility and life modifications

- Specialized equipment solutions

- Home care planning

- Travel and recreational enablement

- Health and wellness resources and strategies

- Community resources and mentoring

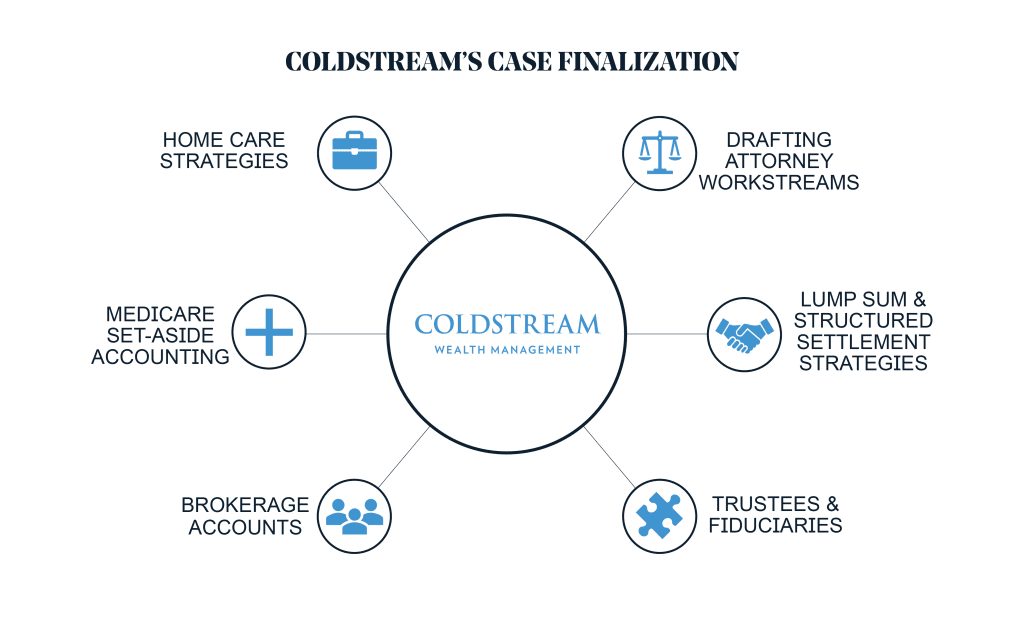

CASE FINALIZATION

Deep knowledge & professional networks in each of these categories provides meaningful benefits to attorneys and their clients.

Guided by a dedicated DAS team member, we collaborate towards closing the case quickly and skillfully.

Resources

Access our full library of resources here.

Loading...

-

Disability Advisory Services Sponsors WSAJ

Coldstream’s Disability Advisory Services (DAS), always dedicated to delivering holistic financial guidance to individuals with a disability who have received a financial settlement, is proud to announce their comprehensive gold sponsorship with the Washington State Association for Justice (WSAJ) for the second year in a row. The “oldest and largest civil justice advocacy organization in [...] -

Special Needs Trust

Examining uses beyond minors and diminished capacities scenarios – Special Needs Trusts can be an important tool for those who’ve experienced traumatic injury. [...] -

Making a Settlement Last: Advice for Attorneys, Legal Teams, and Clients

Lengthy hours are spent arriving at a settlement agreement or achieving a verdict. Most of the time, these monetary settlements are awarded to individuals and families who are not equipped to manage this sudden wealth. A financial disbursement can cause a range of reactions from immediate spending, extreme prudence, or depositing it in a personal [...] -

DAS Case Study: Greg’s Long-Standing Injury

Meet Greg Disability: Paraplegic In 2015, we were introduced to Greg. At the time, he was in his late 30’s and became a paraplegic as a teenager. Greg’s original injury settlement had grown substantially over the years, and he had worked to accumulate wealth from his career in the technology industry. Greg also had a [...] -

DAS Case Study: Sam’s Disability Settlement

Meet Sam Disability: C-4 Quadriplegic We had the pleasure of meeting Sam in 2009. When he visited our office for the first time, he was in his 20’s and had recently received a significant personal injury award due to a disabling accident. As a result of the accident, Sam was left a complete C-4 quadriplegic [...] -

DAS Case Study: Grace’s Adult Brain Injury

Meet Grace Disability: Adult Brain Injury When we met Grace, she had suffered from a brain injury as a result of complications that arose while giving birth to her son and the ensuing treatment. The results were lasting mental and physical pain from oxygen deprivation, blood loss, and disfigurement. The incident caused Grace to lose [...] -

DAS Case Study: Natalie’s Childhood Disability

Meet Natalie Disability: Cognitive and Learning Disabilities In 2015, Natalie, a young girl at the time, incurred physical, emotional and developmental injuries. Due to the length of her legal case, her financial settlement did not occur until she was 18 years old. Natalie’s intention was to finish school and ultimately work with children as a [...] -

Coldstream’s DAS at Outdoors For All Gala

Coldstream’s Disabled Advisory Services (DAS) team celebrated with our guests at Outdoors For All’s annual gala in October. The evening raised over $350,000 for programs that enrich the lives of people living with a disability through outdoor recreation experiences. OFA is the nation’s leading year-round recreation program, serving over 2,400 individuals each year. Thanks to [...] -

The Analysis of Structured and Lump Sum Payouts – What’s Right for Your Client?

DECISION TIME For personal injury attorneys, long hours spent in depositions, research, trial preparation and communications with defense counsel all culminate into successful mediation, or in some instances, a trial verdict. A person’s pain and suffering, future earning potential, and lost wages will be calculated, deliberated, debated, and tallied, representing the financial justice to the [...]