Insights

November 17, 2025

Charitable Giving After the “One Big Beautiful Bill”: Why 2025 Is the Year to Act

In Financial Planning, Philanthropy, Tax Planning

The One Big Beautiful Bill Act (OBBBA) was passed by Congress and signed into law on July 4th, 2025. This new tax law is set to reshape charitable giving rules beginning in 2026. While many of the changes appear subtle, their impact could be significant—especially for families who regularly donate to charity. With just weeks left in 2025, this is the time to evaluate whether accelerating or restructuring your giving before year-end could make a meaningful difference.

The New Rules: What Changes in 2026

1. A New “AGI Floor” on Charitable Giving

Starting in 2026, only charitable contributions above 0.5% of Adjusted Gross Income (AGI) will be deductible.

- Example: If your AGI is $750,000, the first $3,750 of annual giving will no longer be deductible.

- For corporations, the threshold is even higher, with a 1% AGI floor (the IRS also still caps corporate charitable deductions at 10%).

For high net worth families, this could mean thousands of dollars of lost deductions if giving isn’t structured thoughtfully.

2. Charitable Deduction Cap

Beginning in 2026, taxpayers in the top federal tax bracket of 37% will have their charitable deduction benefits capped at 35%. Thus, you may still deduct the full amount of the gift (provided it meets the rules), though the tax advantage will decrease slightly; the value of the deduction is limited to ~35 cents per dollar instead of ~37 cents per dollar. For example, a $10,000 donation that allows a $3,700 tax savings in 2025 would result in tax savings of only $3,500 with the new 2026 cap.

3. Partial Deduction for Tax Filers using Standard Deductions

On the positive side, OBBBA makes permanent the option for non-itemizers to claim a partial deduction for charitable giving. This reinstates a benefit first seen during the COVID pandemic, allowing more Americans to see some tax benefit even if they don’t itemize. For example, you’ll be able to deduct a portion of charitable contributions “above the line.” In other words, you can take the standard deduction and still deduct your charitable contributions as well—up to the limit of $1,000 as a single filer or up to $2,000 if married and filing jointly (MFJ) in cash donations.

Quick tip: You can check whether you used the standard or itemized deductions in 2024 by looking at line 12 of Form 1040 on your 2024 return. If there haven’t been any material changes to your tax situation, you’ll likely have the same type of deduction for 2025.

Gifting Strategy:

If you are over age 70½ or are currently taking Required Minimum Distributions (RMDs), you might consider doing most of your charitable giving through Qualified Charitable Donations (QCDs). For smaller, one-time donations, you can take advantage of the above-the-line deduction ($1,000 for single filers or $2,000 for MFJ), while still claiming the standard deduction. This approach allows you to maximize both your charitable impact and the potential tax benefits. You can read more about QCDs after the OBBB here.

4. Carryovers Still Apply (with limitations)

As in the past, if your charitable gifts exceed the annual limits (generally 30% to 60% of AGI depending on the type of gift), you can carry forward the unused deduction for up to five years. For contributions made in 2026 or later, the new 0.5% AGI “floor” will also apply when you are deducting a carryforward.

- Example: You contribute $300,000 to charity in 2026 or later in a year in which your AGI is $500,000. Because the annual deduction limit only allows you to deduct $200,000, the remaining $100,000 carries forward to future years. When you claim that $100,000 carryforward, the new 0.5% AGI floor applies in each year you use it. So, if your AGI is $200,000 in the carryforward year, the first 0.5% of that—or $1,000—cannot be deducted. That means your allowable deduction from $100,000 carryforward in that year would be $99,000.

Timing Matters

The new AGI floor doesn’t apply until January 1, 2026. That makes 2025 a critical planning year. Accelerating multi-year gifts into 2025 could maximize deductions before the new limits apply.

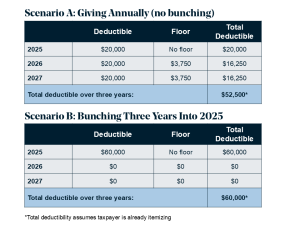

The Power of Bunching

One of the most effective strategies under the new rules is “bunching”—consolidating multiple years’ worth of charitable donations into a single tax year, often using a Donor-Advised Fund (DAF). (You can learn more about Donor-Advised Funds (DAFs) by reading our FAQs here.)

Here’s how it works for a family with $750,000 AGI that gives $20,000 in cash per year with itemized deductions and is under the 37% federal tax bracket:

Result: By bunching, this family increases their three-year deduction by $7,500 compared to spreading their charitable donations across three years evenly.

What You Should Do Now

- Review your giving plans: If you typically make annual contributions, consider accelerating future planned gifts into 2025.

- Consider a Donor-Advised Fund: A DAF lets you employ a “bunching” strategy, claiming the full deduction in 2025 while distributing grants to charities over time.

- If you are qualified, consider using QCDs for the majority of your charitable giving; you can take advantage of the above-the-line deduction ($1,000 for single filers or $2,000 for married filing jointly) for one-time donations if you’re claiming the standard deduction.

- Coordinate with your wealth manager: The right approach for your situation depends on your AGI, whether you itemize your deductions or not, and your long-term philanthropic goals.

The key takeaway is that donors should plan their giving more strategically before December 31st, 2025—especially high-income donors who might greatly benefit from bunching contributions in 2025. High-income donors who have appreciated stock should also consider using a donor-advised fund (particularly if you are planning to rebalance). The reason for bunching in 2025 is to take advantage of the full tax deduction benefit before the new 0.5% floor takes effect. The 2026 changes don’t eliminate deductions, but they will require more intentional planning. 2025 may be the most tax-efficient year to give for the rest of the decade.

At Coldstream Wealth Management, we guide families through these decisions to ensure their philanthropic giving aligns with both their values and their financial goals. Now is the time to review your giving strategy; speak with your Coldstream wealth manager as soon as possible in December to explore the best path forward toward maximizing your charitable donations. If you are looking for ideas for giving, check out Coldstream’s 2025 Annual Holiday Giving Guide here.

*Certified Financial Planner Board of Standards Inc. owns the certification marks CFP®. CERTIFIED FINANCIAL PLANNER™ and CFP® in the U.S., which it awards to individuals who successfully complete CFP Board’s initial and ongoing certification requirements.

DISCLAIMER: THIS MATERIAL PROVIDES GENERAL INFORMATION ONLY. COLDSTREAM DOES NOT OFFER LEGAL OR TAX ADVICE. ONLY PRIVATE LEGAL COUNSEL OR YOUR TAX ADVISOR MAY RECOMMEND THE APPLICATION OF THIS GENERAL INFORMATION TO ANY PARTICULAR SITUATION OR PREPARE AN INSTRUMENT CHOSEN TO IMPLEMENT THE DESIGN DISCUSSED HEREIN.

CIRCULAR 230 NOTICE: TO ENSURE COMPLIANCE WITH REQUIREMENTS IMPOSED BY THE IRS, THIS NOTICE IS TO INFORM YOU THAT ANY TAX ADVICE INCLUDED IN THIS COMMUNICATION, INCLUDING ANY ATTACHMENTS, IS NOT INTENDED OR WRITTEN TO BE USED, AND CANNOT BE USED, FOR THE PURPOSE OF AVOIDING ANY FEDERAL TAX PENALTY OR PROMOTING, MARKETING, OR RECOMMENDING TO ANOTHER PARTY ANY TRANSACTION OR MATTER.

Related Articles

April 14, 2026

Finding Tax Efficiency in an Era of Increasing Tax Obligations

April 7, 2026

The Washington Exodus Begins: Wealthy Families Weigh Their Options as Washington’s Tax Landscape Shifts

April 2, 2026

Washington State Tax Update: What Recent Tax Changes Mean for You