Insights

February 1, 2026

Helping You Make the Most of Your Micron Benefits (2026 Edition)

In Company Benefits

Working at Micron comes with more than a competitive paycheck—it comes with a powerful set of benefits designed to help you build long-term wealth, protect your family, and participate in the company’s success.

Yet, with so many options—from equity grants to deferred compensation and after-tax 401(k) contributions—it can be hard to know where to focus. The reality is, a few small adjustments can make a big difference over time. Below is a practical guide to help you understand Micron’s 2026 benefit programs, updated plan limits, and how to make each component work harder for you. Download a pdf of this article here.

Micron Benefits Summary

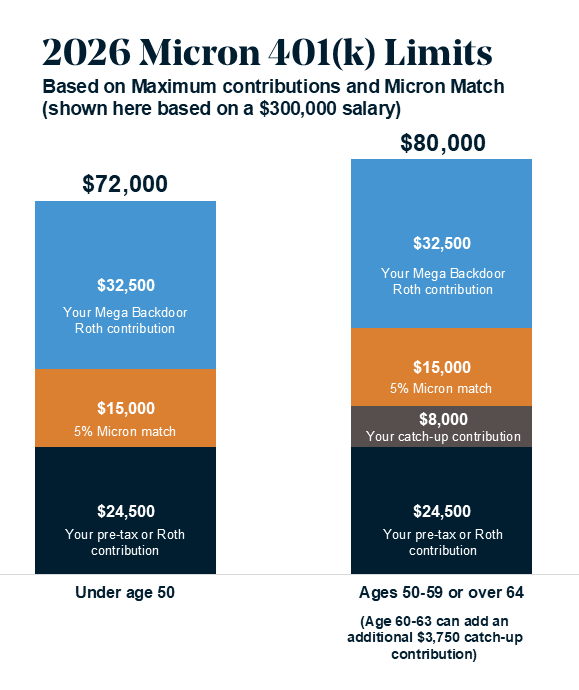

Source: Micron 2026 U.S. Benefits guide

Source: Micron 2026 U.S. Benefits guide, Coldstream

Key Planning Opportunities for 2026

1. Use the New 401(k) Limits to Your Advantage

The 2026 IRS limits are higher than ever, creating more room to save efficiently. The 2026 IRS maximum annual pre-tax/Roth limit is $24,500 plus $8,000 in additional catch-up contributions for team members age 50-59. Note, if you’re age 60–63, take advantage of the enhanced catch-up contribution, which allows an additional $11,250 on top of the base limit (instead of the $8,000 noted above).

This applies to both standard and enhanced catch-up contributions for participants ages 50 and above. We still recommend completing those vs. saving in a taxable account, since you will receive the benefit of tax-free growth and tax-free qualified distributions within a Roth IRA.

Even if you can’t max out your 401(k) contributions, increasing your deferrals by just 1–2% per year can have a major long-term impact.

2. Leverage the Mega Backdoor Roth

Micron’s plan allows after-tax 401(k) contributions up to the total $72,000 cap (or higher for those over 50). By converting those after-tax dollars into a Roth, you can build a larger pool of tax-free income for retirement. This is one of the most powerful but underused tools in employer plans today. It’s also highly important to elect for in-plan Roth conversion of after-tax contributions by contacting Fidelity. Learn more about Roth conversions in our article, “Unlocking the Power of Roth Conversions for Long-Term Wealth Growth” here.

3. Be Intentional with Deferred Compensation

Deferring income can smooth out taxes, especially if you expect lower income in retirement. But remember—this is an unsecured promise by Micron. Make sure you’re not deferring more than you’re comfortable leaving at risk.

4. Balance Company Stock with Diversification

Between Restricted Stock Units, Employee Stock Purchase Plans (ESPP), and options, it’s easy for Micron stock to dominate your entire portfolio. Set target percentages for how much company stock you’re comfortable holding and sell systematically once that threshold is reached. Diversification protects your long-term financial independence.

5. Plan Around Tax Timing

Equity vesting, ESPP sales, and deferred compensation payouts all create taxable events. Coordinating those across years—and possibly pairing them with charitable giving or higher 401(k) contributions—can reduce your effective tax rate.

Bringing It All Together

Micron provides a comprehensive suite of competitive benefits for its team members. But the real opportunity is in how you combine them—aligning your savings, equity, and deferred compensation decisions with your personal goals, tax plan, and time horizon.

Whether your priority is maximizing savings, reducing taxes, or simply creating more flexibility in how and when you work, these benefits can be a cornerstone of your plan when managed thoughtfully.

At Coldstream, we help Micron professionals integrate these programs into a bigger picture—making sure every dollar, share, and tax election is working toward your long-term goals. If you have questions about which options are right for you or how they best fit with your tax and financial situation, consult your Coldstream Wealth Manager.

*Certified Financial Planner Board of Standards Inc. owns the certification marks CFP®. CERTIFIED FINANCIAL PLANNER™ and CFP® in the U.S., which it awards to individuals who successfully complete CFP Board’s initial and ongoing certification requirements.

DISCLAIMER: THIS MATERIAL PROVIDES GENERAL INFORMATION ONLY. COLDSTREAM DOES NOT OFFER LEGAL OR TAX ADVICE. ONLY PRIVATE LEGAL COUNSEL OR YOUR TAX ADVISOR MAY RECOMMEND THE APPLICATION OF THIS GENERAL INFORMATION TO ANY PARTICULAR SITUATION OR PREPARE AN INSTRUMENT CHOSEN TO IMPLEMENT THE DESIGN DISCUSSED HEREIN.

CIRCULAR 230 NOTICE: TO ENSURE COMPLIANCE WITH REQUIREMENTS IMPOSED BY THE IRS, THIS NOTICE IS TO INFORM YOU THAT ANY TAX ADVICE INCLUDED IN THIS COMMUNICATION, INCLUDING ANY ATTACHMENTS, IS NOT INTENDED OR WRITTEN TO BE USED, AND CANNOT BE USED, FOR THE PURPOSE OF AVOIDING ANY FEDERAL TAX PENALTY OR PROMOTING, MARKETING, OR RECOMMENDING TO ANOTHER PARTY ANY TRANSACTION OR MATTER.

Related Articles

January 2, 2026

New Gifting and Contribution Limit Changes For 2026

November 3, 2025

Maximizing Your Employer Benefits

October 31, 2025

Maximizing Your Google Benefits: A Strategic Guide for 2026