Insights

October 14, 2025

Markets at a Crossroads: Resilient Growth Meets Policy Uncertainty

In Market Commentary

Quarter Highlights

Global growth has proven resilient, despite trade shocks.

Since “Liberation Day,” forecasts have rebounded and even improved for 2026. Still, inflation and a weaker U.S. dollar remain the lingering scars of tariff escalation—adding to rising fiscal concerns worldwide.

Recession fears have largely faded.

A strong consumer market and an acceleration in AI-related capital spending continue to drive activity. Labor demand is slowing, but without the classic warning signs of recession.

Tariff policy remains a defining macro variable.

Elevated U.S. tariffs—including potential reciprocal rates up to 100% on certain Chinese goods starting in November—persisted (likely as a negotiation tool) and has reintroduced volatility into the market. So far, the direct pass-through to consumer prices has been modest, but the uncertainty continues to cloud corporate planning and global supply chains. These policy moves create ongoing two-way risks for both inflation and growth.

The Fed can afford to be patient.

Resilient growth and sticky inflation argue for a gradual, measured easing path. The OBBBA’s fiscal boost adds a modest tailwind into 2026, reducing the need for the Fed to make deeper rate cuts below neutral.

Fiscal policy turned stimulative through the One Big Beautiful Bill (OBBB).

The OBBB, with provisions such as expanded child tax credits and higher standard deductions, began affecting 2025 tax liabilities. Early estimates suggest effective reductions of 20–30% for households and businesses, helping to offset some trade-related drag in the economy while boosting domestic sectors like manufacturing, infrastructure, and construction.

Equities retain upside, but near-term volatility is high.

The Fed’s non-recessionary easing cycle and productivity-led earnings growth support a constructive medium-term view. However, renewed tariffs and the recent market downturn call for more guarded positioning as it relates to equities in portfolios.

Fixed income delivered steady, real returns.

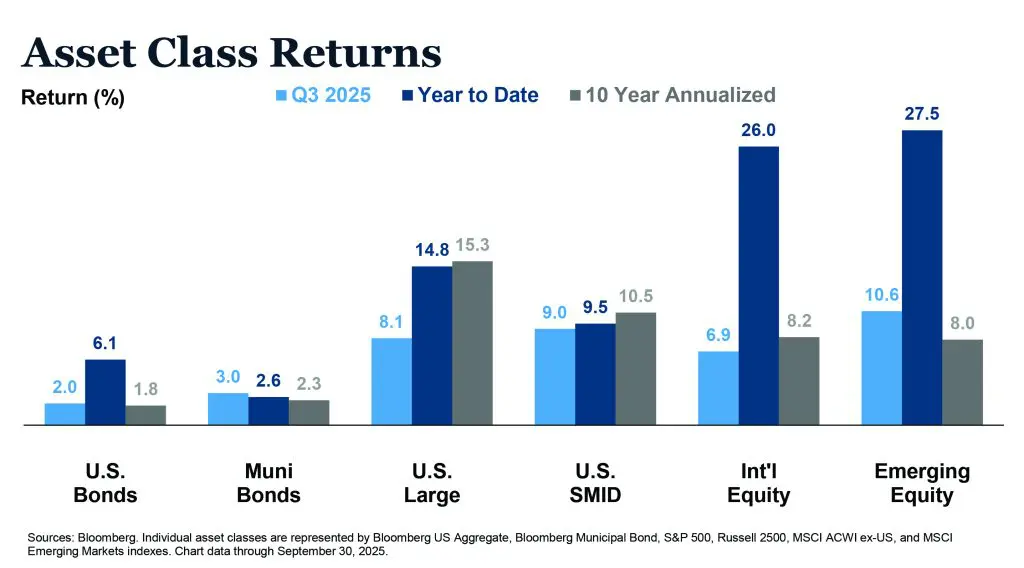

Bond markets continued to contribute positively, with the Bloomberg U.S. Aggregate Bond Index up 5.7% for the quarter. Credit spreads tightened to multi-year lows as healthy corporate balance sheets supported the asset class. Yields remain attractive by historical standards, restoring fixed income’s role as a meaningful income and risk-management tool.

Policy friction reappeared through the government shutdown.

The partial government shutdown that began October 1 has started to disrupt non-essential services and added noise to the data flow. Markets thus far have largely looked through this episode, assuming a temporary impact, but the shutdown serves as a reminder to investors of fiscal fragility and the rising cost of political brinkmanship.

Balance and diversification are essential.

Stretched valuations, uneven global policy, and shifting leadership underscore the need for diversified exposure across regions, market caps, and second-order beneficiaries of innovation and capital investment.

Economy: Resilient Growth, Structural Challenges, and Policy Tailwinds

The global economy continues to demonstrate resilience despite policy and geopolitical shocks in 2025. The U.S. economy expanded amid strong consumer spending and accelerating AI-driven capital expenditures, while Europe benefited from fiscal stimulus and a more predictable trade backdrop. China’s growth remained steady, buoyed by tech-sector optimism and domestic policy support, though lingering property market weakness tempered the upside.

Tariffs continue to shape trade and inflation dynamics. Elevated U.S. tariffs, including potential reciprocal duties on Chinese imports, remain a persistent but largely contained drag on growth. Resulting price increases have been modest, though the risk of broader inflation pressures persists as supply chains adjust and inventories deplete. The U.S. dollar remains weak, pressured by structural concerns and investor hedging, supporting international asset returns.

Monetary and fiscal policy are key drivers of near-term stability. The Federal Reserve has pursued a cautious easing path, implementing a 0.25% cut in September and signaling gradual further reductions, while the One Big Beautiful Bill (OBBB) provides targeted fiscal stimulus. Together, these policies support continued expansion without overheating, even as underlying vulnerabilities—including elevated fiscal deficits, rising government debt, and persistent inflation—remain.

Overall, the macro backdrop combines resilience with caution: near-term growth is robust, but structural and policy uncertainties argue for balanced risk-taking and diversified positioning across portfolios.

U.S. Equities: Resilience with Broadening Participation

The U.S. economy continues to expand despite policy shocks, and equities staged a powerful rally with the S&P 500 Index gaining 8.1% and small/mid cap stocks (Russell 2500 Index) gaining 9.0% for the quarter. Continued record highs were fueled by AI optimism and solid earnings growth of roughly 8% year-over-year. Profit margins continue to surprise to the upside, especially in technology, where AI-driven productivity gains are spreading from developers to end users. Markets have shifted from recession fears to optimism on rates and profits, although the final quarter of 2025 brings renewed uncertainty from government shutdowns and trade tensions with China.

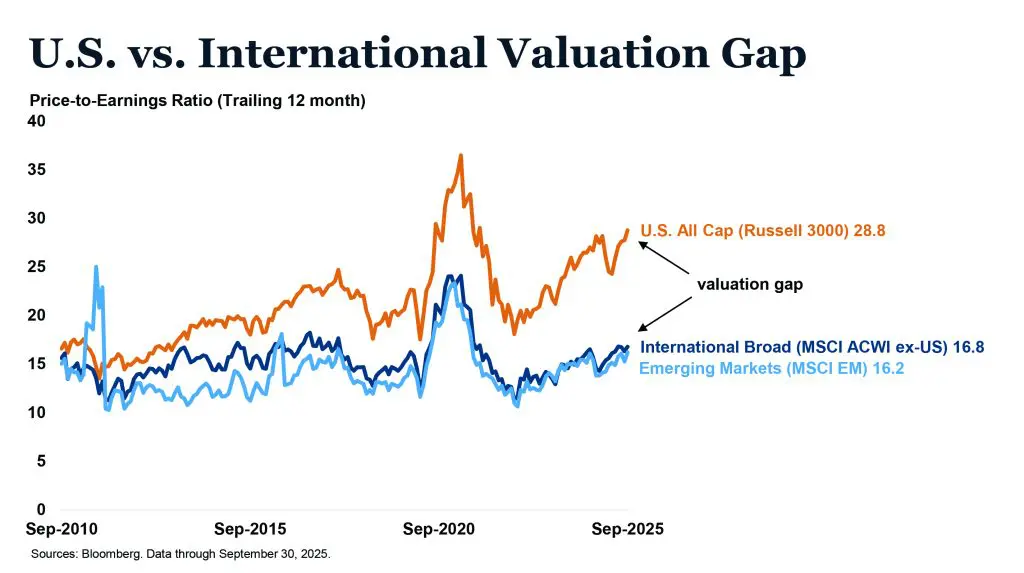

Valuations merit attention as always but have never been a reliable predictor of short- to medium-term market direction. The primary drivers behind the move upward continue to appear intact with an improved outlook for interest rates; however, earnings remain the market’s strongest engine.

International Equity: Policy Support and Valuation Appeal

International equities delivered strong relative performance in Q3, with developed markets gaining approximately 6.9% (MSCI ACWI ex-US) and emerging markets up nearly 10.6% (MSCI Emerging Markets). The rebound was led by improving earnings revisions, moderating inflation, and policy stabilization in Europe and China. After two years of lagging U.S. returns, non-U.S. equities are benefiting from attractive valuations, supportive fiscal measures, and a weakening dollar.

From a portfolio perspective, international exposure continues to play a critical diversification role. Broader participation across global markets, combined with attractive relative valuations and the prospect of monetary easing abroad, provides a compelling opportunity set as we enter the close of 2025.

Fixed Income: Income Amid Tight Spreads and Rising Risk Premiums

Fixed income markets delivered solid returns in Q3, with the Bloomberg U.S. Aggregate Bond Index up 2.0% for the quarter and 6.1% YTD. Strong macro fundamentals and supportive policy helped stabilize yields. The 10-year U.S. Treasury yield ended the quarter just above 4%, reflecting a mix of Fed easing expectations, fiscal uncertainty, and ongoing fiscal concerns.

Credit spreads sit near multi-year tights, underpinned by solid corporate fundamentals. Despite tight spreads, fixed income still provides attractive income and diversification benefits. Overall, the fixed income backdrop is constructive for income-oriented investors, but disciplined selection and diversification remain critical tools in a market of historically tight spreads and ongoing policy uncertainty.

Conclusion: Navigating Resilience Amid Uncertainty

The global economy has demonstrated remarkable resilience in 2025, defying trade shocks, policy volatility, and episodic geopolitical risks. Growth forecasts have stabilized across the U.S., Europe, and China, while U.S. recession fears have been largely dismissed thanks to robust consumer spending, strong corporate balance sheets, and AI-driven capital expenditures. Nevertheless, underlying vulnerabilities remain: elevated tariffs, lingering inflation pressures, a weaker U.S. dollar, and rising global fiscal concerns warrant cautious vigilance.

Equity markets remain strong, supported by non-recessionary Fed easing, policy tailwinds, and ongoing productivity gains, particularly in technology and AI sectors. However, stretched valuations, tariff re-escalation, and near-term market volatility call for more measured positioning. Fixed income markets continue to offer attractive income opportunities, with corporate credit supported by strong fundamentals and limited default risk, though careful security selection is essential amid tight spreads and rising risk premiums.

Portfolio management in this environment emphasizes balance, diversification, and selectivity. Investors should seek exposure across geographies, market caps, and sectors while targeting areas where macro tailwinds, policy support, and attractive valuations converge. Maintaining disciplined positioning, while remaining flexible to respond to market developments, will be critical as the expansion matures and uncertainties persist.

In short, the path forward combines opportunity and vigilance. Resilient growth and policy support provide a foundation for returns, but careful navigation of macro, policy, and valuation risks will define investment success in the remainder of 2025 and into 2026.

Information is current as of 9/30/2025, drawn from third-party sources believed to be reliable but not guaranteed as to accuracy, timeliness or completeness. None of the information provided constitutes an opinion or a recommendation or a solicitation of an offer to buy or sell any particular security. Coldstream analyses are not intended to provide, and should not be construed to constitute, complete accounting, insurance, investment, legal, or tax advice. The investment strategies and securities shown may not be suitable to you. Past performance is no guarantee of future returns. May not be reproduced, republished, or distributed without prior written consent. Questions and comments may be directed to your advisor.

* The CFA Institute owns the certification marks CFA® and Chartered Financial Analyst®. CAIA® is a registered certification mark owned and administered by the Chartered Alternative Investment Analyst Association® in the United States.

Related Articles

April 13, 2026

Watch Coldstream’s MarketCast for Second Quarter 2026

April 9, 2026

Turbulence: Navigating a Complex First Quarter

January 29, 2026

Artificial Intelligence: Boom or Bubble?