Insights

April 4, 2025

Navigating Trump’s Tariff Bombshell: Trade War or Negotiating Tactic

In Investments, Market Commentary

The market volatility that we’ve seen recently as a result of the Trump administration’s tariff announcement is naturally generating anxiety among investors. Although we all understand the risks of investing, it can take investors by surprise when market shocks occur. But as both investment professionals and students of markets and economies, we are well prepared for shifts such as these; the portfolios we craft for our clients build in long-term resilience intended to weather all parts of market cycles and unexpected changes. We see volatility such as this as part and parcel of the investment landscape and make use of all the tools available to us to manage risk while maintaining a strong position to take advantage of long-term growth. For investors who can tolerate the risk and volatility of the current situation, we think there is a good chance that you will be rewarded over time. But we recognize that it can be a difficult experience for investors, and we invite you to work directly with your advisor if you would like to consider a more conservative approach.

Below, we offer some context and insight that may be helpful in understanding the current moment and our expectations and strategy going forward. This remains a fluid situation, and we’ll keep you updated as new information emerges.

Summary of Trump’s Tariff Announcement (4/2/2025)

- President Trump declared April 2nd “Liberation Day,” declaring a “national emergency” and signed an Executive Order introducing a 10% universal tariff on all imports effective April 5, 2025, projecting up to $600 billion in annual revenue to boost U.S. manufacturing; the administration has said that tariffs will remain in effect until threats to our national position are deemed satisfied, resolved, or mitigated.

- Higher reciprocal tariffs targeted “worst offenders,” including an additional 34% on China (totaling 54% this year), 20% on the EU, 24% on Japan, 26% on India, and Southeast Asia at even higher rates – these could be more temporary.

- These tariffs aim to address the national security implications of a $1.2 trillion annual trade deficit.

- Mexico and Canada are exempt from the 10% rate with ongoing USMCA (U.S. – Mexico-Canada Agreement) talks.

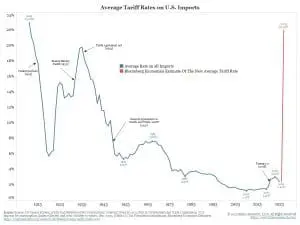

- New tariffs push the average effective tariff rate to ~25%, a high last seen in the early 1900s (refer to exhibit below).

- Additional sector-specific tariffs are possible (e.g., semiconductors, pharmaceuticals, critical minerals).

Key Observations

Unprecedented tariffs: The newly announced tariffs would be the highest since 1904, surpassing even the Smoot-Hawley Tariffs of the 1930s, and significantly higher than those in 2018.

Source: US Census Bureau, Historical Statistics of the United States: Colonial Times to 1970, Part II; US International Trade Commission, *U.S. imports for consumption, duties collected, and ratio of duties to values, 1891-2023, (Table 1); Tax Foundation calculations. Bloomberg Economics Estimates https://taxfoundation.org/research/all/federal/trump-tariffs-trade-war/

Economic context: The economy is already slowing, with some estimates of GDP growth near zero for 1Q25 and 2Q25, exacerbated by government efficiency cutbacks, reduced immigration, and uncertainty from the tariffs.

Labor market concerns: Initial unemployment claims remain low, but rising continuing claims suggest a hiring slowdown, with a potential jobs report showing only ~100,000 job gains.

Fiscal policy response: A proposed “big, beautiful bill” with tax cuts (e.g., corporate tax from 21% to 15%) and possible stimulus checks ($3,000-$5,000 per household) are being considered by Congress to counter economic weakness.

Inflation risk: Tariffs could push CPI inflation higher, complicating Federal Reserve policy, with markets pricing in three to four rate cuts by year-end if unemployment rises.

Global trade: Enormous foreign policy implications as high tariffs may lead non-U.S. countries to shun American products and firms, extending beyond economic effects.

Market reaction: U.S. equities are now in correction/bear territory, with defensive sectors outperforming, yields falling, and the dollar weakening.

Stock Market Reaction (through 4/4/2025)

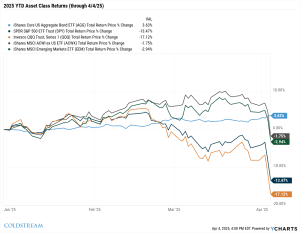

Sharp declines across major indexes: The S&P 500 Index plunged 9.1% for the week, its worst five-day period since the onset of the COVID downturn in March 2020. The more value-oriented Dow dropped 7.7% while the Nasdaq fell 10.0%, reflecting broad investor anxiety over tariff impacts. (Refer to the chart below.)

Recent leaders drove the market lower: The “Magnificent Seven” tech group lost a combined $950 billion in market cap, driving roughly half of the day’s $1.9 trillion S&P 500 loss on Thursday alone. Friday’s market declines were much more broad based.

Value stocks, while not immune, showed relative resilience: Sectors like consumer staples, healthcare and utilities have outperformed thus far in 2025, as investors rotated toward defensive plays amid tariff-induced growth concerns.

Tech and retail hit hard: Apple (AAPL) and Nike (NKE) have both tumbled in excess of -23% year-to-date as tech and retail stocks, reliant on global supply chains, bore the brunt, with the Nasdaq nearing a circuit breaker threshold. (Refer to the chart below.)

Flight to safe havens: Bond yields continue to fall as investors flock to safe-haven assets. The Barclays US Aggregate Index gained 2.7% on the year. This reflected heightened recession fears outweighing short-term inflationary pressures from tariffs.

Global ripple effects: International and Emerging Markets followed the path of the U.S. market, albeit with more muted losses on Thursday but then accelerated on Friday as foreign trade partners started announcing retaliatory tariffs.

*Source: YCharts, Coldstream

*Source: finviz.com (YTD returns through 4/4/25)

Coldstream’s Strategy

Coldstream will continue to place an emphasis on diversification in areas of core bonds, international equities, and alternatives, and focus on active management around valuations, quality, and tariff impacts in sectors like tech and materials.

As the tariff landscape shifts dramatically, investors face a complex environment of uncertainty with stagflationary pressures, heightened recession risks, and global trade tensions. With recession risks elevated and market volatility likely to persist, adapting strategies to evolving trade negotiations and policy shifts will be essential. We believe investors can weather the immediate turbulence of this tariff-driven economic shift while remaining positioned for longer-term opportunities with defensive positioning, an allocation to bonds which now have a supportive yield cushion, diversified equity allocations, style diversification, and proactive management.

Sharp market drops like we experienced today undoubtably feel unsettling, but it’s important to take a step back and put it in perspective. Volatility is a natural part of the market’s rhythm, especially when big policy shifts like universal tariff announcements hit the headlines. Markets hate uncertainty, and right now, they’re pricing in a mix of fear and speculation about what these tariffs could mean for trade, inflation, and corporate earnings. The duration and ultimate depth of these tariffs remain uncertain, complicating the outlook. The initial reaction is often a knee-jerk sell-off as traders scramble to adjust. But history shows us that these storms tend to pass.

Over the long term, the market’s trend has been unmistakably upward. Take the S&P 500 Index as a guide: since 1950, it’s finished the year higher about 70% of the time, with an average annual return of around 9% after inflation. On a day-to-day basis, markets tend to see a decline roughly 45% of the time. But those down days often eventually equate to noise in the bigger picture for long-term investors. Over decades, the market rewards patience, not panic. Tariffs, while disruptive, don’t rewrite that story; it’s quite possible that they are intended to be a negotiating tool, and the real impact depends on how they’re implemented and how businesses adapt. Supply chains have been rewired before, and they’ll adjust again if needed.

The fundamentals still hold: companies are generating profits, consumers are spending, and the labor market remains resilient. Central banks are watching closely, too, with tools to cushion any prolonged fallout. Days like April 3rd are a reminder that markets overshoot—both up and down. Volatility is an integral part of investing, and it naturally increases around major announcements like universal tariffs. We’ve certainly lived through similar downside experiences during the Great Financial Crisis of 2008 and the early onset of COVID just over five years ago in 2020.

We continue to believe in a steady, disciplined approach that aligns with your unique financial goals, and we’re here to support you in maintaining focus on the big picture. Diversification across sectors, geographies, and asset classes is an important tool to help balance portfolios against unknown risks and to ride out market swings. We’ve seen markets respond aggressively like this before and are confident that we have the tools in place to help you weather the storm. We believe that over the long term, investors are rewarded for taking risk and encourage you to keep a long-term perspective, allowing your portfolio time to both recover and then continue to grow as markets stabilize.

As always, we’re committed to guiding your strategy with your long-term objectives in mind, maintaining a thoughtful, disciplined, and balanced approach. Thank you for your continued trust in us, and please don’t hesitate to reach out with any questions or concerns.

* The CFA Institute owns the certification marks CFA® and Chartered Financial Analyst®. CAIA® is a registered certification mark owned and administered by the Chartered Alternative Investment Analyst Association® in the United States.

Related Articles

May 28, 2026

Building a Financial Foundation: Books for Young Adults

May 15, 2026

Irrational Decisions in Investing

May 8, 2026

What Does ESG Investing Look Like Today?