Insights

November 14, 2023

Bundling Charitable Contributions to Maximize your Tax Benefits

In Philanthropy, Wealth Strategy

If you’re reading this article, it’s likely you are charitably inclined, value giving back to the community, and attend fund-raising events for the causes most important to you.

Now picture this… you are sitting at a table for your favorite annual gala – the time has come to fill out your donation form and write a check or add your credit card number to make that large donation. But did you know there’s a more tax-advantaged option on that form? It’s a check box that says, “Donate from Your Charitable Gift Fund.” The donation you are about to make at that moment could both generously support the organization AND provide some beneficial tax planning opportunities. How? Let us introduce you to the wonderful world of Charitable Gift Funds.

What is a Charitable Gift Fund?

Also known as a Donor Advised Fund (DAF), a Charitable Gift Fund is essentially a giving account. It allows you to make a charitable contribution, receive a current year tax deduction, and make charitable gifts over time. Charitable gift funds are established at a charitable sponsor (e.g., Fidelity Charitable or Schwab Charitable). Once you’ve contributed to your Charitable Gift Fund, the assets are managed at the charitable sponsor, typically require no annual distributions, and offer options for anonymous granting. You, as the donor, can recommend how, what, and when the assets are ultimately gifted to the various non-profit organizations of your choice.

Ways to Donate to Your Charitable Gift Fund

You can fund and contribute to your Charitable Gift Fund using:

- Cash

- Appreciated securities (e.g., stocks, bonds, or mutual funds)

- Real estate

- Privately held business interest.

Funding Limits

Before making a large contribution to your Charitable Gift Fund, you’ll want to review the annual limits on the deductibility of gifts to maximize your tax benefit. Deductibility varies based on whether you 1) contribute to a qualified organization versus a non-qualified organization, and 2) the type of asset(s) you are donating. We typically recommend donating long-term appreciated stock to Charitable Gift Funds (which are considered a qualified organization).

The deductibility limit for donating long-term appreciated stock (held over one year) to your Charitable Gift Fund is 30% of your Adjusted Gross Income (AGI). If you contribute more than this deduction limit, the excess deduction can be carried over up to five years. If you choose to contribute cash, the donation deductibility limit is 60% of your AGI.

Donations to your Charitable Gift Fund are deductible if you itemize when filing your tax return.

Bundling Charitable Contributions to Maximize Your Tax Benefit

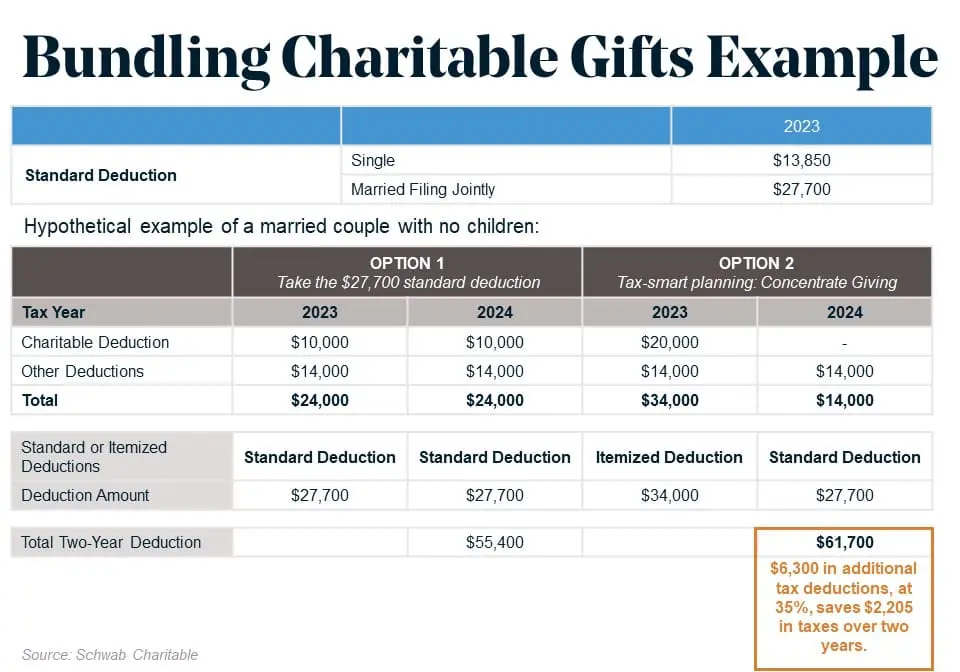

One tax-advantageous strategy is bundling multiple years of charitable giving to your Charitable Gift Fund in one year. This tactic allows you to take advantage of bigger tax benefits gained by itemizing deductions in a single year, versus what you might otherwise receive from spreading the gifts out over several years. Here is an example:

As illustrated in “Option 2” from the example above, by gifting two years’ worth of charitable contributions to your Charitable Gift Fund in one year, you are able to leverage itemized deductions and reduce your overall taxes across two years while at the same time continuing to support the charities that are important to you.

Beginning in 2026, the standard deduction is scheduled to be reduced by approximately half due to the expiring provisions of the 2017 “Tax Cuts and Jobs Act.” This makes the bundling strategy most effective in tax years 2023 and 2024.

Charitable giving can be an impactful part of your financial plan. With a little forethought, the gifts you make can benefit non-profit organizations you care about and be structured effectively to reduce your income tax bill. Please reach out to your Coldstream team if you’d like to discuss tax-advantaged charitable giving.

DISCLAIMER: THIS MATERIAL PROVIDES GENERAL INFORMATION ONLY. COLDSTREAM DOES NOT OFFER LEGAL OR TAX ADVICE. ONLY PRIVATE LEGAL COUNSEL OR YOUR TAX ADVISOR MAY RECOMMEND THE APPLICATION OF THIS GENERAL INFORMATION TO ANY PARTICULAR SITUATION OR PREPARE AN INSTRUMENT CHOSEN TO IMPLEMENT THE DESIGN DISCUSSED HEREIN. CIRCULAR 230 NOTICE: TO ENSURE COMPLIANCE WITH REQUIREMENTS IMPOSED BY THE IRS, THIS NOTICE IS TO INFORM YOU THAT ANY TAX ADVICE INCLUDED IN THIS COMMUNICATION, INCLUDING ANY ATTACHMENTS, IS NOT INTENDED OR WRITTEN TO BE USED, AND CANNOT BE USED, FOR THE PURPOSE OF AVOIDING ANY FEDERAL TAX PENALTY OR PROMOTING, MARKETING, OR RECOMMENDING TO ANOTHER PARTY ANY TRANSACTION OR MATTER.

Insights Tags

Related Articles

June 4, 2026

Becoming Financially Independent: A Practical Checklist for Young Adults

May 28, 2026

Building a Financial Foundation: Books for Young Adults

May 15, 2026

Irrational Decisions in Investing