Insights

January 23, 2026

Filing for Medicare: What to Consider When Claiming Benefits

In Insurance, Retirement

Many Americans are accustomed to private health insurance, whether that be coverage through their employer, or a plan purchased individually. Reaching eligibility for Medicare marks a crucial step toward transitioning away from job-based health insurance in retirement. The process can feel daunting if you don’t understand the various components of your coverage. Here, we aim to distill the complexities in order to help facilitate a smooth process.

UNDERSTANDING COVERAGE

Medicare Part A (Hospital Insurance) primarily covers hospital stays, skilled nursing facility care, hospice care, and some home health services. Part B (Medical Insurance) encompasses medical services such as doctor visits, outpatient care, preventive services, physical and occupational therapy, and durable medical equipment. Part C (Medicare Advantage) offers a private insurance option for Parts A & B. Choosing a Medicare Advantage plan can provide enhanced benefits depending on your specific needs, but does potentially limit access to in-network doctors and coverage. Lastly, Part D focuses on prescription drug coverage.

WHEN TO ENROLL

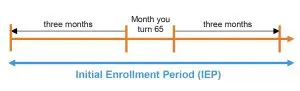

It is generally advisable to begin the Medicare enrollment process at least three months before turning 65. Your enrollment window lasts a total of seven months, starting three months before you turn 65 and ending three months after the month you turn 65. This period is referred to as the Initial Enrollment Period (IEP). Applying for Medicare during the IEP helps avoid potential gaps in healthcare coverage and protects you from late enrollment penalties.

Medicare applications are typically done through the Social Security Administration. If an individual is already receiving Social Security benefits upon turning 65, they have the good fortune of being automatically enrolled in Medicare Parts A and B. However, if you plan to delay your Social Security until after age 65, it is important to understand that you will not be automatically enrolled in Medicare. With full retirement age at (FRA) at 67 for many Americans, and many opting to delay their Social Security benefits until FRA or later, this is becoming a larger issue to be aware of.

CONSIDERATIONS IN CHOOSING COVERAGE

Choosing the right Medicare plan requires consideration of your individual healthcare needs and preferences. While Medicare (Part A and B) provides comprehensive coverage, many Americans opt for Medicare Advantage (Part C) plans offered by private insurers. The reasons vary but tend to revolve around enhanced benefits such as dental coverage, vision coverage, hearing services, and perhaps of most importance, the ability to stay with your primary care physician.

MEDICARE PREMIUMS

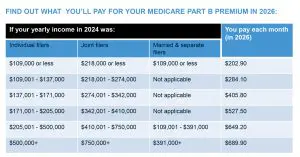

The most common method of paying Medicare premiums is a deduction directly from your Social Security check; however, other payment methods are available. Part A coverage comes with no-cost premiums, as long as you have paid Medicare taxes for at least ten years. Premiums are assessed for your Part B coverage, which are calculated based on your income. The higher your Modified Adjusted Gross Income (MAGI), the higher your monthly premium will be for Medicare Part B. For 2026, the standard Part B monthly rate is $202.90. But you would pay higher rates if your MAGI exceeds $109,000 ($218,000 on a joint return). Managing this MAGI can be challenging for retirees in years where they have one-time income or gain events, as these events may trigger higher-than-expected Medicare premiums. If you experienced a major life changing event (marriage, divorce, death of spouse, loss of income), you may contest the increase by submitting Form SSA-44.

MEDICARE SUPPLEMENT INSURANCE (MEDIGAP)

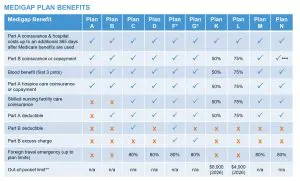

Medicare supplemental insurance, called Medigap, is insurance sold by private companies meant to help fill in the gaps in Medicare, covering out-of-pocket costs such as premiums, copays, and deductibles. You must be enrolled in Medicare Part A and B to qualify for Medigap policies. Medigap insurance does not offer additional benefits; it just helps cover the out-of-pocket expenses after Medicare.

There are ten different types of Medigap plans offered in most states, named by letters A, B, C, D, F, G, K, L, M, N. Plans with the same letter name offer the same benefits, though the price may change from state to state and by insurance company. It’s important to compare the costs of different Medigap plans, as premiums can vary widely.

ENROLLING IN MEDIGAP

Medigap open enrollment begins the first month you have Medicare Part B and are 65 or older; for the next six months, you can enroll in any Medigap policy. This is a one-time open enrollment period; after this period, you may not be able to buy a Medigap policy, or you might only be able to access it at a higher cost. Some states offer Medicare SELECT policies, which allow you to change your mind within a year of enrolling and switch to a standard Medigap policy. You cannot enroll in both Medicare Advantage and Medigap; you must choose one or the other.

Learn more about Medigap and Medigap plans at https://www.medicare.gov/health-drug-plans/medigap/basics

NOTE: Plan C & Plan F aren’t available if you turned 65 on or after Jan. 1, 2020, and to some people under age 65. You might be able to get these plans if you were eligible for Medicare before Jan. 1, 2020, but not yet enrolled. Learn more about these plans at https://www.medicare.gov/health-drug-plans/medigap/basics/compare-plan-benefits

*Plans F & G offer a high deductible plan in some states.

** Plans K & L show how much they’ll pay for approved services before you meet your out-of-pocket yearly limit and Part B deductible. After you meet them, the plan will pay 100% of your costs for approved services.

*** Plan N pays 100% of the costs of Part B services, except for copayments for some office visits and some emergency room visits.

SOURCE: Medicare.gov; https://www.medicare.gov/health-drug-plans/medigap/basics/compare-plan-benefits

WHAT IF YOU’RE STILL WORKING AT AGE 65?

We are often asked what to consider with Medicare enrollment if you are still working past 65? An important consideration is whether your company employs 20 or more people.

If you are working past 65 and have health insurance coverage from a company that employs 20 or more people, you can delay enrolling in Medicare until the employment ends or the coverage stops, whichever occurs first. You would then qualify for a special enrollment period to enroll in Medicare before or within eight months of losing the job-based health insurance.

If instead your coverage is from a company with fewer than 20 employees, you will need to speak directly with your employer to determine how to handle your health insurance. Companies with fewer than 20 employees have the choice of allowing you to stay on their plan or dropping you from coverage and requiring you to enroll in Medicare. If this is your situation, we strongly recommend working with your employer to determine how the employer’s plan will fit in with Medicare coverage.

MAKING CHANGES

Lastly, if this all feels overwhelming, don’t worry! Your decisions don’t have to be permanent. Open enrollment occurs annually in the fall (October 15 – December 7). If your coverage needs have evolved, we recommend reviewing your options during open enrollment.

Applying for Medicare is a pivotal step toward securing healthcare coverage during your golden years. Understanding the eligibility criteria, enrollment periods, premiums, and available coverage options are key in selecting the best plan for your specific healthcare needs. Your Coldstream advisor can help you assess your needs and include health care coverage into your long-term financial plan, and we would be happy to refer you to a Medicare specialist who can help you understand your coverage options and provide guidance in selecting the optimal plan.

SOURCE: medicare.gov: https://www.medicare.gov/publications/11579-medicare-costs.pdf

Insights Tags

Related Articles

February 27, 2026

New Ways to Access Your Social Security Account: Login.gov or ID.me

October 31, 2025

Maximizing Your Google Benefits: A Strategic Guide for 2026

September 22, 2025